Even as the retail sector has fallen out of favor with CRE investors the past few years, investors could be overlooking potential opportunity as the sector’s fundamentals look increasingly healthy in our post-pandemic landscape.

The retail sector has fallen dramatically out of favor with US commercial real estate (CRE) investors, plunging from 27.5% of total US CRE deal volume in the early to mid-2000s to just 9.5% of total deal follow in the aftermath of the COVID-19 pandemic.

In 2023, retail comprised 15% of deal volume, on par with the office sector, which continues to garner headlines for its challenged fundamentals and high-profile defaults.1 In fact, when calls for submissions for this edition of Summit Journal went out, retail was the last sector to be claimed—as no one had interest in writing on the topic.

And at a recent US CRE conference I attended (not AFIRE), the sector was entirely ignored. However, as the sector’s fundamentals look increasingly healthy in this post-pandemic landscape, Madison believes investors could be overlooking potential opportunity in retail.

Retail’s fall from being the second-most transacted CRE sector occurred due to the synergy of secular technological disruption and one of the worst recessions and recovery cycles in modern US economic history buffeting the sector at the same time.

On the cyclical front, the Great Financial Crisis (GFC)-induced recession and the tepid recovery thereafter significantly constrained the US consumer. The labor market recovered very slowly in the aftermath of the GFC, with unemployment remaining above 5% until late 2015, all while the consumer had to repair household balance sheets damaged in the wake of the mortgage crisis and housing bust.2 While this cyclical headwind limited consumer spending and behavior, advancements in technology, including rising broadband internet penetration and smartphones, turned e-commerce into a massive commercial disruptor. E-commerce as a percent of total sales rose from 3.5% in the fourth quarter of 2007 to 11.9% just prior to the onset of the pandemic.3

Retail fundamentals buckled under the combined impact of these cyclical and secular forces. During the recession and in the years that followed retailers struggled. Big-box retailers struggled to compete with the convenience and costs of e-commerce platforms, with notable brands such as Sears, K-Mart and others liquidating, and many other large retailers rapidly reduced their location count.

Those that survived this reduction wave also grappled with a weaker consumer backdrop owing to what was at the time the worst recession since the Great Depression and an elongated recovery period. As a result, retail vacancies rose significantly, climbing 400 basis points to 11% in the aftermath of the GFC and then remained stubbornly high for several years thereafter.4 Green Street data show that Retail RevPAF, a combined metric that includes the impact of occupancy and rents, fell significantly during the cycle, declining 17.7% from 2008–12.5 Yet, these negative data points still undersell the pervasive negativity that surrounded the retail sector as headlines were punctuated with the phrase “retail apocalypse” and stores and properties seemingly closed on a daily basis as evidenced by the number of regional malls in operation cratering from a peak of 2,500 to just 700 today.6

The COVID-19 pandemic then served as an accelerant on many of these trends, weakening retail fundamentals even further. The widespread lockdowns and limitations imposed on consumer behavior created an extinction event for many retailers. Couped up inside, e-commerce activity surged from 11.9% of total retail sales to a peak of 16.5% in the second quarter of 2020.7 Foot traffic to retail sites would remain severely impaired even after lockdowns were lifted for around eighteen months as practices such as social distancing were common and there was a general public anxiety toward being in crowded spaces. The impact on retail fundamentals was swift and severe; in the aftermath of the pandemic, Strip Center REITs saw occupancy fall rapidly to levels last observed in the depths of the GFC, and RevPAF contracted 7.6% in a single year.8

However, as the economic backdrop and consumer behavior has normalized in the years that have followed the pandemic, Madison believes the outlook for retail fundamentals has shifted markedly and it is potentially time for investors to reassess the sector with fresh eyes.

The current economic growth backdrop is supportive of a strong consumer and retail demand. Unemployment is at its lowest level since the 1960s at 3.8%, and the prime-age employment ratio is at its highest levels since 2000, at 80.7%, resulting in strong wage growth measuring 4.1% year-over-year.9 Wage growth is 110 basis points higher than the pace observed just prior to the pandemic and importantly outpacing inflation, as inflation has decelerated to just 2.7% year-over-year, resulting in real wage growth of 1.4% year-over-year.10

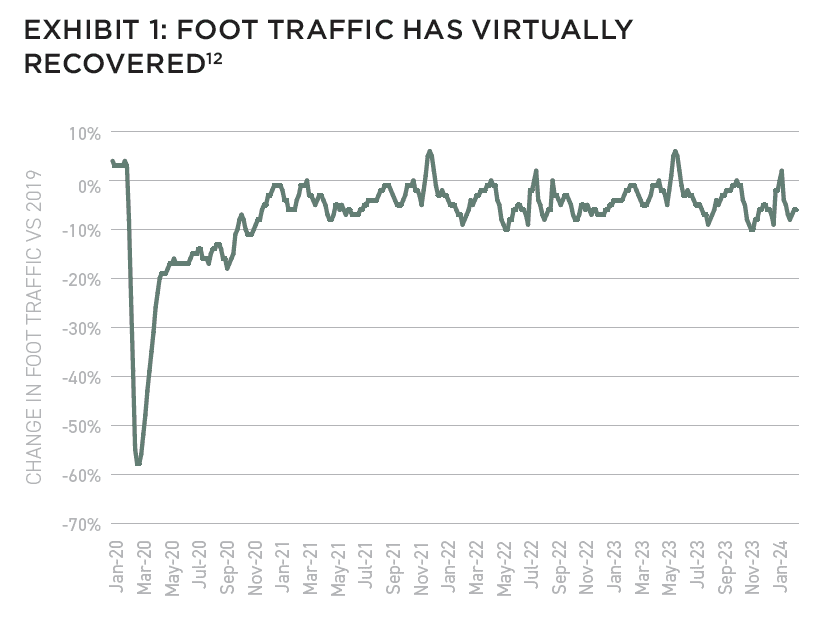

Consumer behavior has normalized in the wake of the pandemic as well. Foot traffic data from placer.ai shows that traffic levels are just marginally below their pre-pandemic norms when assessing a representative portfolio of 2,200 properties.11

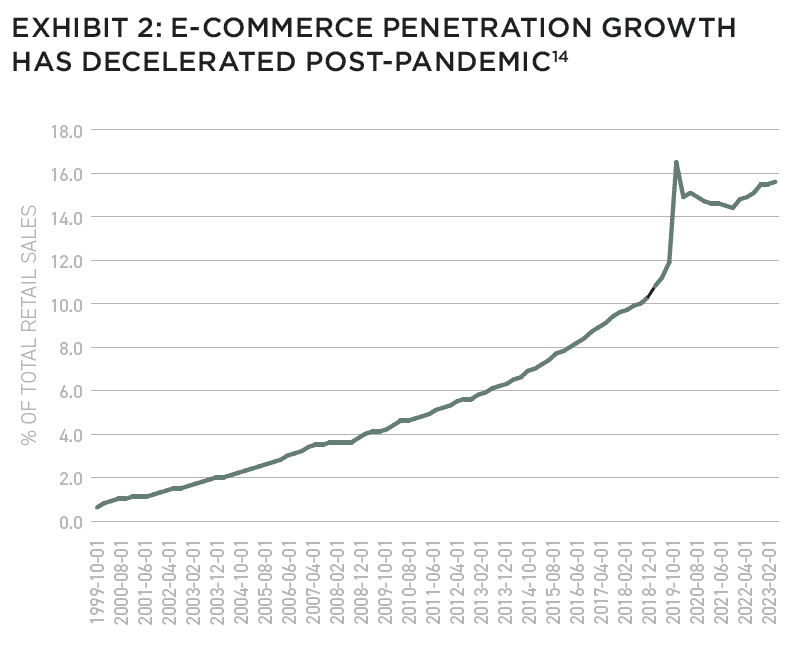

The secular headwinds have also abated. While still growing, the rise in e-commerce has decelerated in the years that have followed the pandemic-induced surge. E-commerce currently comprises 15.6% of total retail sales, still ninety basis points lower the pandemic-induced peak observed in the second quarter of 2020.

Furthermore, e-commerce penetration has only risen fifty basis points over the last year, a halving of the growth rate that was observed in the years prior to the pandemic.13 Crucially, e-commerce in some ways has become a demand tailwind for retail space, as many surviving retailers are embracing omni-channel distribution models and using retail locations as micro-last-mile fulfillment centers, and as locations for dealing with returns. This advancement in the logistics and operations of retailers blunts the go-forward impact of e-commerce cannibalization.

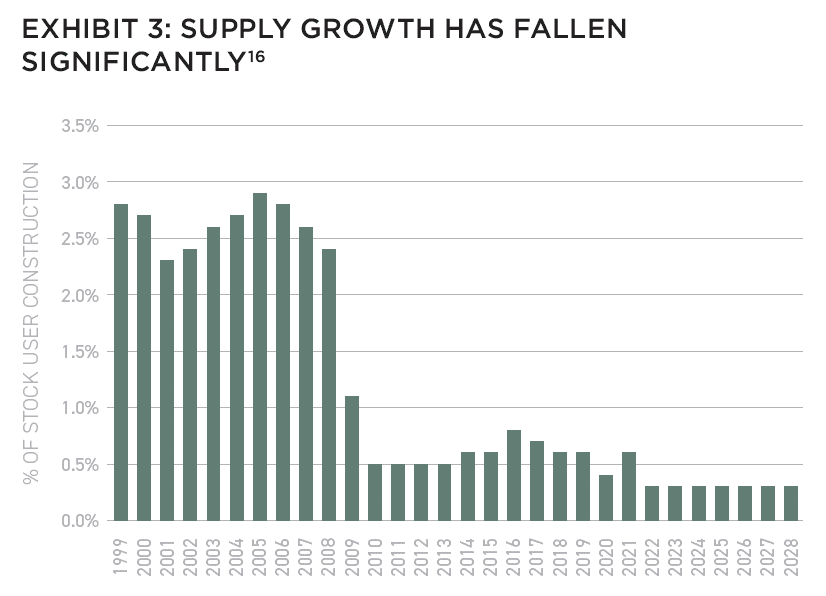

As the demand factors have turned more positive on both a cyclical and secular level, the supply landscape has become massively supportive of fundamentals growth. The decades-long disfavor of the sector among investors has led to a virtual absence of development and go-forward supply.

In the decade prior to the GFC the US saw an average 2.6% annual increase in strip center retail supply. This fell to just a 0.6% average annual supply increase in the post-GFC economic cycle as fundamentals waned. Currently, supply is expected to rise at just half that rate, 0.3% per annum, from 2024–28 as the sector’s disfavor and higher construction costs due to interest rates result in even less development activity. The lack of supply stands in stark contrast to the two most desired CRE sectors among US investors, multifamily and industrial, which are set to average 1.8% and 2% annual increases respectively over the same time horizon with some metros seeing significantly higher development pipelines than the national averages indicate.15

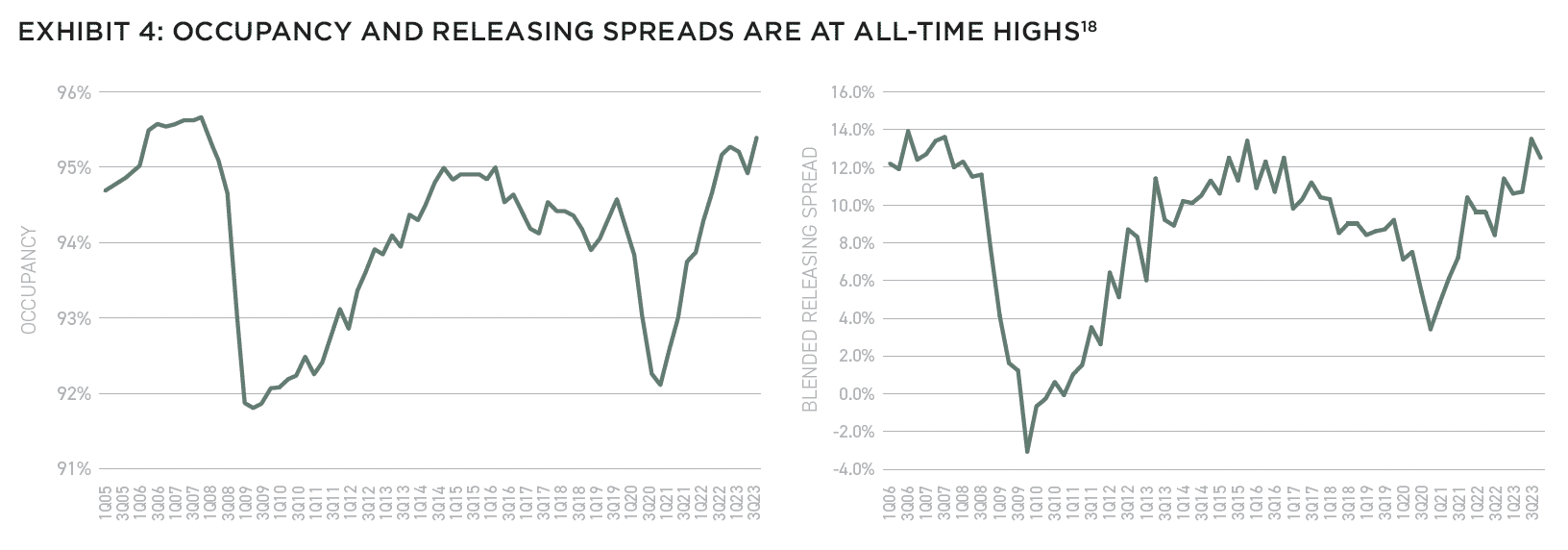

The lack of incoming supply should serve as an accelerant to already improved retail fundamentals. Strip Center Retail REIT occupancy has fully recovered to its pre-GFC level, measuring 95.4% as of Q4 2023. This is the highest occupancy level observed by the REITs since the all-time peak of 95.7% in Q4 2007. Additionally, blended re-leasing spreads measured 12.5% as of Q4 2023, on par with the peak levels observed just prior to the GFC as well.

Unsurprisingly, given the strong occupancy backdrop and lack of incoming supply, Green Street projects NOI growth of 3.1% per year through 2028 for the retail sector. While this lags other high-octane sectors, it would be the strongest five-year growth CAGR for strip center retail NOI growth in their data history, which goes back to 2001.17

Despite the seeming turnaround in the cyclical and secular backdrops, the improvement in fundamentals, and the lack of supply risk, the retail sector remains undesired by investors. In CBRE’s annual Investor Intentions Survey, just 22% of respondents noted they would target the sector for investment in 2024. This puts retail firmly behind multifamily (which 75% of investors are targeting) and industrial—two sectors currently grappling with large supply pipelines that will weigh on growth and fundamentals in the short-term.19 Madison believes in the long-term growth story those sectors offer but thinks investors should also begin to consider allocating to strip center retail as well. The scars of the past have healed and Madison believes the sector could offer compelling growth opportunities that other investors are overlooking

EXPLORE THE NEW ISSUE

NOTE FROM THE EDITOR: WELCOME TO #15

Benjamin van Loon | AFIRE

MID-YEAR CRE MARKET OUTLOOK: AFIRE

Benjamin van Loon and Gunnar Branson | AFIRE

MULTIFAMILY OUTLOOK: AMERICAN REALTY ADVISORS

Sabrina Unger and Britteni Lupe | American Realty Advisors

MULTIFAMILY GAP CAPITAL: BARINGS REAL ESTATE

Dags Chen, CFA and Lincoln Janes, CFA | Barings Real Estate

SINGLE-FAMILY RENTAL OUTLOOK: CERBERUS CAPITAL MANAGEMENT

Kevin Harrell | Cerberus Capital Management

SINGLE-FAMILY RENTAL SUPPLEMENT: YARDI

Paul Fiorilla | Yardi

LOGISTICS OUTLOOK: BRIDGE INVESTMENT GROUP

Jay Cornforth, Jack Robinson, PhD, Morgan Zollinger, and Cole Nukaya | Bridge Investment Group

DATA CENTER OUTLOOK: PRINCIPAL ASSET MANAGEMENT

Casey Miller and Ben Wobschall | Principal Asset Management

SELF-STORAGE OUTLOOK: HEITMAN

Zubaer Mahboob | Heitman Europe

COLD-STORAGE OUTLOOK: NEWMARK

Lisa DeNight | Newmark

OFFICE OUTLOOK: CUSHMAN & WAKEFIELD

David Smith | Cushman & Wakefield

RETAIL OUTLOOK: MADISON INTERNATIONAL REALTY

Christopher Muoio | Madison International Realty

HOSPITALITY OUTLOOK: JLL

Zach Demuth | JLL

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

NOTES

1. Real Capital Analytics; as of April 2024.

2. BLS via Bloomberg; as of May 2024.

3. US Census Bureau, Federal Reserve Economic Database; as of May 2024.

4. Moody’s REIS; as of May 2024.

5. Green Street; as of May 2024.

6. SiteWorks, Business Insider; as of October 2022.

7. US Census Bureau, Federal Reserve Economic Database; as of May 2024.

8. Green Street; as of May 2024.

9. Bureau of Labor Statistics, Federal Reserve Economic Database, May 2024

10. Bureau of Economic Analysis, Bloomberg; as of May 2024

11. Placer.ai, Green Street; as of April 2024.

12. Placer.ai, Green Street; as of April 2024.

13. US Census Bureau, Federal Reserve Economic Database; as of May 2024.

14. US Census Bureau, Federal Reserve Economic Database; as of May 2024.

15. Green Street; May 2024 Forecasts are inherently limited and should not be relied upon as indicative of future results

16. Green Street; May 2024 Forecasts are inherently limited and should not be relied upon as indicative of future results

17. Green Street; April 2024 Forecasts are inherently limited and should not be relied upon as indicative of future results

18. Green Street; April 2024 2024 Forecasts are inherently limited and should not be relied upon as indicative of future results

19. CBRE Investor Intentions Survey; as of January 2024.

—

ABOUT THE AUTHOR

Christopher Muoio is Head of Data and Research for Madison International Realty, a leading real estate private equity firm.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Founded in 1992, Cerberus is a global leader in alternative investing with approximately $65 billion1 in assets across complementary credit, private equity, and real estate strategies. We invest across the capital structure where our integrated investment platforms and proprietary operating capabilities create an edge to improve performance and drive long-term value. Learn more.

Principal Real Estate is the dedicated real estate investment team of Principal Asset Management, the global investment solutions business for Principal Financial Group®. As a top 10 global real estate manager, with over $98 billion in assets under management and more than 60 years of experience, we provide clients with access to opportunities across both public and private equity and debt. Learn more.