Commercial real estate (CRE) has faced significant challenges over the past two years. Rising interest rates, recession fears, and the mistaken impression that office market contagion would spread to other sectors have weighed on the asset class, pushing values down by 24.7% from their 2022 peaks.[1]

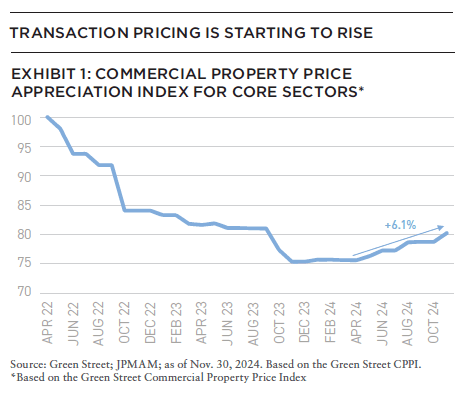

However, those concerns now appear overblown—and the challenging capital market conditions that once eroded property values are easing. Interest rates are falling. Debt is becoming cheaper and easier to secure. And transaction volumes are up by 25% from their Q4 2023 trough.[2] With most, if not all, of the asset class’s primary return drivers on the upswing, CRE prices have turned the corner, and are likely to accelerate sharply in the coming quarters. Transaction market pricing, which was roughly flat earlier in 2024, is increasing again and went up by 6.1% over the past seven months (Exhibit 1).

In our view, this shift marks the start of a generational buying opportunity for CRE, which is still pricing at a steep discount to previous peaks but continues to benefit from healthy property cash flow growth.

TRANSACTION PRICING IS STARTING TO RISE

How can we be so confident? Here, we analyze the fundamentals that will drive future performance, including falling interest rates, cheaper financing, improving liquidity, elevated occupancy, persistent cash flow growth and improving capital market conditions.

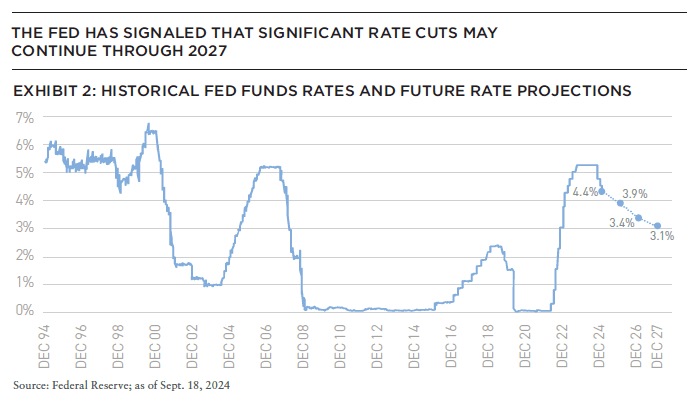

After embarking on the most aggressive rate increases since the early ’80s, the Federal Reserve (Fed) has pivoted and is now easing policy rates. The first rate cut, a larger-than-expected 50 basis points (bps) reduction, came in September, with two additional 25bps cuts coming in November and December.

Forecasts of future cuts vary, but the Fed’s internal predictions imply that rates may fall by more than 220bps from September’s peak in the coming years.

If realized, this drop would put downward pressure on cap rates.[3] This, combined with healthy fundamentals, should help real estate markets recover much of the value lost since prices peaked in the second quarter of 2022.[4]

PERSISTENT DEMAND HELPS KEEP OCCUPANCY ELEVATED

Despite recent headwinds, CRE’s underlying fundamentals remain strong. While some office assets continue to face challenges, occupancy rates across CRE remain higher than their pandemic lows, and overall occupancy is now 246bps above its long-term average.[5]

Demand is also growing. As of Q3 2024, tenants were filling more space and net absorption was positive across nearly all the major commercial real estate sectors.[6] This strong backdrop has kept net operating income (NOI) rising and, unlike previous downturns in which property cash flows fell, NOI is 6.1% above where it was when pricing peaked in the second quarter of 2022.[7]

Additionally, supply trends are improving with construction starts down between 71% and 92%, depending on the sector.[8] This will reduce deliveries of newly built properties in the coming quarters, setting up a more favorable supply/demand dynamic for owners. The improving environment should allow the industry to build on positive trends, making the short- and mid-term outlooks for property performance even better.

REAL ESTATE PRICING TRENDS ARE TURNING MORE FAVORABLE IN ALL CORNERS OF THE MARKET

The public REIT market, which has already risen by nearly 43% from its earlier trough, was the first to reflect this brightening outlook.[9] It then spread to transaction markets.

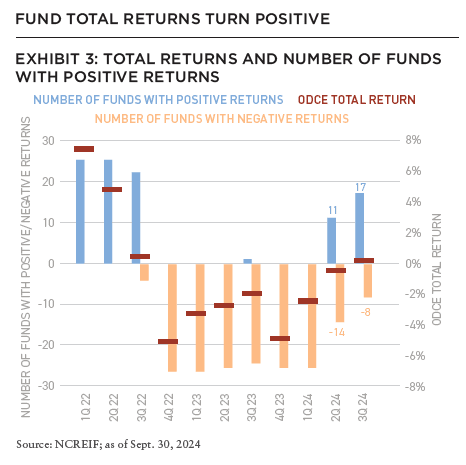

Real estate fund values, which lagged behind REIT and transaction pricing, are now also hitting an inflection point: As of the third quarter, more than two thirds of the reporting funds posted positive returns, and overall index performance was positive for the first time since 2022 (Exhibit 3).

This has set up a unique (and favorable) dynamic in which private real estate values look particularly attractive compared to other asset classes.

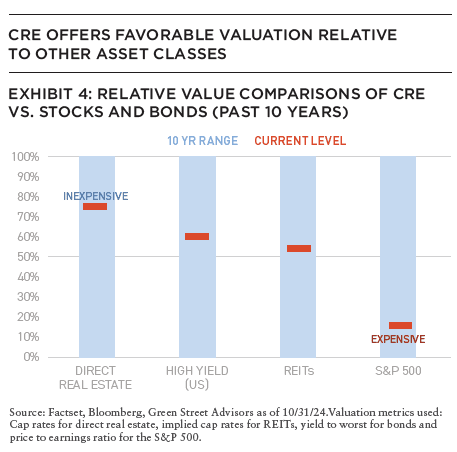

Unlike stocks and bonds, which have already experienced significant gains, real estate prices are still at or near cyclical lows. The US stock market has climbed roughly 75% since its pre-pandemic peak, lifting the price-to-earnings ratio of the S&P 500 close to some of the highest levels of the past decade.[10] Meanwhile, private real estate values are about as low as they have been during this same period (Exhibit 4).

CRE OFFERS FAVORABLE VALUATION RELATIVE TO OTHER ASSET CLASSES

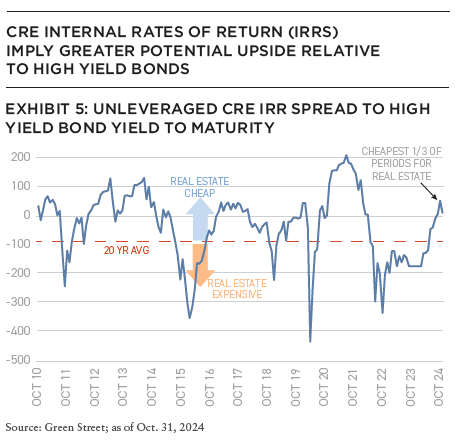

Although the difference is not as stark, the story is similar for fixed income assets. Bond yields imply less upside potential compared to CRE cap rates and—after also accounting for the appreciation component of CRE—spreads between expected CRE returns and high yield bond yields are well above long-term averages (Exhibit 5).

This represents one of the most attractive entry points for private real estate in the past twenty years.

Historically, CRE has proven resilient over time, and—given the current market landscape—it is not unreasonable for investors to expect strong gains from the asset class in the years ahead.

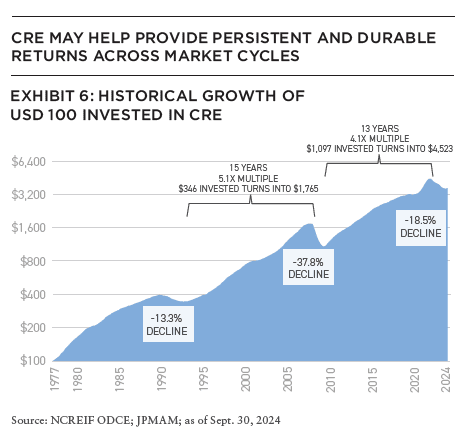

Thanks to a sizeable and stable income component, total returns for CRE stayed positive through the bursting of the dot-com bubble in the early 2000s and only saw one quarter of modest decline during the COVID pandemic (Exhibit 6).

This resiliency has not only delivered extended periods of consistent growth but has also helped diversify investors’ stock and bond portfolios, which can be more cyclical.

TIME MAY BE RUNNING OUT TO BUY INTO CRE AT CYCLICAL LOWS

However, investment timing does matter. As market transparency increases, CRE cycles appear to be intensifying and returns becoming more front-loaded. Given strong economic growth, the healthy fundamentals we see in CRE, the expectation of additional rate cuts by the Fed in the coming quarters and the sharp uptick in REIT pricing this year, private real estate values may be poised to follow a similar path.

With investor sentiment improving and leading indicators already rising, the window to invest at cyclical lows may be short. This means first movers are the most likely to benefit from what we believe could be a surge in pricing.

The current environment offers unique entry points that should not be overlooked due to negative sentiment. Investors who continue to be active in markets with steady demand, growth drivers and supply limitations will be rewarded over the next real estate market cycle.

NEW: SUMMIT #17

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

WHERE ARE WE IN THE CYCLE?: OVERVIEW OF THE US ECONOMY AND REAL ESTATE SECTOR

Richard Barkham + Jacob Cottrell | CBRE

COMPELLING OPPORTUNITIES: MAKING A CASE FOR US REAL ESTATE

Karen Martinus + Mark Fitzgerald + Max von Below | Affinius Capital

OPEN WINDOW: WHY NOW IS THE TIME TO INVEST IN COMMERCIAL REAL ESTATE

Chad Tredway + Josh Myerberg + Luigi Cerreta | JPMAM

NORMALIZING MOVEMENT: POPULATION MOVEMENTS NORMALIZING AFTER COVID-19 SHOCK

Martha Peyton + Matthew Soffair | LGIM America

CHRONIC SHORTAGE: THE US HOUSING SCARCITY WILL BE LIKELY TO PERSIST FOR SEVERAL YEARS

Gleb Nechayev | Berkshire Residential Investments

FLORIDA FOCUS: PRODUCTION INDEX BELOW 50 CURIOUSLY SIGNALS OPPORTUNITY

Rafael Aregger | Empira Group

WHOLESALE CHANGE: DEMOGRAPHIC CHANGES AND STAGNANT INVENTORY CREATE NEW OPPORTUNITIES FOR RETAIL

Stewart Rubin + Dakota Firenze | New York Life Real Estate Investors

GAME CHANGE: INFRASTRUCTURE GROWTH ACCELERATING WITH AI

Jon Treitel | CBRE Investment Management

FOR THE TREES: MASS TIMBER INTEGRATION IN INDUSTRIAL REAL ESTATE

Mary Ellen Aronow + Erin Patterson + Caroline Suarez + Cassidy Toth | Manulife Investment Management

BORDER INDUSTRIAL: INVESTING IN US/MEXICO BORDER PORT INDUSTRIAL MARKETS

Dags Chen, CFA + Lincoln Janes, CFA | Barings Real Estate

RESILIENCE AMIDST UNCERTAINTY: HOW ISRAELI AND UKRAINIAN INVESTORS ARE ADAPTING REAL ESTATE STRATEGIES DURING CONFLICT

Asaf Rosenheim | Profimex

CYBER RISK VIGILANCE: HOW REAL ESTATE DIRECTORS AND BOARDS CAN GUARD AGAINST CYBER RISK

Marie-Noëlle Brisson, FRICS, MAI + Michael Savoie, PhD | CyberReady, LLC

ALTERNATE REALTY: DIGITAL RIGHTS MANAGEMENT FOR REAL ESTATE AND AUGMENTED REALITY

Neil Mandt | Digital Rights Management + Steve Weikal | MIT Center for Real Estate

DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman + Gregory Fennell + Jon E. Linder | Dentons

HOUSING COMPLEX: CUTTING-EDGE APARTMENTS ARE A CATALYST FOR A MORE PROFITABLE FUTURE

Alejandro Dabdoub | AOG Living

NOTES

1. National Council of Real Estate Investment Fiduciaries (NCREIF). Market calculations based NCREIF – Open End Diversified Core Equity (ODCE) Fund Index; data as of September 30, 2024.

2. MSCI Real Capital Analytics, rolling 3-month transaction volume (seasonally adjusted) as of September 30, 2024.

3. A capitalization, or “cap”, rate is a property’s net operating income (NOI), revenue less operating expenses, divided by its current market value. It is commonly used to estimate the potential income return on an investment property.

4. NCREIF, ODCE Fund Index; data as of September 30, 2024.

5. Ibid.

6. CoStar, “Net Absorption for Office, Multifamily, Industrial and Retail,” data as of September 30, 2024.

7. NCREIF, ODCE Fund Index; data as of September 30, 2024.

8. CoStar, “Construction Starts for Office, Multifamily, Industrial and Retail,” data as of September 30, 2024.

9. NAREIT; Equity REIT Index total return, data as of November 30, 2024.

10. Bloomberg, FactSet, Standard & Poor’s; data as of November 30, 2024.

ABOUT THE AUTHORS

Chad Tredway is Head of Real Estate Americas at J.P. Morgan Asset Management and leads the 240-person group that manages more $74 billion of real estate assets across a range of equity and debt.

Josh Myerberg is Head of Portfolio Strategy for Real Estate America’s Open-Ended Core and Core Plus Funds.

Luigi Cerreta is Interim Head of US Real Estate Research for Real Estate Americas. He performs regional and market economic analyses that support the investment decision making process.

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

/ EXECUTIVE SPONSOR

AOG Living is a leading fully integrated, multifamily real estate investment, construction, and property management firm headquartered in Houston, Texas. AOG Living has acquired, built, or developed more than 20,000 multifamily units with a total aggregate value of over $2.4 billion and has a growing portfolio of more than 35,000 apartment homes and 170+ properties under management throughout the nation. Learn more at aogliving.com.

/ ASSOCIATE SPONSOR

Vertically integrated owner, operator, and developer of Sunbelt multifamily. Partnering with institutions on a single-asset and programmatic basis. 28k+ units acquired and developed. 62k+ units under management. 1,500+ associates. 8 Sunbelt states. To learn more, visit hrpinvestments.com and hrpliving.com. And for more information, contact john.duckett@hrpliving.com.

/ SUPPORTING SPONSOR

Affinius Capital is an integrated institutional real estate investment firm focused on value-creation and income generation. With a 40-year track record and $64 billion in gross assets under management, Affinius has a diversified portfolio across North America and Europe providing both equity and credit to its trusted partners and on behalf of its institutional clients globally. To learn more, visit affiniuscapital.com.