Look for select-service and luxury assets to be the most liquid, with urban markets likely to present the best opportunity to acquire quality assets given strengthening fundamental performance and a pronounced discount to replacement.

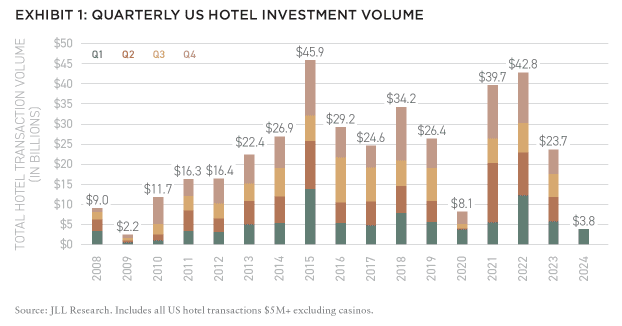

The US hotel transaction activity has been decidedly volatile in the post-COVID era. Following the initial pandemic shock in 2020, hotel liquidity reached its highest two-year total in US history, with a volume of $82.4 billion in 2021 and 2022.1

This exceeded the prior two-year high (2015 and 2016) by 10%, or $7.3 billion. This surge in transaction activity was characterized by unprecedented growth in demand for resort and leisure-heavy assets driven by strong fundamental performance. Further, investors benefitted from a favorable interest rate environment as the ten-year US Treasury averaged 60 basis points less than historical averages for much of the two-year period. This changed dramatically in mid-2022 and throughout 2023 as the Federal Reserve began its hawkish monetary tightening policies to quell inflation.

Resultantly, interest rates rose to levels not seen since before the Great Financial Crisis (GFC) which placed downward pressure on the ability of investors to transact. As such, US hotel transaction volume sunk to only $23.7 billion in 2023, a ten-year low, driven by declines in average deal sizes and historically low portfolio volumes as investors struggled to underwrite high-dollar transactions.2

While these trends have extended into Q1 2024, there is reason for optimism, with multiple catalysts on the horizon to spur increased hotel investment opportunities including:

- Discount to replacement cost

- Impending loan maturities

- Reinstitution of property improvement plans (PIPs)

- Private equity fund-life expirations

DISCOUNT TO REPLACEMENT COST

Historically, the cost-per-key for hotel development and acquisition have been in alignment; however, post-COVID supply chain disruptions combined with high labor and materials costs have led to a significant increase in the cost of hotel development. This has been most notable in urban markets where the development cost-per-key for full-service hotels soared to $742,000 in 2023, up 32% relative to 2019.

This surge in costs has created a scenario in which it is now more cost-effective for investors to buy existing full-service hotels rather than build new ones, with the differential reaching 39% in 2023.

The wide gap between the cost-to-buy and the cost-to-build presents a historically unique opportunity for investors to acquire quality assets at a meaningful discount to replacement. Look for this disparity to diminish over the medium-term with construction costs likely to decrease as supply disruptions ease and cost of materials decline.

As such, investors have a relatively short window to capitalize on the opportunity, which should lead to increased transaction activity in the coming months.

IMPENDING LOAN MATURITIES

Driven predominantly by CMBS and banks, there is a record $150 billion of US hotel loans slated to mature over the next 18–24 months. With many of those loans originated at interest rates that are materially less than those available today, look for this to be a significant catalyst of hotel transaction activity.

While these loan maturities are not expected to trigger widespread distress, it is likely that they will trigger some “forced” sales as some owners continue to grapple with lower profit-margins stemming from high operating expenses and rising property insurance costs. This will predominantly impact markets in which fundamental performance has been slower to recover, particularly those that are heavily reliant on large group business and inbound Asian travel. The latter is exceptionally important to the recovery of gateway markets as Asian travelers typically book further out, stay longer than the average domestic or European traveler, and spend more. Well-capitalized investors who are less reliant on leverage or who have access to lower costs of capital will likely be able to acquire quality assets.

REINSTITUTION OF PROPERTY IMPROVEMENT PLANS

Prior to 2020, the average US hotel was renovated every seven to ten years to ensure brand compliance and remain competitive in the market. In the immediate aftermath of COVID, when RevPAR declined more than that of 9/11 and the GFC combined, many hotel owners had to dip into their furniture, fixture, and equipment (FF&E) reserves just to make payroll.

With an uncertain timeline for recovery, and most owners singularly focused on returning to profitability, maintenance and renovation was largely ignored. Further, hotel brands were generally lenient with owners, recognizing the unprecedented financial challenges. Now, with US RevPAR fully recovered and demand continuing to surge, many brands are increasingly enforcing PIP compliance.

As some owners continue to struggle with lower profit-margins, this is yet another stress point that is likely to spur some transaction activity over the short-to-medium term. Look for hotels in urban markets, particularly larger boxes, to likely be the most impacted.

PRIVATE EQUITY FUND-LIFE EXPIRATIONS

Private equity has historically been the largest acquirer of US hotel assets, accounting for an average of 40% of annual volume over the past decade. With an average fund lifespan of seven years, groups generally acquire hotels that offer value-add opportunities to generate meaningful returns and satisfy their investors’ requirements.

Over the next two years, there is nearly $7.0 billion in closed-end funds slated to reach the exit stage of their investment lifespan. Look for this to catalyze hotel transaction activity, with quality assets likely to hit the market.

JLL expects US hotel transaction volume to accelerate meaningfully in the short- to medium-term fueled by the above four catalysts. Look for investors to increasingly target must-have assets in urban markets underpinned by rising fundamental performance fueled by the recovery of group, business, and international travel. As has been the case over the past eighteen months, expect there to be a bifurcation in investor demand, with assets on opposite ends of the spectrum—luxury and select-service—likely to garner the most interest.3

Private equity, REITs, and high net-worth individuals (HNWIs) will likely be the most acquisitive. Look for cross-border capital, which has been largely absent over the past three years, to reemerge with Middle Eastern, Asian, and select European buyers expected to reenter the market.

RENEWED INVESTOR INTEREST FOR URBAN ASSETS

It is no secret that urban hotels were the most negatively impacted in the immediate aftermath of COVID driven by widespread travel restrictions, the closure of most tourist attractions, and a lack of both business and group travel. RevPAR in many of the world’s largest cities declined by as much as 80%, with some reporting occupancies in the single digits.

Now, more than four years past the initial pandemic shock, urban hotel performance has soared underpinned by the reopening of international borders and the return of group and business demand. The former is a key demand-driver for gateway markets such as New York City, Los Angeles, San Francisco, and Washington, DC.

Although inbound international travel is expected to fully recover by the end of 2024, its composition will be different from that of pre-COVID with increased European travelers as Asian travel generally lags driven by slower border re-openings and lengthy visa wait-times.

With borders now fully reopened and visa wait-times beginning to abate, look for Asian travel to accelerate and reach a full recovery by mid-2025. Driven by this surge in performance, look for urban markets to be the most appealing for hotel investment across the US.

In fact, JLL’s 2023 Global Hotel Investor Sentiment Survey reported that 84% of hotel investors expect to deploy the bulk of their capital towards urban markets over the next twelve months.4 As asset pricing generally remains below pre-pandemic levels, expect urban hotel liquidity to increase further. Well-capitalized investors should be able to acquire quality assets.

JUXTAPOSITION OF ACQUISITION COMPOSITION

Luxury hotels and select-service assets have generally garnered the most investor interest and have been the most liquid over the past three years. Fueled by a growing HNWI population, which comprise only 0.3% of the world’s population but contribute 70% of the world’s spend on luxury travel, luxury hotel performance has soared post-COVID with many hotels generating record-high RevPAR underpinned by unprecedented average rates (ADRs).

As a result, investors have flocked to the sector, with institutional groups increasingly acquisitive driven by rising yields. Conversely, demand for select-service hotels has also surged over the past three years as Americans now have more work-related flexibility and select-service hotels offer rooms that are conducive to remote work. Further, the average cheque-size to acquire a select-service asset is 65%–75% less than that of a full-service asset, making the sector increasingly appealing to investors as interest rates have risen. Look for this juxtaposition of acquisition composition to continue over the short-to-medium-term.

PRIVATE EQUITY, REITs, AND FOREIGN INVESTORS TO BE MOST ACQUISITIVE

Private equity has raised nearly $80 billion in closed-end funds globally targeting US hotel assets over the past three years. Widespread capital market dislocation pushed many of these groups to the sidelines in 2023 but they should be increasingly active in the coming months as the market stabilizes and hotel performance continues to be robust.

Look for private equity to target both asset and platform acquisitions, particularly as hotel supply growth slows and operating companies become more valuable. Similarly, hotel REITs are expected to go on offense following three years of pruning their portfolios to shore up their balance sheets. Given their access to lower costs of capital, expect many of the US hotel REITs to be increasingly acquisitive.

Lastly, foreign capital, which has been largely absent for the past three years driven by border closures and geopolitical volatility, should reemerge as the US economy generally stabilizes and hotels have shown to be a superior hedge against inflation. With a dearth of quality product expected to hit the market in the short-to-medium-term, look for these investor types to be highly acquisitive, with must-have assets in urban and gateway markets likely to be the largest recipients of capital.

As the US hotel industry continues to defy the broader economy, with RevPAR soaring to a full recovery and remaining strong, investment opportunities should increase. Impending loan maturities, deferred capex with PIPs being reinstituted, and a high volume of private equity funds reaching the exit stage of their lifespan should all catalyze increased hotel transactions over the short- to medium-term.

Look for select-service and luxury assets to be the most liquid, with urban markets likely to present the best opportunity to acquire quality assets given strengthening fundamental performance and a pronounced discount to replacement. Investors that prioritize ingenuity and remain nimble will have the opportunity to acquire quality assets and strategically grow their portfolios.

EXPLORE THE NEW ISSUE

NOTE FROM THE EDITOR: WELCOME TO #15

Benjamin van Loon | AFIRE

MID-YEAR CRE MARKET OUTLOOK: AFIRE

Benjamin van Loon and Gunnar Branson | AFIRE

MULTIFAMILY OUTLOOK: AMERICAN REALTY ADVISORS

Sabrina Unger and Britteni Lupe | American Realty Advisors

MULTIFAMILY GAP CAPITAL: BARINGS REAL ESTATE

Dags Chen, CFA and Lincoln Janes, CFA | Barings Real Estate

SINGLE-FAMILY RENTAL OUTLOOK: CERBERUS CAPITAL MANAGEMENT

Kevin Harrell | Cerberus Capital Management

SINGLE-FAMILY RENTAL SUPPLEMENT: YARDI

Paul Fiorilla | Yardi

LOGISTICS OUTLOOK: BRIDGE INVESTMENT GROUP

Jay Cornforth, Jack Robinson, PhD, Morgan Zollinger, and Cole Nukaya | Bridge Investment Group

DATA CENTER OUTLOOK: PRINCIPAL ASSET MANAGEMENT

Casey Miller and Ben Wobschall | Principal Asset Management

SELF-STORAGE OUTLOOK: HEITMAN

Zubaer Mahboob | Heitman Europe

COLD-STORAGE OUTLOOK: NEWMARK

Lisa DeNight | Newmark

OFFICE OUTLOOK: CUSHMAN & WAKEFIELD

David Smith | Cushman & Wakefield

RETAIL OUTLOOK: MADISON INTERNATIONAL REALTY

Christopher Muoio | Madison International Realty

HOSPITALITY OUTLOOK: JLL

Zach Demuth | JLL

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

NOTES

1. All transaction volume comes from JLL Research and is inclusive of hotel transactions greater than $5 million, excluding casinos. Entity-level deals are included only if the underlying real estate traded. All data is reported in USD.

2. Excluding 2020.

3. Includes extended-stay.

4. “JLL Global Hotels Investor Sentiment Survey,” November 8, 2023. https://www.us.jll.com/en/trends-and-insights/research/jll-global-hotels-investment-sentiment-survey.

—

ABOUT THE AUTHOR

Zach Demuth is Global Head of Hotels Research for JLL Hotels & Hospitality Group.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Founded in 1992, Cerberus is a global leader in alternative investing with approximately $65 billion1 in assets across complementary credit, private equity, and real estate strategies. We invest across the capital structure where our integrated investment platforms and proprietary operating capabilities create an edge to improve performance and drive long-term value. Learn more.

Principal Real Estate is the dedicated real estate investment team of Principal Asset Management, the global investment solutions business for Principal Financial Group®. As a top 10 global real estate manager, with over $98 billion in assets under management and more than 60 years of experience, we provide clients with access to opportunities across both public and private equity and debt. Learn more.