The real estate investment landscape is witnessing a transformative shift, driven by macroeconomic changes, evolving human needs, and technological advancements.

Within this dynamic environment, the emergence of OpCo-PropCo investment models presents a compelling opportunity for institutional investors seeking to capture value in innovative, operationally complex real estate business models that have emerged from this transforming landscape.

This article explores the evolution of OpCo-PropCo investments, elucidates the diverse investment structures, and identifies the key players shaping a handful of burgeoning sectors.

THE CURRENT CONTEXT

In recent years, traditional real estate investment paradigms have encountered limitations in accommodating the rapid proliferation of novel real estate business models. Venture capital, while adept at fostering innovation, often falls short in adequately addressing the capital requirements and risk profiles inherent in real estate ventures. The requirements include lease payments, space build-outs, furnishings, etc. The most notable example is Softbank’s efforts in funding WeWork’s growth, which led to total losses of over $14 billion for Softbank as of WeWork’s bankruptcy filing last November.1

Conversely, traditional real estate investment frameworks often emphasize stable, long-term returns, which naturally leads investors to favor investment profiles with a proven track record. These frameworks typically rely on historical performance data, established market trends, and de-risked profiles. This focus on stability can create a risk-averse environment where emerging or innovative real estate ventures, which might not have extensive performance histories, struggle to attract investment.

The convergence of these factors has catalyzed the rise of OpCo-PropCo investments, offering a hybrid approach that blends the risk appetite of venture capital with the stability of real estate investment. OpCo-PropCo investments entail the pairing of an operating company (OpCo), typically focused on technology-driven real estate solutions, with a property company (PropCo) responsible for acquiring and managing real estate assets.

OpCo-PropCo investments involve a dual-entity structure:

- OpCo focuses on the operational strategy, management, and value-add initiatives for real estate properties.

- PropCo holds the real estate assets and typically finances these assets with the capital raised from investors.

This separation allows for focused management of each entity and tailored investment strategies that meet diverse investor needs.

EXPLORING OPCO-PROPCO INVESTMENT MODELS

The landscape of OpCo-PropCo investments encompasses diverse structures tailored to accommodate the unique needs and objectives of stakeholders. Broadly categorized, these models include:

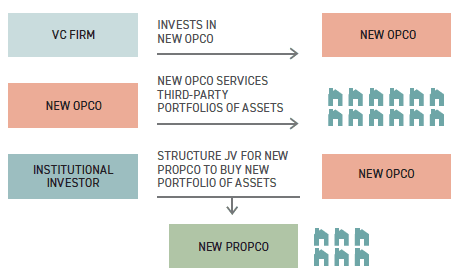

JVs with Institutional Investors

JVs (JVs) represent a prevalent approach to OpCo-PropCo investments, leveraging the complementary strengths of OpCos and institutional investors. OpCos, often equipped with innovative real estate solutions, partner with institutional investors to establish PropCos dedicated to real estate acquisition and management. This model facilitates the deployment of capital at scale while mitigating risk through shared governance structures.

Key features of JVs include:

- Alignment of Interests: One of the primary advantages of JVs is the alignment of interests between OpCos and institutional investors. By structuring partnerships around shared goals and incentives, stakeholders can collaborate effectively to pursue mutually beneficial opportunities.

- Streamlined Decision-Making: JVs streamline decision-making processes by delineating roles and responsibilities between OpCos and institutional investors. OpCos typically assume responsibility for day-to-day operations, including property management and asset acquisition, while institutional investors provide oversight and strategic guidance.

- Enhanced Access to Capital: For OpCos, JVs offer access to institutional capital, enabling them to scale their operations and pursue growth opportunities more aggressively. By tapping into institutional investor networks, OpCos can access larger pools of capital and expand their real estate portfolios more rapidly.

- Risk Mitigation: JVs mitigate risk through diversification and shared governance. By pooling resources and expertise, OpCos and institutional investors can distribute risk across multiple projects and asset classes, reducing the impact of individual market fluctuations or operational challenges.

- Flexibility in Structure: JVs offer flexibility in structuring investment arrangements to accommodate the specific needs and preferences of stakeholders. Equity stakes, profit-sharing agreements, and incentive mechanisms can be tailored to align with the risk profiles and investment objectives of both parties.

Examples of such collaborations include:

- Invesco & Mynd: Focus on single-family rentals.

- W5 & Quarters: Specialize in co-living apartment buildings.

- Saluda Grade & AvantStay: Engage in short-term vacation rental properties.

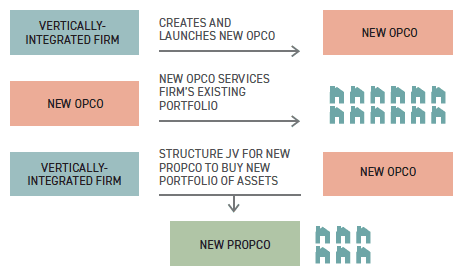

In-House Incubation with Vertically Integrated Firms

Vertically integrated real estate firms are increasingly adopting in-house incubation strategies to foster OpCo-PropCo ventures. By leveraging existing infrastructure and expertise, these firms empower entrepreneurs to develop tailored OpCo-PropCo models aligned with market demands.

Core aspects of in-house incubation include:

- Seamless Integration of Functions: In-house incubation models facilitate seamless integration between OpCo and PropCo functions, leveraging the operational synergies and economies of scale inherent in vertically integrated firms. By consolidating management and decision-making processes, these models streamline operations and optimize resource allocation.

- Direct Access to Capital: Entrepreneurs participating in in-house incubation programs benefit from direct access to capital and resources provided by vertically integrated firms. By leveraging existing funding channels and investment platforms, entrepreneurs can expedite the development and expansion of their OpCo-PropCo ventures.

- Strategic Support and Guidance: In-house incubation programs offer entrepreneurs access to strategic support and guidance from experienced real estate professionals. Mentors and advisors within vertically integrated firms provide valuable insights and industry expertise, helping entrepreneurs navigate complex challenges and capitalize on emerging opportunities.

- Potential Limitations on Autonomy: Despite the benefits of in-house incubation, entrepreneurs may encounter limitations on autonomy and decision-making authority. As subsidiaries or affiliates of vertically integrated firms, OpCo-PropCo ventures may be subject to oversight and control measures imposed by parent companies, impacting entrepreneurial freedom and flexibility.

Examples include:

- Vornado & Placemakr: Development of apartment-hotels.

- Capstone Equities & Portal Warehousing: Innovations in co-warehousing.

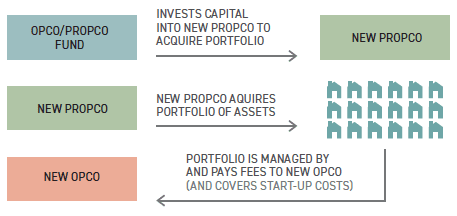

Purpose-Built OpCo-PropCo Funds

Purpose-built funds offer a holistic approach to OpCo-PropCo investments, providing sponsors with greater control and flexibility over investment strategies. By integrating OpCo financing within PropCo frameworks, these funds optimize capital deployment and maximize long-term value creation.

Key characteristics of purpose-built funds include:

- Substantial Co-Investment from OpCo Sponsors: Purpose-built funds typically require substantial co-investment from OpCo sponsors, aligning the interests of LPs and GPs and ensuring commitment to the success of OpCo-PropCo ventures. This “skin in the game” incentivizes stakeholders to pursue value-enhancing strategies and maximize returns.

- Optimized Fee Structures and Investment Horizons: Purpose-built funds feature optimized fee structures and investment horizons designed to maximize investor returns while minimizing overhead costs and administrative burdens. By aligning fee incentives with performance metrics and investment objectives, purpose-built funds enhance investor alignment and promote long-term value creation.

- Exclusive Rights and Incentives for Investors: Purpose-built funds offer exclusive rights and incentives for investors, including rights of first offer/refusal on future acquisitions, free warrants in OpCo equity, and preferential access to investment opportunities. These incentives enhance investor participation and loyalty, fostering a collaborative and mutually beneficial investment environment.

- Long-Term Hold Strategy: Purpose-built funds typically adopt a long-term hold strategy, focusing on portfolio aggregation and value creation over extended investment horizons. By prioritizing stability and sustainability, purpose-built funds mitigate short-term market volatility and capitalize on emerging trends and opportunities over time.

This model is exemplified by firms like Cloudland, which invests in emerging real estate models such as short-term rentals and workforce housing.

NAVIGATING THE DYNAMICS OF OPCO/PROPCO PARTNERSHIPS

In the world of OpCo/PropCo partnerships, structuring successful collaborations requires a nuanced understanding of control dynamics, termination clauses, exclusivity agreements, and operational alignment.

Establishing Control and Stability

The negotiation of control dynamics often revolves around two models: the discretionary model, which grants the OpCo autonomy within predefined investment criteria, and the right of first refusal (ROFR) model, which gives the PropCo veto power over each deal. Hybrid approaches that blend elements of both models can offer a middle ground, ensuring alignment while mitigating risks associated with extreme control dynamics.

Termination clauses play a pivotal role in shaping the stability and longevity of OpCo/PropCo partnerships. Setting clear conditions for termination, linking penalties to contract duration, and tailoring termination rights based on successor concerns are essential strategies for safeguarding long-term interests and fostering trust between parties.

Balancing Exclusivity and Market Dynamics

Exclusivity agreements define the boundaries of collaboration and competition in OpCo/PropCo partnerships. While exclusivity offers focus and security, it also presents challenges in navigating market dynamics and maximizing deal flow.

PropCo exclusivity serves as a cornerstone for aligning investment strategies and maximizing returns. By committing to exclusive partnerships, PropCos can streamline their investment focus and leverage their expertise for mutual benefit.

OpCo exclusivity presents a delicate balance between constraints and opportunities for growth and diversification. Finding the right balance between exclusivity and flexibility is crucial for optimizing market presence and deal flow while protecting brand integrity.

Clear boundaries through geographic or asset-specific exclusivity clauses are essential for mitigating risks and fostering collaboration. Defining the scope and duration of exclusivity agreements helps parties navigate market dynamics while safeguarding mutual interests and opportunities.

Fostering Operational Alignment and Collaboration

Operational alignment is critical for maximizing value creation and synergy in OpCo/PropCo partnerships. Proactive strategies for preempting conflicts and fostering collaboration are essential for operational success.

Comprehensive agreements detailing budgets, brand standards, and operational considerations help preempt conflicts and streamline operations. By setting clear expectations upfront, parties can mitigate conflicts and maximize value creation. Aligning investment criteria with operational goals fosters compatibility and maximizes returns. By ensuring that investment criteria align with operational objectives, parties can optimize deal flow and capitalize on synergies across the asset lifecycle.

NEW: SUMMIT #16

NOTE FROM THE EDITOR: ISSUE #16

Benjamin van Loon, CAE | AFIRE

GLOBAL CONSUMPTION: APAC DATA CENTER INVESTMENT STRATEGIES IN THE AGE OF DIGITIZATION

Michelle Lee, Eugene Seo, and Wayne Teo | CapitaLand Investment

DISTINCT VERTICALS: AI IS CHANGING THE REAL ESTATE INDUSTRY ON TWO DISTINCT PATHS

Daniel Carr and Andrew Peng | Alpaca Real Estate

DIVERGING FORTUNES: ARE COMPARISONS BETWEEN OFFICE AND RETAIL STILL WARRANTED?

Brian Biggs, CFA and Ashton Sein | Grosvenor

OCCUPYING FORCE: INSTITUTIONAL OFFICE PROPERTIES FEELING THE PAIN

Nolan Eyre, Scot Bommarito, and William Maher | RCLCO Fund Advisors

VALUE-ADD VS. CORE: COMPARING CORE AND NON-CORE STRATEGIES WITH NEW DATA

Yizhuo (Wilson) Ding | Related Midwest and Jacques Gordon, PhD | MIT Center for Real Estate

FAVORABLE CONDITIONS: STRUCTURAL CHANGES TO THE MARKET FAVOR NONBANK CRE LENDERS

Mark Fitzgerald, CFA, CAIA, and Jeff Fastov | Affinius Capital

INFRASTRUCTURE VIEWPOINT: INTEREST RATE CHANGES COULD UNLOCK NEW INFRASTRUCTURE INVESTMENTS

Tania Tsoneva | CBRE Investment Management

MISSING MIDDLE: WORKFORCE AND AFFORDABLE HOUSING IN THE US

Jack Robinson, PhD and Morgan Zollinger | Bridge Investment Group

NARROW SPACES: CHOKED STRAITS AND IMPLICATIONS FOR GDP, INFLATION, AND CRE

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

OPCO-PROPCO OPPORTUNITY: EMERGING MODELS AND THE KEYS TO STRUCTURING PARTNERSHIPS

Paul Stanton | PTB and Donal Warde | TF Cornerstone

TRANSFORMING LUXURY: UNLOCKING VALUE IN LUXURY HOSPITALITY REAL ESTATE

Alia Peragallo | Beach Enclave and AFIRE Mentorship Fellow, 2024

SOLAR VALUATION: IS SOLAR ENERGY A VALUATION GAME-CHANGER?

David Wei and Michael Conway | SolarKal

GROUND LEVEL: THE CASE FOR GROUND LEASES AND LONG-TERM CAPITAL

Shaun Libou | Raymond James

LEGAL UPDATE / DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman, Gregory Fennell, and Jon E. Linder | Dentons

LEGAL UPDATE / ENHANCED PROTECTION: LEVERAGING THE SAFETY ACT FOR ENHANCED LIABILITY PROTECTION IN REAL ESTATE

Andrew J. Weiner, Brian E. Finch, Aimee P. Ghosh, Samantha Sharma, and Sarah Hartman | Pillsbury

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

—

NOTES

1. https://www.wsj.com/livecoverage/stock-market-today-dow-jones-11-08-2023/card/wework-is-bankrupt-and-softbank-s-losses-are-14-billion-and-counting-0qi7ppzt5txbktqSgbia

—

ABOUT THE AUTHORS

Paul Stanton is a real estate investment banker and entrepreneur. He is the Co-Founder and Partner of PTB, a boutique investment bank focused on joint ventures, capital raising and M&A for innovating real estate sponsors and companies. Donal Warde is a real estate investment and technology professional specializing in the multifamily industry. As Director of Special Projects at TF Cornerstone, he leads tech initiatives to enhance operational efficiency and returns. His background in real estate investment management and tech-driven solutions reflects a commitment to innovation in the multifamily sector.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Leverage the only investment management suite that automates complex processes and ensures transparency from investor to asset operations, integrating investment and debt management, capital raising, investment, financial, and operational metrics through a branded investor portal. Learn more.