Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Over the past decade, the US single-family rental (“SFR”) industry has matured from a largely mom-and-pop cottage business to a professionally managed, institutional-caliber asset class that fills a pronounced gap in the US housing continuum. Of course, before the GFC there were always SFR homes; however, these were typically owned and managed by individuals or small local operators, who were often more focused on near-term cash flow rather than customer service and providing a high-quality product. In fact, in 2005 there were approximately 13 million occupied SFR homes,[1] or 34% of the entire rental housing stock in the US.[2]

The GFC served as a catalyst for the institutionalization of the industry, as large and newly formed technology-enabled owner/operators were able to acquire distressed and neglected homes, renovate them to a high standard, and rent them to families looking for quality rental housing and a high level of customer service. In many instances, these operators transformed what may have been the worst home on the street into the best home on the street. This served to benefit both local homeowners, as it improved the quality of their neighborhood, and renters, who benefited from increased housing options, and served as the genesis of today’s SFR industry.

In spite of strong resident demand and high levels of customer satisfaction, the SFR industry remains very small and concentrated among a handful of operators – in fact, less than 2% of the country’s approximately 16 million SFR homes are owned by institutional owners.[3]

DEMOGRAPHIC TAILWINDS SUPPORT SFR

One of the significant drivers in the growth of the SFR industry is demographics, especially the aging of the millennial generation (born from 1981 to 1996). This cohort of 72 million people[4] fueled a major growth in demand for multifamily housing over the past 10 years and is now entering the prime period for family formation. As a result, from 2018 to 2028, more than 12 million net new households are expected to be created in the US[5] compared to approximately 10 million formed from 2008 to 2018.[6] Whereas homeownership was top of mind for many predecessor generations, a combination of tighter mortgage lending restrictions, heightened student debt, sizable down payment requirements, and the desire to spend money on experiences rather than possessions are all factors strengthening the preference of many millennials to rent homes, rather than own.

In addition to millennials, the country’s 69 million baby boomers (born from 1946 to 1964)[7] are likely to rely less and less on retirement homes, and have exhibited a strong preference to age in place. The results of a survey by the American Association of Retired Persons (AARP) in 2018 found that 76% of older Americans would prefer to stay in their existing home as they aged or move to a similar suburban home.[8] This is a primary reason why the US “mover rate,” which measures the rate at which households move to other homes, has decreased over the past several years from 13% in 2010 to 9.3% in 2020,[9] further increasing demand for suburban housing and reducing available rental supply.

These demographic tailwinds, accelerated by fallout from the COVID-19 pandemic, have led to an increased preference for detached single-family homes, which offer more indoor and outdoor space, as well as access to common suburban amenities like neighborhood parks. Even as the economy and country open back up, there has been a measurable shift toward work-from-home (either full-time or part-time), which often requires additional space for home offices or “Zoom rooms,” and a reduced need to commute every day has made certain suburbs more attractive, as residents are willing to bear a longer commute for a couple of days per week, compared with the more traditional five-day in-office workweek.

PROVIDING SFR RESIDENTS WITH SUPERIOR PRODUCT AND SERVICE OFFERINGS

The evolution of SFR from mom-and-pop to professional management has provided residents with meaningful lifestyle improvements across a number of dimensions. As SFR operations have continued to expand and evolve over the past decade, significant investment has been made in technology-enabled service offerings that are designed to save residents both time and money, while enhancing the efficiency of operating platforms.

At every step of the resident life cycle, property managers have found innovative ways to serve their residents, relieving them of many of the burdens associated with leasing or owning a home, such as:

• Leasing: Using cutting edge websites and new self-showing technology, prospective residents can lease a home quickly, efficiently and with minimal distraction. With a few clicks, residents can view detailed information on a particular home online, take a virtual tour, book an in-person home visit, and complete an application. Digital locks, facial recognition, and smart phone technology have also revolutionized the leasing experience, as residents can now enter homes using self-showing apps on their own schedule and at their own pace, without the need for a leasing agent. Many residents of SFR homes can actually go from finding a home online to move-in in a matter of days, in a predominantly “virtual” experience.

• Home Quality and Energy Efficiency: Institutionally owned and managed SFR homes are typically renovated to a high standard, and often include energy-efficient appliances, newer-vintage roofs, windows, and insulation, as well as smart home technology such as smart thermostats, leak detection sensors, smart locks, and other connected tools. These features, combined with high-grade and environmentally friendly paint, flooring, and carpets, provide residents with an incredible move-in and lifestyle experience, as if they are moving into a brand-new or freshly renovated home, with improved air quality and circulation, as well as reduced utility expenses compared to a similar vintage but unrenovated home.

• Ongoing Maintenance: In many ways, technology-enabled large-scale managers of SFR homes have revolutionized the home maintenance process. Instead of waiting for individual vendors to service homes, many large operators have built a robust staff of in-house maintenance technicians who can be dispatched on short notice to tend to day-to-day repairs. These technicians are usually very personable, have a background in home repair and construction, and are equipped with service vehicles that are well stocked with numerous parts for common plumbing, HVAC, and handyman issues. As a result, home repairs can usually be completed by one technician in a single visit, as opposed to requiring multiple visits from multiple vendors, which can cause frustration and waste valuable time for SFR residents.

• Superior Customer Service: State-of-the-art call centers in the SFR industry leveraging Interactive Voice Agents (IVA), enable residents to quickly resolve a wide range of issues, either through “self-service” functionality or by speaking to a live agent. These range from submitting a maintenance service request, to asking about a renewal notice or inquiring about moving to a larger rental home in the same neighborhood. The general goal across the industry is to achieve a high level of customer satisfaction while reducing stress and time wasted.

In many ways, renting an institutionally managed single-family home today is like living in a full-service apartment or hotel, and certainly more convenient and compelling compared to renting from a non-institutional landlord, or even homeownership in some cases. Professional property management, combined with high-quality renovations and worry-free maintenance, provides residents with more free time to spend with family and friends.

SFR: A KEY COMPONENT OF THE INSTITUTIONAL REAL ESTATE PORTFOLIO

Traditionally, the composition of an institutional real estate portfolio has relied heavily on office and retail – two sectors that continue to experience major disruptions worldwide. In fact, based on PREA’s 2020 survey data, office and retail comprised approximately 55% of portfolios, with residential making up only 23%,[10] despite the fact that the value of all single-family housing in the US (on a standalone basis) is over $35 trillion,[11] more than double the size of the traditional commercial real estate market (including multifamily, office, retail, industrial, hospitality, and others).[12]

Given current trends, recent performance, and uncertainty regarding the future usage of office and retail space, the 2021 AFIRE International Investor Survey reveals that institutional investors are keenly focused on increasing their exposure to rental housing, with 86% intending to increase exposure in the next three to five years (ranking first in the survey). Meanwhile, office and retail continue to cool.

In allocating capital to an institutional real estate portfolio, investors have historically taken the view that “residential” or “housing” is essentially 100% “multifamily rental.” However, as the SFR industry (and other housing-related industries, such as manufactured housing, student housing, and senior housing) have matured, many investors are looking at these strategies as part of an expanded “rental housing bucket.” In some instances, investors are allocating more than 30% of their capital to this sector, using this broader definition.

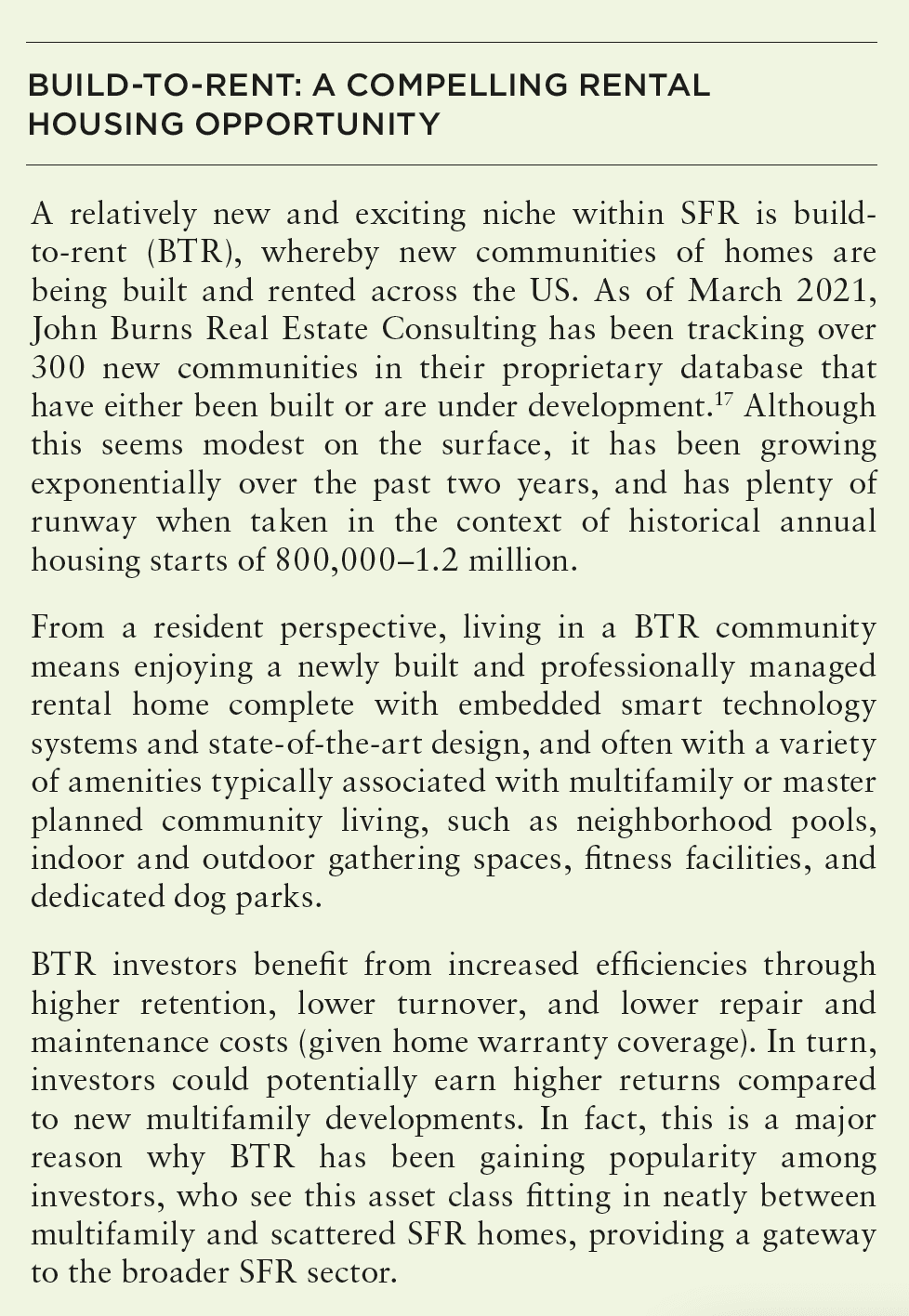

A major driver of this allocation and definition change is investment returns. Over the past five years, housing asset classes have tended to outperform other traditional real estate asset classes, with SFR (12.6% annual return over five years), senior housing (8.8%), and multifamily (5.4%) at or ahead of office (5.7%) and shopping malls (1.6%).[13] Given the large size and relative superior performance of the housing asset classes, institutional investors are likely to benefit from expanding their historical portfolio allocation to include these housing asset classes.

INCREASED CAPITAL FLOWING TO SFR

With demand for single-family housing outpacing supply, and demographic trends, combined with the recent pandemic, accelerating the appetite for suburban living in detached homes, the potential for long-term growth has continued to spark the interest of institutional investors. During the first quarter of 2021 alone, institutional equity investments or commitments to the SFR space exceeded US$6 billion. This is more than half of the US$10 billion committed to the sector over the past three years.[14] Comparatively, in Q1 2021 office and retail investment volume each decreased over 40% year over year.[15]

The stability of the housing market and predictable cash flow streams from rental income also make SFR a compelling asset class for public and private debt investors. Since the first SFR securitization in 2013, there have been 93 debt offerings for more than US$45 billion of proceeds.[16] Earlier issuances tended to be floating rate private label securitizations; however, the vast majority of recent transactions have been fixed rate. Leverage points vary by offering, but typically range from 65% to 75%, with some offerings approaching 87.5% LTV or higher. Demand for SFR securitization remains strong in 2021, with each new securitized debt issue well oversubscribed by both traditional and new investors, another example of the strong institutional demand in the sector.

A RESILIENT FUTURE

Demographic shifts, challenging homeownership dynamics and the shortage of housing inventory have continued to drive SFR demand and fuel institutional investment. The maturation and institutionalization of SFR have led to improved property management, an increase in the affordable housing stock, flexibility for American households, and the development of in- demand build-to-rent communities – all while generating strong returns to investors.

THE HOUSING SECTION

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS

—

ABOUT THE AUTHOR

Jonathan Ellenzweig is Chief Investment Officer for Tricon Residential, which owns and operates approximately 31,000 single-family rental homes and multifamily rental units in 21 markets across the United States and Canada, managed with an integrated technology-enabled operating platform.

—

NOTES

1. Drew, Rachel B. “Single-Family Rentals Have Risen to Nearly a Third of Rental Housing.” Joint Center for Housing Studies, Harvard University. October 5, 2015. jchs.harvard.edu/blog/single-family-rentals-have-risen-to-nearly-a-third-of-rental-housing

2. “America’s Rental Housing 2015: Expanding Options for Diverse and Growing Demand.” Joint Center for Housing Studies, Harvard University, December 9, 2015. jchs.harvard.edu/research-areas/reports/americas-rental-housing-2015-expanding-options-diverse-and-growing-demand

3. “US Single Family Rental (SFR) Outlook.” Green Street Real Estate Analytics. February 2021. greenstreet.com/

4. US Census Data. 2019. census.gov/data.html

5. The Joint Center for Housing Studies of Harvard University, jchs.harvard.edu/

6. “Historical Households Tables.” US Census Data. census.gov/data.html

7. US Census Data. 2019. census.gov/data.html

8. Binette, Joanne and Kerri Vasold. “2018 Home and Community Preferences Survey: A National Survey of Adults 18-plus.” American Association of Retired Persons (AARP). August 2018. aarp.org/research/topics/community/info-2018/2018-home-community-preference.html

9. “CPS Historical Geographic Mobility/Migration Graphs.” US Census Data. December 2020. census.gov/data.html

10. “Investment Intentions Survey 2021.” Pension Real Estate Association (PREA). Accessed June 22, 2021. prea.org/

11. “2020 US Housing Market Gains Were Biggest in 15 Years,” Zillow.com, January 2021

12. CoStar, costar.com/; S&P Global Market Intelligence, spglobal.com/marketintelligence/en/; Nareit Research, reit.com; Tricon Research, triconresidential.com

13. “US Single-Family Rental (SFR) Outlook, February 2021.” Green Street Real Estate Analytics. greenstreet.com/; Green Street’s SFR private-market return time series incorporates market-level HPA indices (geographic weighting based on institutional SFR ownership) with historical apartment and/or SFR nominal yields to estimate long-term unlevered total returns for private real estate owners.

14. “US Multifamily Research Brief, SFR Equity Investment Soars to New Heights in Q1 2021.” CBRE Research. Accessed June 22, 2021. cbre.com/research-and-reports

15. “US Capital Markets Figures, Q1 2021.” CBRE Research.

16. Tricon Research. triconresidential.com/

17. “Investor Mania 2.0.” John Burns Real Estate Consulting. realestateconsulting.com/investor-mania-2-0/#