With favorable demand driven by demographics and social trends that are likely to continue for years, the institutional single-family rental market is poised to become a growing commercial real estate niche.

Strong demand has created robust fundamental performance and opportunities for growth.

The institutional SFR market does face challenges, including garnering (unwarranted) blame for the rising cost of housing and the waning of scattered-site acquisitions over the last two years after rising interest rates pushed up the cost of capital. Yet the segment was given a shot in the arm from the pandemic, which increased demand for single-family homes and suburban housing, while growth is driven by construction of build-to-rent (BTR) communities.

DEMOGRAPHICS BOOST DEMAND

The SFR market is not new, as there are nearly twenty million single-family homes operating as rentals in the US. The vast majority of SFRs are owned by small operators, primarily “mom and pop” operators that own fewer than ten units. Institutions with a hundred or more units own roughly 800,000 units, or less than 5% of SFRs and less than 1% of all single-family homes in the US.

Demand for SFRs has soared in recent years, for a myriad of reasons. But it all boils down to the fact that there is a large cohort of households that want the amenities of a single-family home but cannot or do not want to afford a home. These drivers include:

- Work from home. Hybrid work is becoming the norm in many office-using industries. Homes have extra space compared to apartments and are more conducive to work with less noise.

- Growing families that were in apartments but want more space for children and/or pets.

- Renters that want the flexibility to move for job opportunities.

- Downsizing empty-nesters who want single-family home amenities but don’t want the burdens of maintenance.

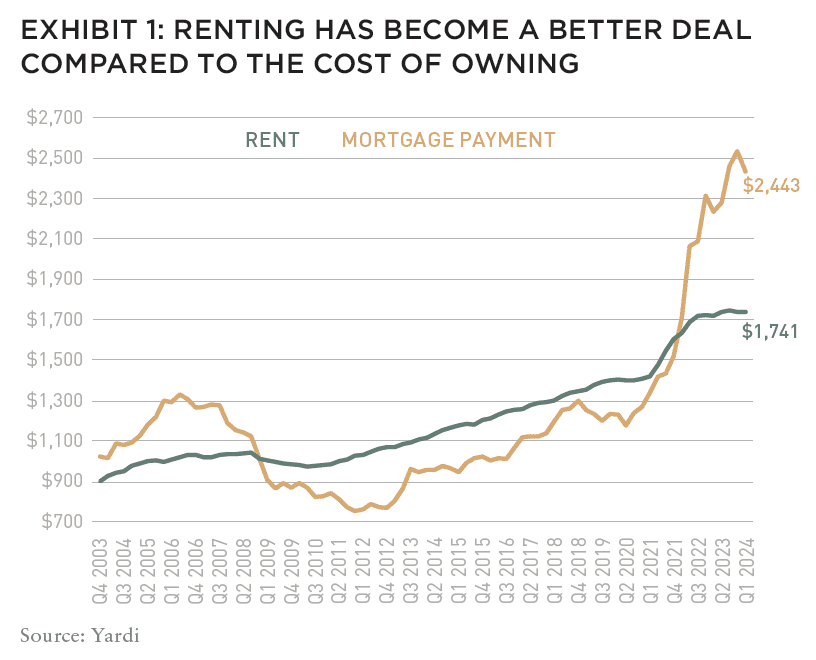

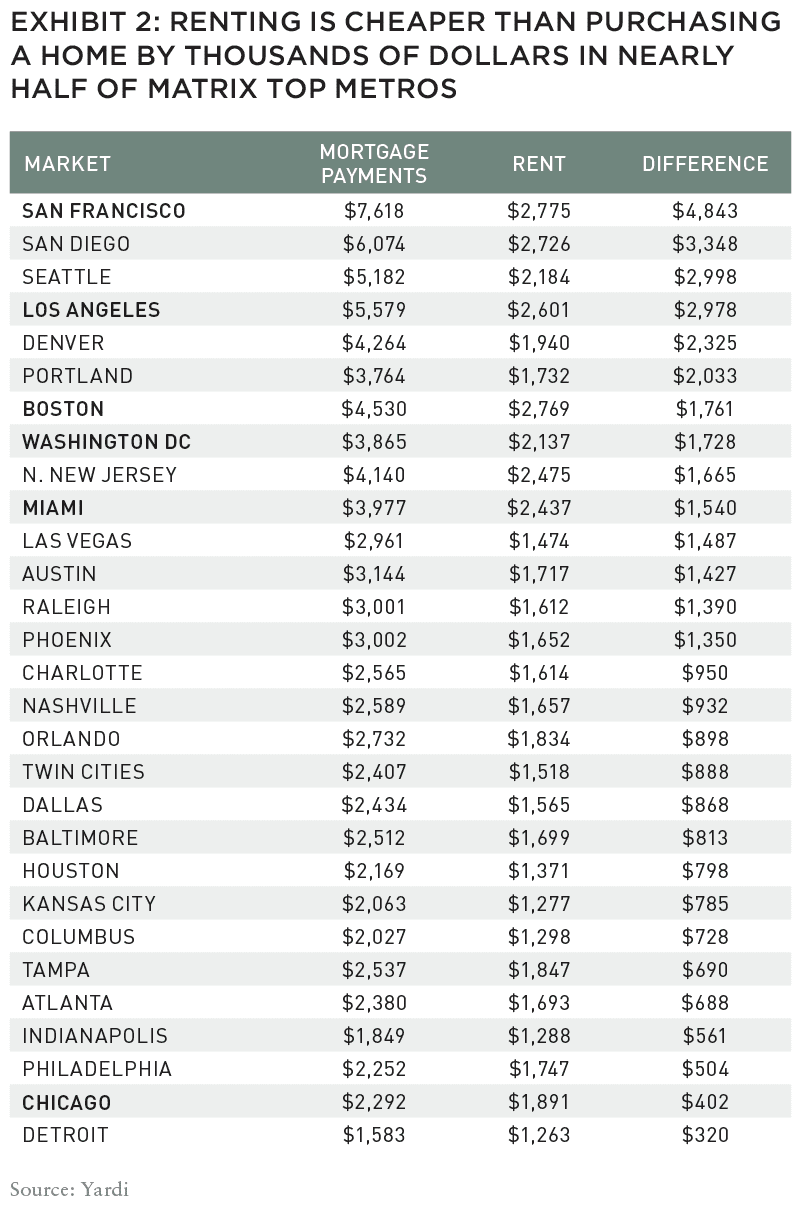

- Households that would like to own but cannot afford to buy. With interest rates at the levels they are in the second quarter of 2024, the cost of owning a median-priced home with a thirty–year mortgage is about 40% more expensive than the average US rent—the biggest gap between the two in recent decades. That keeps many first-time homebuyers in rentals.

STRONG FUNDAMENTAL PERFORMANCE

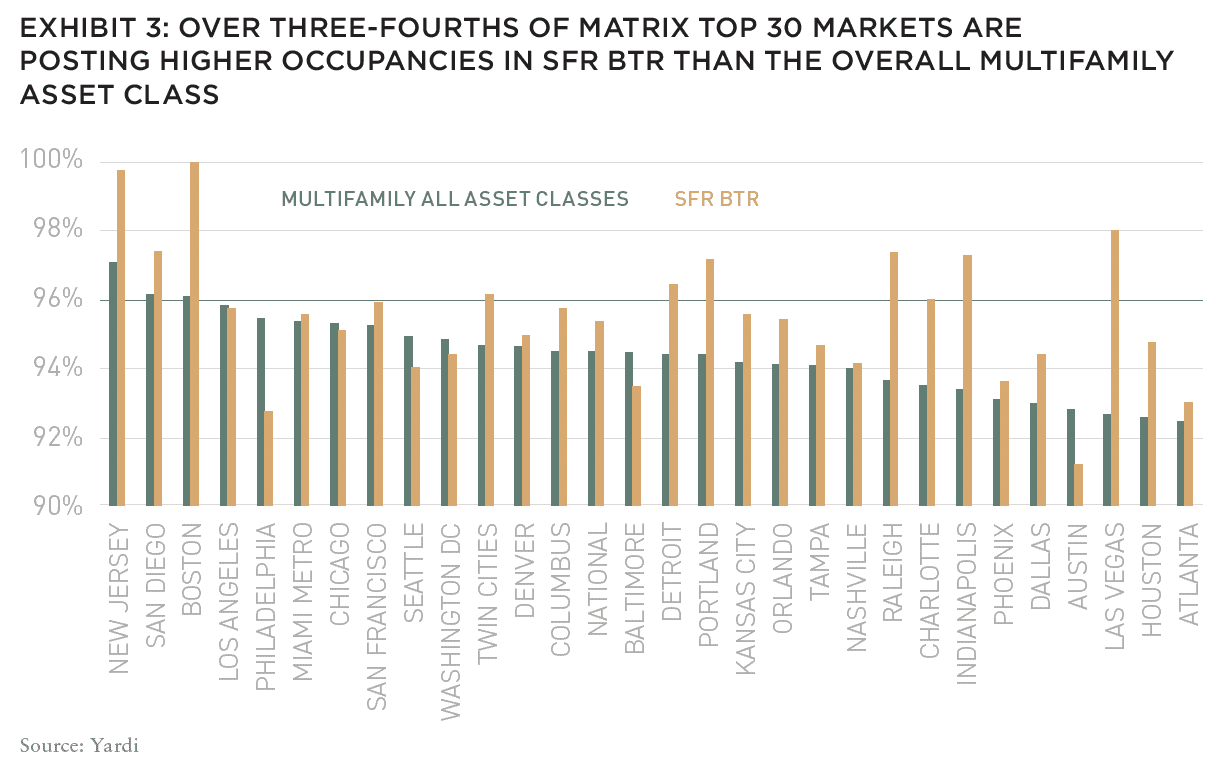

Strong demand for SFRs is producing healthy fundamentals, according to Yardi Matrix data on more than 163,000 units in communities with fifty or more units. Directionally, SFR has acted much like multifamily in recent years, with demand and rents surging post-pandemic due to a wave of household formation, then moderating through the course of 2023. However, SFR rent growth and occupancy rates have been slightly better than multifamily.

As of March 2024, occupancy in SFR communities nationally was 95.4% nationally—about a full percentage point ahead of multifamily rates. The occupancy rate for SFR renter-by-necessity (RBN) units, which encompasses less expensive properties, was even higher at 96.6%, demonstrating strong demand for more affordable units. The national occupancy rate for higher-end Lifestyle SFR properties at the end of Q1 2024 was also strong at 95.0%.

The average national SFR rent was an all-time high of $2,154 as of April 2024, compared to $1,725 for multifamily, according to Matrix. SFR rents have grown 30% between the start of the pandemic lockdowns in April 2020. Year-over-year SFR rent growth as of April 2024 was 1.3% nationally; 70 basis points higher than 0.6% multifamily growth, per Matrix. SFR rents were led by RBN properties, which recorded 3.9% growth, while Lifestyle rents were up 0.4%.

ACQUISITIONS SUBSIDE, BTR GROWING

Low interest rates were conducive to acquisitions for institutional SFRs, which expanded their portfolios rapidly in 2021 and 2022 through both scattered-site and portfolio acquisitions. Matrix recorded a record $2.8 billion of transactions of communities with fifty or more units in 2021 and another $2.7 billion in 2022.

However, the rise in mortgage rates throughout 2022 made purchasing homes less profitable. SFR acquisitions were curtailed due to pricing uncertainty and the lack of overall inventories of for-sale homes. Acquisitions of SFR communities dropped to $1.4 billion in 2023 and is at $400 million through April 2024, per Matrix. Scattered site acquisitions have fallen to less than 2% of total institutional home purchases, according to John Burns Real Estate Consulting.

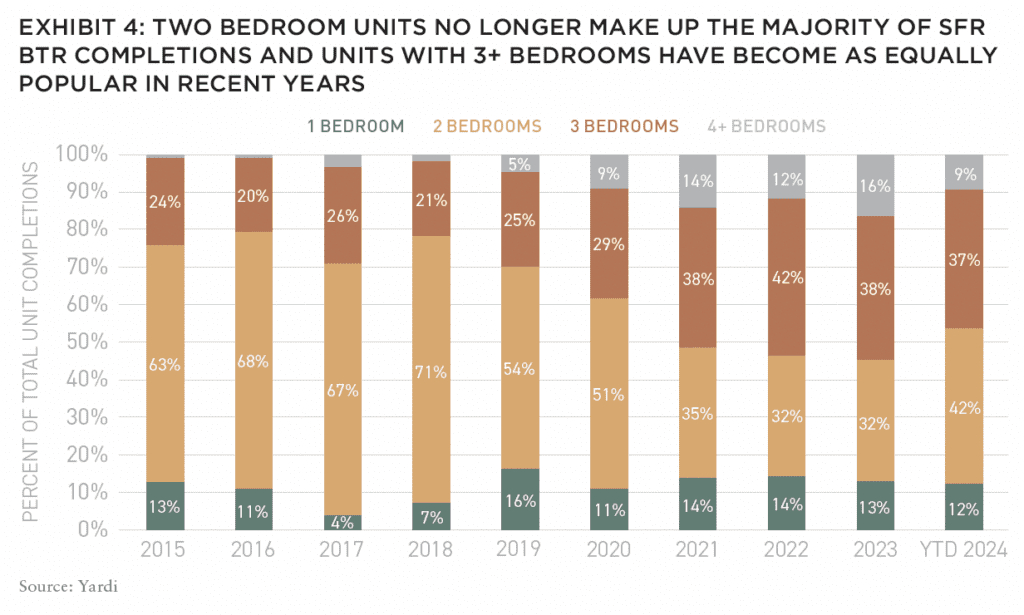

Consequently, institutional SFR growth is increasingly coming through the development of new communities. A record high 64,000 BTR units were under construction as of April 2024, according to Matrix. We forecast 32,350 deliveries in 2024, also a record, topping the previous peak 29,100 units delivered in 2023.

While those numbers are insignificant compared to the more than 500,000 multifamily deliveries forecast by Matrix to be delivered this year, bear in mind that build-to-rent as a market strategy is barely a decade old. It was not until 2016 that more than 5,000 units BTR came online in a single year.

Unless or until interest rate conditions change dramatically, institutional SFR growth will increasingly come from BTR rather than scattered-site acquisitions. Not just because of financial conditions, either. SFR operators are realizing the value in being able to control the quality of construction while property management and on-site maintenance are more efficient when units are adjacent.

As BTR grows, developers are able to construct communities with amenities that attract tenants, including community facilities such as pools, clubhouses, trails, attached garages, and on-site maintenance. Other amenities that are highly desired include better parking, storage, and yards, even if small. Young singles and couples prefer pet-friendly units, while families prefer large common areas. Developers also can design units to include smart home technology such as EV charging in garages and resilient design to accommodate frequent moving.

MEETING CHALLENGES

Institutional SFR growth does not lack challenges. Legislators on the federal and state level have introduced laws to limit institutions from buying single-family homes. While none of these laws have yet passed, the industry must fight the policy backlash. The key to improving housing affordability is through matching demand with enough supply, not limiting ownership.

Institutions also are contending with ways to increase efficiency in property management and maintenance, the rising levels of fraud, finding suitable land to build on and entitlement process resistance in municipalities that prefer for-sale homes. The upshot, though, is that with demand for SFR product remaining durable and institutional capital available, the segment is on target to become a growing niche sector in commercial real estate.

EXPLORE THE NEW ISSUE

NOTE FROM THE EDITOR: WELCOME TO #15

Benjamin van Loon | AFIRE

MID-YEAR CRE MARKET OUTLOOK: AFIRE

Benjamin van Loon and Gunnar Branson | AFIRE

MULTIFAMILY OUTLOOK: AMERICAN REALTY ADVISORS

Sabrina Unger and Britteni Lupe | American Realty Advisors

MULTIFAMILY GAP CAPITAL: BARINGS REAL ESTATE

Dags Chen, CFA and Lincoln Janes, CFA | Barings Real Estate

SINGLE-FAMILY RENTAL OUTLOOK: CERBERUS CAPITAL MANAGEMENT

Kevin Harrell | Cerberus Capital Management

SINGLE-FAMILY RENTAL SUPPLEMENT: YARDI

Paul Fiorilla | Yardi

LOGISTICS OUTLOOK: BRIDGE INVESTMENT GROUP

Jay Cornforth, Jack Robinson, PhD, Morgan Zollinger, and Cole Nukaya | Bridge Investment Group

DATA CENTER OUTLOOK: PRINCIPAL ASSET MANAGEMENT

Casey Miller and Ben Wobschall | Principal Asset Management

SELF-STORAGE OUTLOOK: HEITMAN

Zubaer Mahboob | Heitman Europe

COLD-STORAGE OUTLOOK: NEWMARK

Lisa DeNight | Newmark

OFFICE OUTLOOK: CUSHMAN & WAKEFIELD

David Smith | Cushman & Wakefield

RETAIL OUTLOOK: MADISON INTERNATIONAL REALTY

Christopher Muoio | Madison International Realty

HOSPITALITY OUTLOOK: JLL

Zach Demuth | JLL

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

ABOUT THE AUTHORS

Paul Fiorilla is Director of Research for Yardi Matrix, which provides critical data for professional property managers.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Founded in 1992, Cerberus is a global leader in alternative investing with approximately $65 billion1 in assets across complementary credit, private equity, and real estate strategies. We invest across the capital structure where our integrated investment platforms and proprietary operating capabilities create an edge to improve performance and drive long-term value. Learn more.

Principal Real Estate is the dedicated real estate investment team of Principal Asset Management, the global investment solutions business for Principal Financial Group®. As a top 10 global real estate manager, with over $98 billion in assets under management and more than 60 years of experience, we provide clients with access to opportunities across both public and private equity and debt. Learn more.