While rate hikes and pricing dislocations have frozen CRE liquidity, there is still a significant demand for equity. These conditions create prime vintage for secondary investments.

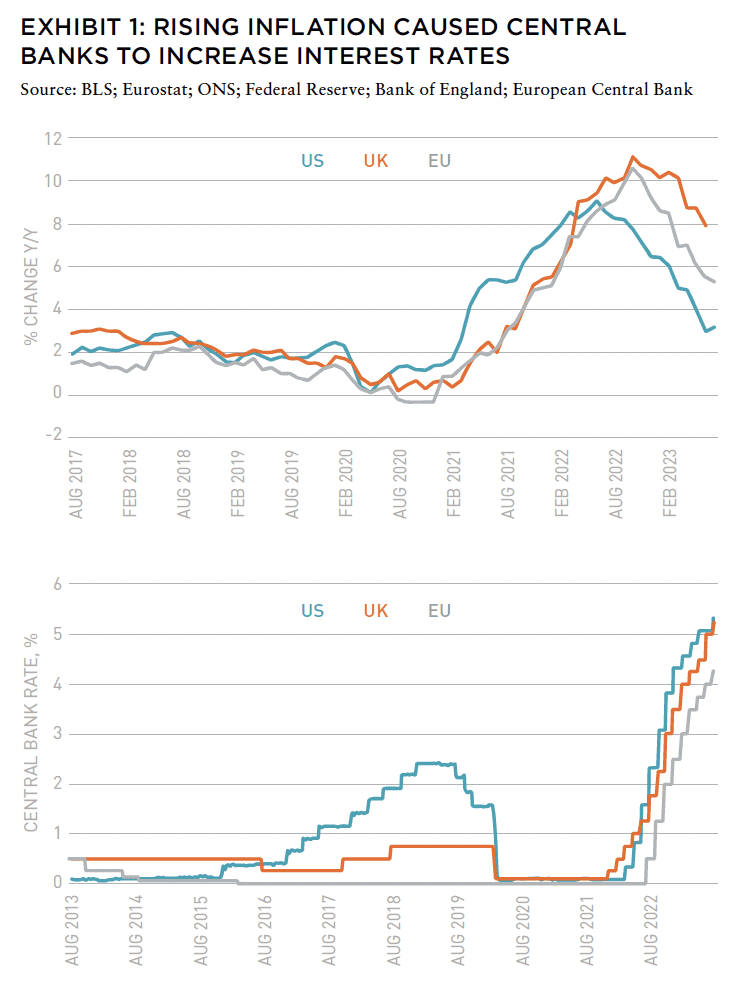

Over the last two years, global central banks have undertaken aggressive monetary policy stances in pursuit of taming the outbreak of inflation that occurred following the COVID-19 pandemic.

Major central banks such as the Federal Reserve, Bank of England, and European Central Bank have hiked rates at a pace and to levels not seen in decades. On average, the major central banks have hiked rates more than 500BPS in just over 18 months, bringing financing rates to their highest levels since pre-GFC in the US and UK and to their highest level since 2001 in the EU.1

To date, the significant re-pricing of credit has not yet appeared to have a major impact on economic growth, as the major economies have not only avoided recession, but in the case of the US, continue to grow at a strong pace with Q3 2023 GDP growth measuring 4.9%.2

However, despite the topline healthy economic backdrop, the commercial real estate (CRE) industry is clearly experiencing its own recession.

Looking solely at high-level deal volume metrics, CRE private market transaction activity in the US is at its lowest level since the COVID-19 pandemic onset in 2020, with an average of $93 billion transacting through the first three quarters of 2023. And in the EU, deal volume is at its lowest level since 2012, with an average of $40b per quarter through the first three quarters of 2023.3

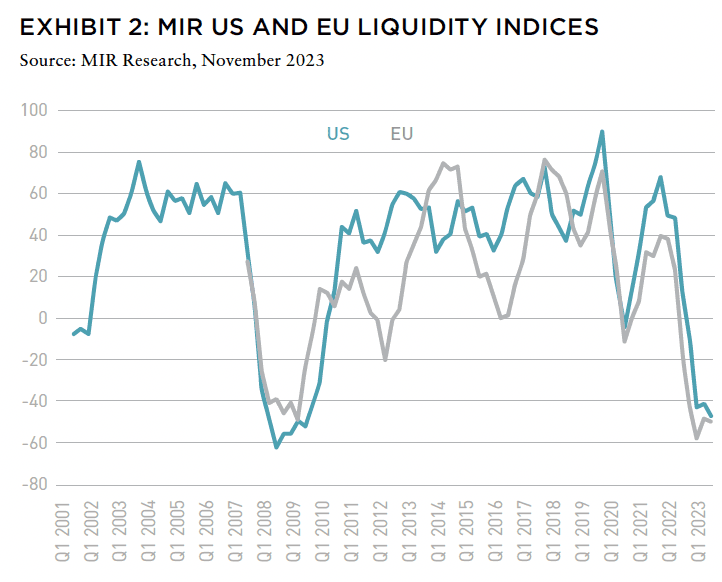

However, Madison believes the extent of the CRE recession is likely much deeper than even these metrics indicate—and is actually on par with what was observed during and following the GFC when incorporating the full mosaic of CRE capital markets data. Madison’s proprietary Liquidity Indices for the US and Europe highlight just how deep the contraction in CRE liquidity and activity has been, with both indices measuring at levels last observed during the GFC for each of the last four quarters.

These indices capture data points across a myriad of CRE capital markets including: 1) Private Market Deal Volume and Pricing, 2) Public Markets Performance, 3) CMBS Issuance, and 4) Capital Raising Performance and Trends. The indices are published on a scale of 100 to -100, with figures above zero indicating improving or healthy CRE conditions and those below zero indicating the opposite.

For example, in the case of higher-quality institutional-grade apartment properties in NCREIF portfolios, same-store expense growth has exceeded inflation over the last five-, ten-, fifteen-, and twenty-year periods.

Similar dynamics can be observed in the much broader universe of properties captured by multifamily CMBS data. Moreover, average expense growth was slightly ahead of revenues over the last five years, and it appears this will also be the case in 2023 and potentially the first half of 2024. This will put pressure on NOI growth and margins, and we see from the data that the impact varies widely across markets, subtypes, and assets.

As shown in Exhibit 2, both the US and EU Liquidity indices currently measure at levels last observed during the GFC and its aftermath. This underscores the breadth of the current freeze the new interest rate regime put in place.

However, investors continue to demonstrate the need for liquidity within the CRE space. Public REITs, which are liquid, have seen their value fall 29% from their peak as of this writing,4 handily outpacing the decline in less liquid instruments such as private CRE and non-traded REITS (NTRs), as investors have used them as a source of liquidity.

Signs of liquidity strains are also evident in large NTRs such as BREIT and Starwood’s SREIT, that began restricting investor redemption requests in November 2022 as their fund-raising levels declined significantly and redemptions requests from investors rose.

Through July 2023, NTRs raised just $8.6 billion of capital, well off the average pace of $34 billion per year they raised in each of the two years prior to rate hikes.5 Capital raising head winds are impacting other real estate vehicles as well, with Delaware Statutory Trusts (DSTs) vehicles designed for 1031 exchange investors, having raised just $2.9 billion through July, falling well below the pace of $9.2 billion raised in 2022.6

The CRE market is facing a wave of debt maturities that is also driving demand for liquidity. The US is facing nearly $500 billion in maturing commercial property loans in 2024 alone, with an additional ~$425 billion per year in maturities in the three years that follow, resulting in total maturities of over $1.7 trillion through 2027.7

The EU faces a similar cliff of debt maturities, with €235 billion of maturing debt in 2025 and an average €255 billion per year thereafter through 2028, for total maturities of €1 trillion.8

As interest rates are much higher now than when the debt was issued, Madison believes there will be a significant need for equity and recapitalization of many property and portfolio balance sheets. While the rate hikes and subsequent pricing dislocations have frozen CRE liquidity, it is clear that across structures and asset classes there is still a significant demand for liquidity and equity.

Madison believes that these market conditions are creating a prime vintage for secondary investments as a way to satisfy these acute liquidity and equity needs as they emerge. Secondaries currently account for 2% of total CRE AUM,9 but Madison believes the time is now for this proportion to grow as they serve as a vital bridge in during periods of liquidity dislocation.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #14

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: CLIMATE-RESPONSIVE REAL ESTATE INVESTMENT

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: STRIPPING THE CASHFLOW FROM THE DEAL

Paul Fiorilla | Yardi

MARKET OUTLOOK: MODEST GROWTH AND RETREATING INFLATION IN 2024

Martha Peyton, CRE, PhD | LGIM America

UNDERPERFORMANCE PARADOX: NEW RESEARCH QUESTIONS THE VALUE OF PRIVATE REAL ESTATE FUNDS

William Maher, Taylor Mammen, Ben Maslan | RCLCO Fund Advisors

NAVIGATING THE CURVE: RESILIENCE, ADAPTATION, AND PREPARING FOR 2024

Jack Robinson, PhD | Bridge Investment Group

LIQUIDITY FREEZE: POTENTIAL SOLUTIONS FOR COMMERCIAL REAL ESTATE

Christopher Muoio | Madison International Realty

SUPPLY WAVE: REASON FOR OPTIMISM IN THE MULTIFAMILY SECTOR

Sabrina Unger, Britteni Lupe | American Realty Advisors

MANAGE WHAT YOU MEASURE: UNDERSTANDING EXPENSE INFLATION IN APARTMENTS

Gleb Nechayev | Berkshire Residential + Webster Hughes, PhD | ThirtyCapital

PARSING OFFICE DISTRESS: PLANNING FOR THE NEXT GENERATION OF OFFICE SPACE

Dags Chen, Lincoln Janes, CFA | Barings Real Estat

MODEL STATES: USING ECONOMIC STATE MODELS TO ASSESS THE US OFFICE OUTLOOK

Armel Traore Dit Nignan | Principal Real Estate

OUTWARD SHIFT: WILL THE LOGISTICS SECTOR CONTINUE TO OUTPERFORM?

Kerrie Shaw | AXA IM Alts

HARNESSING THE WIND: TECHNOLOGICAL CHANGE AND THE PROMISE AND PERIL OF AI FOR REAL ESTATE

Nikodem Szumilo | University College London + Chris Urwin | Real Global Advantage

MIND YOUR DATA: REAL ESTATE INVESTING, FROM THE POINT OF VIEW OF A DATA NERD

Ron Bekkerman, PhD

OPERATING EXPENSES RISING THE OTHER MAJOR COMPONENT OF NOI GETS MORE FOCUS

Stewart Rubin, Dakota Firenze | New York Life Real Estate Investors

IN MEMORIAM: JANICE STANTON

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

ABOUT THE AUTHORS

Christopher Muoio is Head of Data and Research for Madison International Realty.

—

NOTES

1. Federal Reserve, Bank of England, European Central Bank via Bloomberg, November 2023

2. Bureau of Economic Analysis via Bloomberg, November 2023

3. Real Capital Analytics, www.rcanalytics.com, November 2023

4. MSCI RMZ Index, Bloomberg, November 2023

5. Stanger Market Pulse, July 2023

6. Mountain Dell Consulting, 1031 DST/TIC Markey Equity Update, August 2023

6. Real Capital Analytics, www.rcanalytics.com, April 2023

7. Green Street, September 2023

8. Preqin, August 2023

—