Increased remote and hybrid work is shifting occupier demand, and reducing employees’ willingness to commute, but much of that impact has filtered through the system. Portfolio right-sizing will reduce in coming years.

Cushman & Wakefield has certainly not been pollyannish about the current state and future of office in North America. Dating back to 2020, we have recognized that increased remote work would have sustained impacts on occupier demand and that the nature of office would have to evolve.1,2

We have also been realistic that some portion of existing office stock would be obsolete, that the glidepath to recovery would take some time, and that owners should be realistic about the outlook for 2024.3, 4, 5

With all that said, it is worthwhile to recognize the continued importance of the office sector to the wider US and global economies. There are still 4.4 billion square feet of occupied office space in the US, and the majority of companies with office attendance policies are utilizing hybrid structures with employees in the office several days per week in order to optimize employee productivity, corporate collaboration, and the benefits of interpersonal relationships.6, 7

Looking forward, there are several themes we are paying attention to:

- The population out-migration trends in large cities that accelerated early during the pandemic are returning to long-term norms.

- The supply-side boom is quickly unwinding, and new office deliveries will be historically low in the middle of this decade.

- Occupiers have been right sizing their portfolios, but much of the effects of increased remote and hybrid work environments have filtered through the system.

THE DEATH OF CITIES HAS BEEN OVERBLOWN

The pandemic disproportionately impacted urban cores of cities. Densely populated areas were less attractive for health reasons, and many city centers became less active due to government policy, business closings, and consumer behavior changes. This led to a well-documented increase in the net migration out of urban cores, especially in larger North American cities.

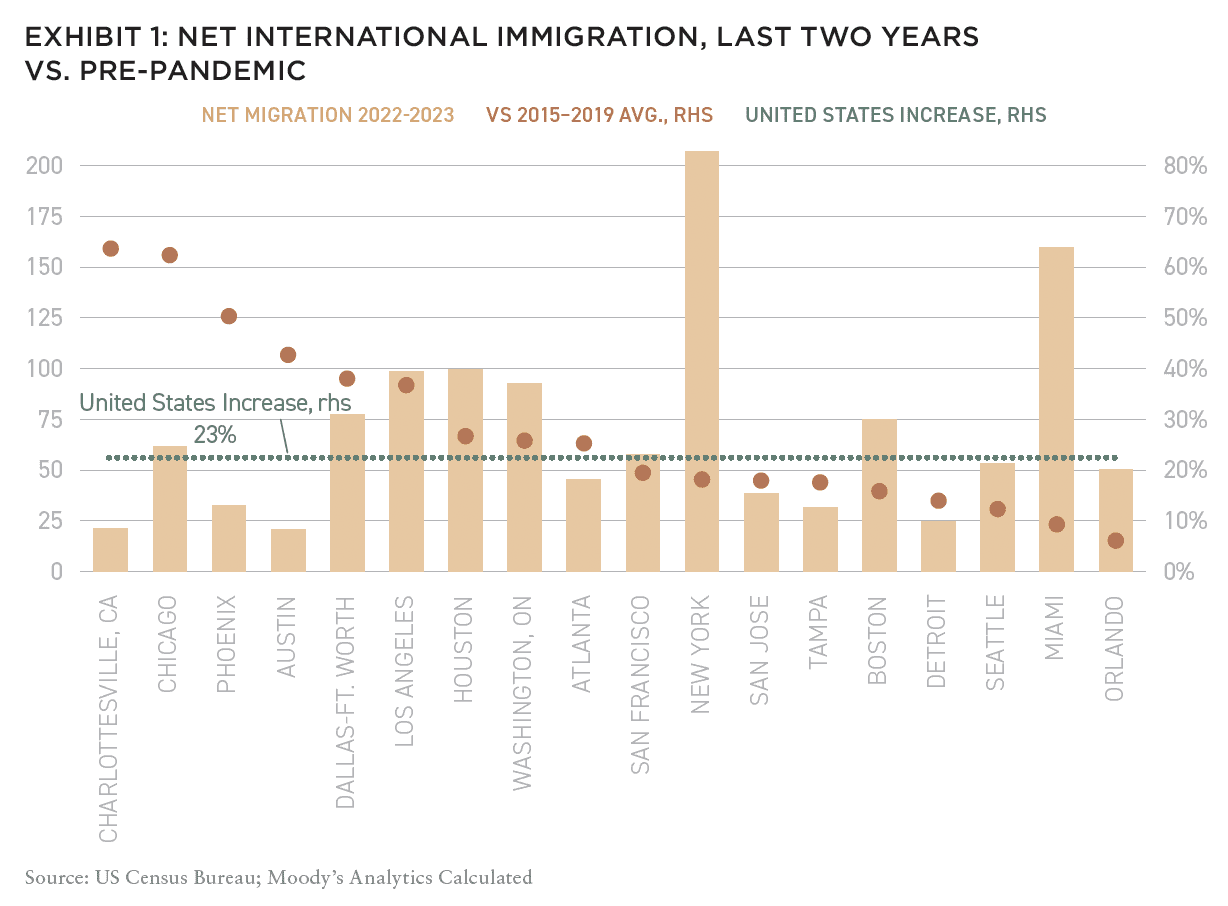

However, net migration patterns have returned from the 2020 extremes, and in some cases, look more promising for large cities than they did prior to the pandemic. For example, net out-migration is now 17% lower in the six US gateway markets than it was in 2019.8 Additionally, after decreasing for five years, net international immigration into the US nearly tripled in 2022, and 2023 was up another 14%.

The net increase in international migration of 2.1 million people over the past two years (2022–2023) is the highest two-year total since 2001–2022 and exceeds the thirty-year historical average by 20%.9 Immigration is up double digits in most of the largest US cities, which is an important development as it is a key driver of population growth in those markets.

All of this points to a recovering population trend in and around large North American cities. The urban core continues to be attractive to people looking for economic opportunity and a vibrant, diverse place to live.

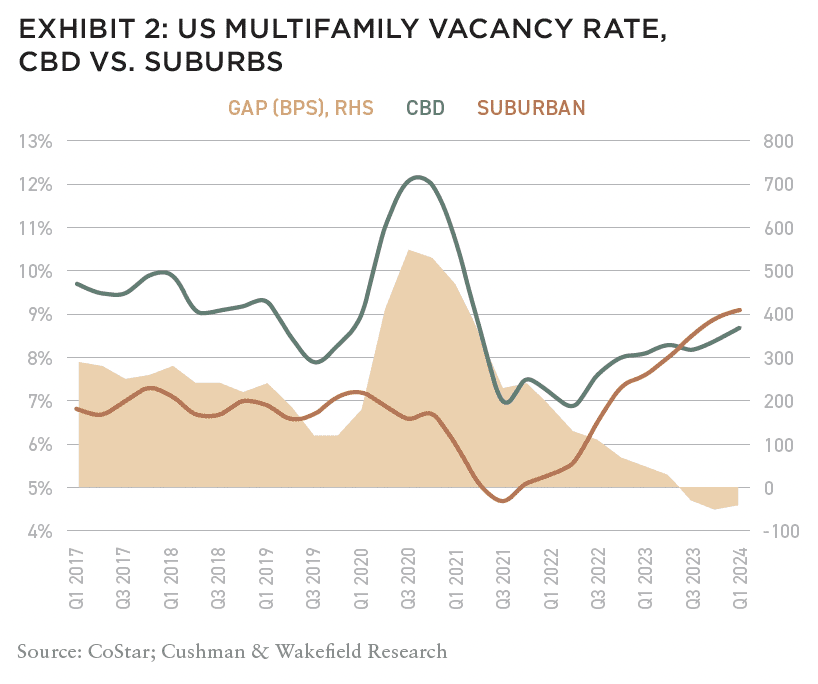

Residents have flocked back to the cities. Multifamily absorption as a share of inventory has been double that of the suburbs over the past four years (15.9% vs. 6.8%).10 National US multifamily vacancy in the CBD is currently lower than in the suburbs, which hasn’t occurred since 2012. Cities are still places where people want to live, creating demand for more conversions of office space to housing over the next decade.11

CONSTRUCTION ACTIVITY WILL SLOW DOWN OVER THE NEXT FEW YEARS

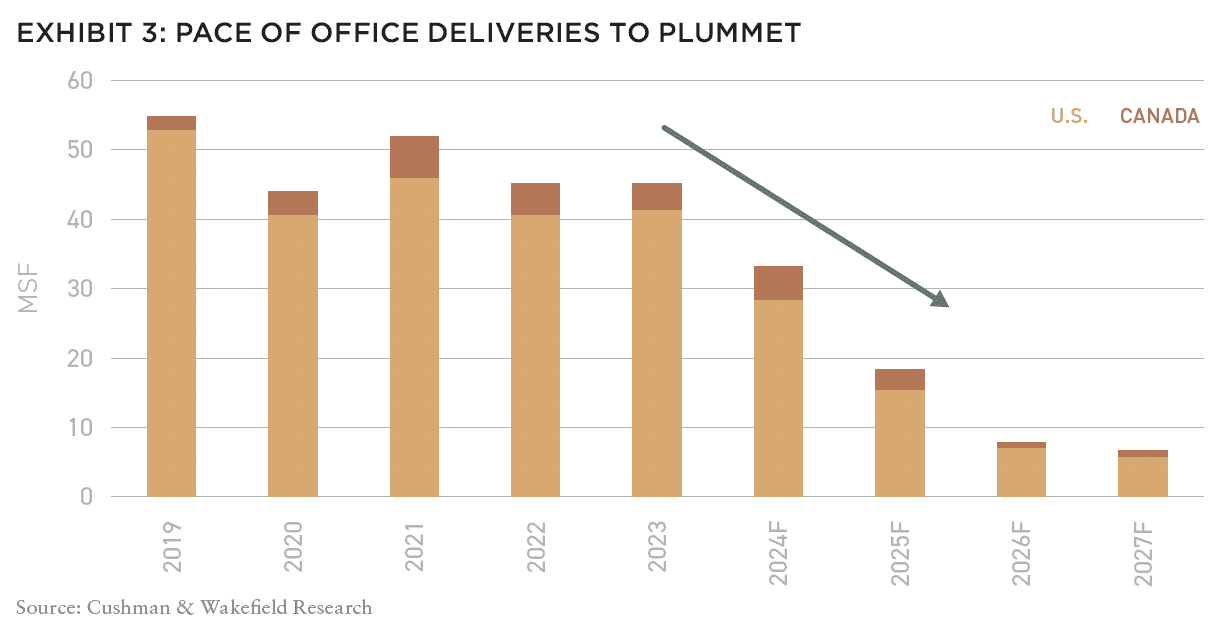

Construction activity had been gathering steam in the latter years of last decade, setting up the office market with a historically larger under-construction pipeline in early 2020. New office deliveries over the past four years have been a significant contributor to growing vacancy, with 194 million square feet of office deliveries since the beginning of 2020 (representing 3.6% of inventory).

However, due to rising construction costs, labor challenges, and high interest rates, the new construction pipeline is shrinking for commercial property types, including industrial, multifamily, and office.12, 13 The new construction pipeline is now at less than 50 million square feet for this first time since Q1 2013, and is equal to 0.9% of current inventory, down from 2.5% in 2020 and below the pre-pandemic norm of 1.5%.

Office construction activity is slowing and will continue to moderate through the middle of the decade. In fact, in the next four years, the North American office market is forecast to deliver just over a third of the space that came online since 2020 (66 million square feet vs. 185 million square feet).

The effects of this are twofold. First, occupiers will have fewer options for leases in the newest and best space since there will be so much less new construction. Second, owners will have an opportunity to fill in the high-quality office market by renovating and upgrading existing space over the next few years. Not surprisingly, the amount of office buildings undergoing significant investment and renovation has doubled since 2019.

OCCUPIERS ARE STILL COMMITTED TO THE RIGHT TYPE OF OFFICE

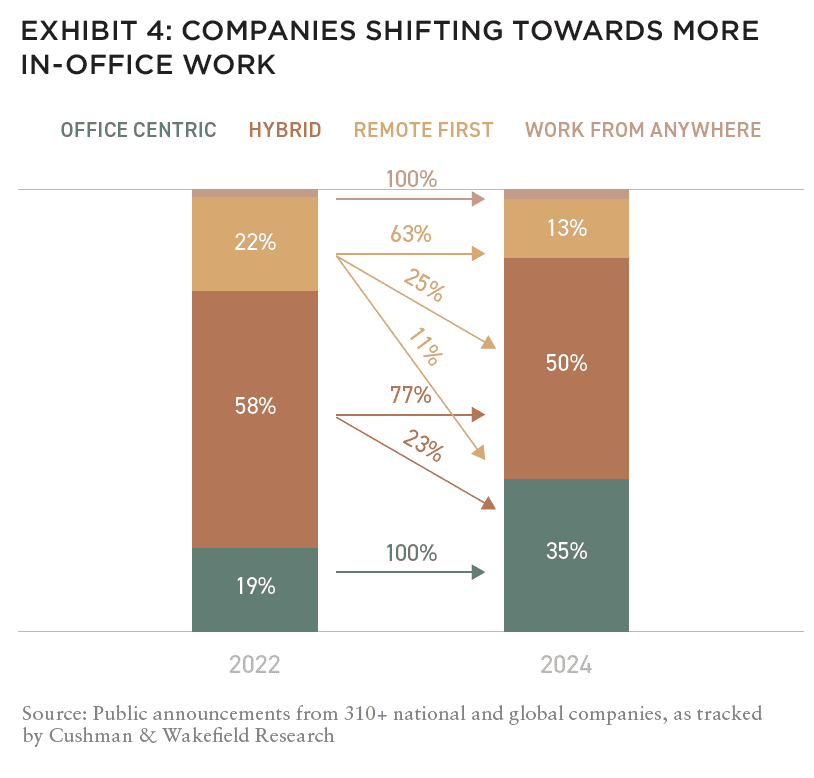

The amount of remote work is structurally higher than it was in 2019, but the majority of companies are moving forward with hybrid workplace strategies that have most employees in the office several days a week and working remotely the rest of the week. The net impact on space needs is much smaller than when employees shift to 100% remote work, and fully remote workplace strategies continue to be an outlier among North American companies.

There is reason to believe that much of the impacts of increased hybrid and remote work have worked their way through the system. Organizations with stated workplace policies are still leaning heavily on hybrid work ecosystems, with 50% of the firms tracked by Cushman & Wakefield Research currently utilizing a hybrid structure. However, that is down from 58% in 2022, and the share of companies with an office-centric workplace policy (i.e., at least three days per week in the office) has increased from 19% to 35%.

As companies change their polices, they almost always shift towards more in-office work—not less. In fact, more than a third of firms that were “remote-first” in 2022 have shifted to either hybrid (25%) or office-centric (11%) policies. A quarter of organizations that were hybrid in 2022 have shifted to be office-centric over the past two years. All of this points to the fact that we may be past “peak remote” work, as most occupiers are focused on how they optimize in-office attendance along with employee flexibility to maximize productivity, innovation, culture, and employee engagement.14

The corresponding downsizing may be nearing an end. After declining for three straight years, the average lease size held steady in 2023 (up 0.4%). And, according to a winter 2024 survey conducted in partnership between CoreNet Global and Cushman & Wakefield, the average office occupier expects to increase their overall office portfolio square footage by 0.7% over the next two years. This aligns with the Cushman & Wakefield US Macro Outlook base case scenario, which expects vacancy to peak in the near future.15

When economic uncertainty fades and office job growth picks up again, we can expect occupancy to stabilize and absorption to then turn positive.

KEY TAKEAWAYS

Cities rebounding: Some of the demographic shifts at the height of the pandemic were temporary. Said another way, people still want to live in large, vibrant cities.

Quality is king: The best office product is very much in demand. The construction pipeline has decreased by 63% since early 2020. New starts have fallen off substantially among rising construction costs and higher rates, which means that new deliveries will continue to dwindle in the coming years.16 Look for new product to continue to outperform in the coming quarters and years, and as this highly sought-after product fills up, and with little construction in the pipeline, look for demand to spillover to next highest quality tier.

Office space still critical to businesses: Occupiers are committed to the office as a part of their business strategy, even if they are offering more employee flexibility than they did five years ago. The office is still a central part of the economy and a driver of productivity, career development, culture, and innovation.

Impacts of portfolio right-sizing slowing down: Increased remote and hybrid work is shifting occupier demand, and reducing employees’ willingness to commute, but much of that impact has filtered through the system. Portfolio right-sizing will reduce in coming years.

EXPLORE THE NEW ISSUE

NOTE FROM THE EDITOR: WELCOME TO #15

Benjamin van Loon | AFIRE

MID-YEAR CRE MARKET OUTLOOK: AFIRE

Benjamin van Loon and Gunnar Branson | AFIRE

MULTIFAMILY OUTLOOK: AMERICAN REALTY ADVISORS

Sabrina Unger and Britteni Lupe | American Realty Advisors

MULTIFAMILY GAP CAPITAL: BARINGS REAL ESTATE

Dags Chen, CFA and Lincoln Janes, CFA | Barings Real Estate

SINGLE-FAMILY RENTAL OUTLOOK: CERBERUS CAPITAL MANAGEMENT

Kevin Harrell | Cerberus Capital Management

SINGLE-FAMILY RENTAL SUPPLEMENT: YARDI

Paul Fiorilla | Yardi

LOGISTICS OUTLOOK: BRIDGE INVESTMENT GROUP

Jay Cornforth, Jack Robinson, PhD, Morgan Zollinger, and Cole Nukaya | Bridge Investment Group

DATA CENTER OUTLOOK: PRINCIPAL ASSET MANAGEMENT

Casey Miller and Ben Wobschall | Principal Asset Management

SELF-STORAGE OUTLOOK: HEITMAN

Zubaer Mahboob | Heitman Europe

COLD-STORAGE OUTLOOK: NEWMARK

Lisa DeNight | Newmark

OFFICE OUTLOOK: CUSHMAN & WAKEFIELD

David Smith | Cushman & Wakefield

RETAIL OUTLOOK: MADISON INTERNATIONAL REALTY

Christopher Muoio | Madison International Realty

HOSPITALITY OUTLOOK: JLL

Zach Demuth | JLL

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

NOTES

1. Thorpe, Kevin. “Global Office Impact Study & Recovery Timing Report.” Cushman & Wakefield, September 20, 2022. Accessed May 24, 2024. https://www.cushmanwakefield.com/en/insights/global-office-impact-study-and-recovery-timing-report.

2. Cushman & Wakefield. “The Future of the Office Space.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/insights/the-future-of-the-office-space.

3. Cushman & Wakefield. “Glide Path Report.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/united-states/insights/glide-path-report.

4. Cushman & Wakefield. “Obsolescence Equals Opportunity.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/united-states/insights/obsolescence-equals-opportunity.

5. Cushman & Wakefield. “2024 US Macro Outlook.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/united-states/insights/us-macro-outlook.

6. Based on Cushman & Wakefield Research’s tracking of over three hundred companies with publicly stated workplace policies.

7. Cushman & Wakefield. “Experience per Square Foot Instant Insights: April 2024.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/united-states/insights/experience-per-square-foot-instant-insights#april24.

8. Cushman & Wakefield Research analysis of US Postal Service (USPS) Change of Address data.

9. US Census Bureau.

10. CoStar.

11. Cushman & Wakefield. “Converting Offices to Housing: What You Need to Know.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/united-states/insights/converting-offices-to-housing.

12. Cushman & Wakefield. “North American Industrial Construction Map,” January 11, 2024. Accessed May 28, 2024. https://www.cushmanwakefield.com/en/united-states/insights/north-american-industrial-construction-interactive-map.

13. Cushman & Wakefield. “Contextualizing Development Risk.” Accessed May 28, 2024. https://www.cushmanwakefield.com/en/united-states/insights/contextualizing-development-risk.

14. Cushman & Wakefield. “Experience per Square Foot Instant Insights: January 2024.” Accessed May 24, 2024. https://www.cushmanwakefield.com/en/united-states/insights/experience-per-square-foot-instant-insights#jan24

15. Cushman & Wakefield. “2024 US Macro Outlook.” Accessed May 28, 2024. https://www.cushmanwakefield.com/en/united-states/insights/us-macro-outlook.

16. Cushman & Wakefield. “US Office Fit Out Cost Guide / Highlights 2024.” Accessed May 28, 2024. https://www.cushmanwakefield.com/en/united-states/insights/office-fit-out-cost-guide.

—

ABOUT THE AUTHORS

David C. Smith is Head of Americas Insights, Global Research, for Cushman & Wakefield, a global real estate services firm.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Founded in 1992, Cerberus is a global leader in alternative investing with approximately $65 billion1 in assets across complementary credit, private equity, and real estate strategies. We invest across the capital structure where our integrated investment platforms and proprietary operating capabilities create an edge to improve performance and drive long-term value. Learn more.

Principal Real Estate is the dedicated real estate investment team of Principal Asset Management, the global investment solutions business for Principal Financial Group®. As a top 10 global real estate manager, with over $98 billion in assets under management and more than 60 years of experience, we provide clients with access to opportunities across both public and private equity and debt. Learn more.