When it comes to real estate investing, what do the Catholic Church, the English Monarchy, and Harvard University have in common?

Over long periods of time, each of these institutions has accumulated considerable wealth, often in large part due to the ownership of land holdings which are frequently structured as ground leases.

Ground leases are an overlooked asset class among institutional investors due to their low absolute returns, limited market depth, and lack of institutional expertise.

However, despite the latest conventional wisdom that attractive “real estate” is comprised of apartments in the Sunbelt or last-mile industrial, ground leases have been hiding in plain sight for centuries and are among the most attractive risk-adjusted real estate investments a long-term investor could make.

WHAT IS A GROUND LEASE?

Ground leases represent ownership of land and its “improvements,” such as buildings or infrastructure, and are leased by the land owner (otherwise known as the “fee owner” or “lessor”) to a leasehold owner (lessee), creating two distinct legal estates. The lessee enjoys the right to use the land as they see fit throughout the ground lease term, subject to certain use restrictions in the ground lease. In exchange, the lessee pays to the lessor periodic ground rent payments and assumes responsibility for all operating costs of the land and its improvements.

Ground leases are typically structured as triple-net leases with a 99-year lease term and inflation-protected contractual rent escalations. When the ground lease reaches expiration, ownership of any improvements on the land typically revert to the landowner unless otherwise specified.

WHY SHOULD LONG-TERM INVESTORS CARE?

Ground leases are somewhat like a fixed income instrument due to their regular, secure, long-term rental payments, albeit with inflation protection and contractual rent increases, gradual appreciation accrual as the lease approaches maturity, and long duration (ninety-nine years vs. typical loan maxing out at ten years). Furthermore, instead of a bullet payment upon maturity, ground leases instead inherit ownership of all improvements on the land.

In a typical real estate capital stack, ground lease rent payments have senior priority over the leasehold lender’s debt service payments. With this in mind, because the most senior slice of debt would typically be rated with AAA credit risk, ground leases are normally deemed to have AAA credit risk as well (or better). At the same time, Fitch assigns a AA+ credit rating to US sovereign debt, rendering ground leases effectively safer than “risk-free” bonds.

On newly originated ground leases, an investor could achieve an unlevered internal rate of return of approximately 7.5% over ninety-nine years.[1] For perpetual investors with stated long-term investment goals of achieving nominal returns of approximately 7%[2], investment exclusively in ground leases in the latest vintage would effectively guarantee meeting or exceeding that requirement for the next ninety-nine years at a risk-level safer than US treasuries and without the need to re-invest the capital for at least a century (if ever). With modest leverage, the return becomes that much more attractive without committing to materially incremental risk.

HOW WOULD GROUND LEASES FIT INTO A BROADER PORTFOLIO?

At prevailing ground lease economics, a long-term investor should manage a portfolio exclusively of ground leases. However, over an extended timeline, ground lease origination yields may range below or above long-term investors’ target returns and should therefore be considered in the context of a broader investment portfolio.

We estimate that institutional ownership of ground leases is currently less than 1% of the total addressable market[3], indicating most institutional investors surprisingly have minimal to no meaningful exposure to the asset class.

As a result, long-term investors have not optimized the risk-adjusted returns of their portfolio because ground leases have higher returns than historical fixed income strategies, albeit with negligible risk. Consequently, the substitution of ground leases with an average fixed-income strategy should both increase nominal returns and reduce risk across a traditional long-term portfolio.

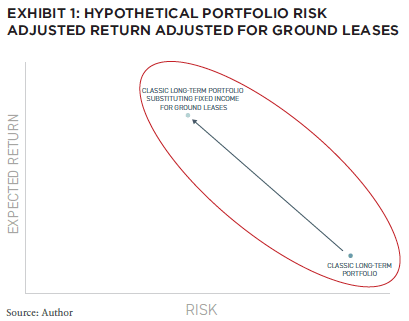

Exhibit 1 offers an illustrative example. Utilizing the twenty-year average historical returns and risk measurements of one of the largest US pension funds (the “classic long-term portfolio”), we substituted the fund’s 28.7% fixed income weighting with ground leases.

The pension’s fixed income twenty-year return of 4.3% is not only 320BPS below prevailing ground lease ninety-nine-year returns of ~7.5%[4], but also has greater historical volatility. Therefore, the substitution of ground leases for fixed income strategies should shift a portfolio’s risk and return metrics favorably.[5]

GROUND LEASES ALSO HAVE COMPELLING RELATIVE VALUE

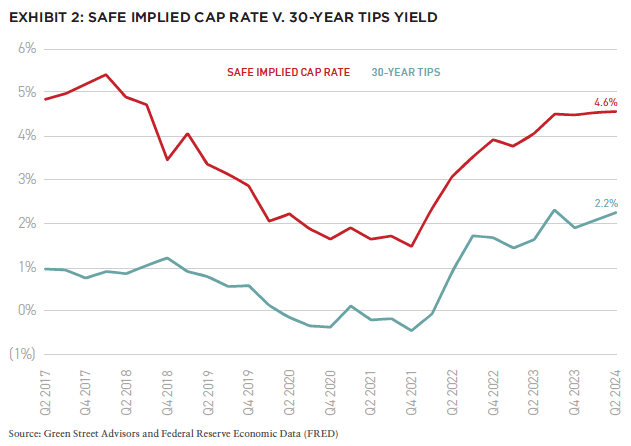

The most analogous investment products to ground leases are Treasury Inflation-Protected Securities (TIPS), as they similarly hedge for inflation and have a “risk-free” credit profile.

From 2017 to 2024, ground lease implied cap rates[6] have traded at an average 261BPS spread to thirty-year US TIPS (Exhibit 2) despite ground leases’ (1) comparable credit risk and inflation-linked increases[7], (2) minimum contractual rent increases regardless of inflation, and (3) gradual appreciation capture over the course of the lease term.

In this context, ground leases are a highly attractive investment structure on a relative basis, notwithstanding their compelling risk-adjusted nominal returns.

While TIPS’ enhanced liquidity could justify a tighter return than a typical ground lease, we do not believe the liquidity premium is large enough to justify the wide yield spread to ground leases.[8]

US TREASURY YIELDS REMAIN ELEVATED

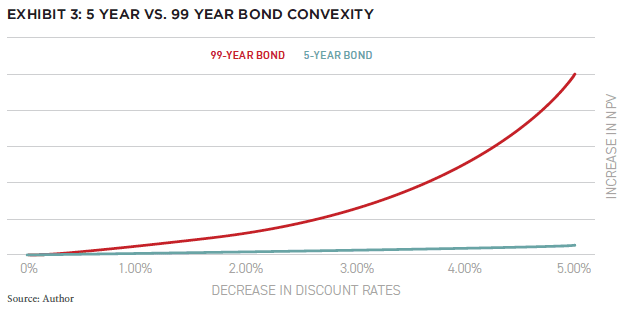

Within the past twelve months, the thirty-year US treasury yield reached levels not seen since 2009 and 2010. The US treasury is the base rate on which ground leases price, and their elevated yields allow ground lease originators to lock in high cap rates (the ground lease proxy for “interest rates”) for ninety-nine years. With such long duration, ground leases have extremely high “convexity”[9] – in other words, their valuations are highly sensitive to fluctuations in interest rates.

As we face a backdrop of declining rates based on the latest Fed dot plot (which forecasts a 225BP drop through 2026[10]), ground leases originated in this environment stand to appreciate significantly. On the other hand, if rates rise or remain steady, a status quo or reduction in valuation would be mitigated by increased cash flows from annual rent escalations and CPI adjustments. Of course, while we believe 2024 will be a strong vintage for new ground lease origination, a prudent investor should carefully dollar cost average their bets in any sector to mitigate vintage risk.

Exhibit 3 demonstrates the sharp contrast in convexity between a ninety-nine-year ground lease vs. a five-year bond. In this example, a 100BP decline in the discount rate would mean 24% appreciation of the ground lease, in contrast to approximately 4% appreciation of the five-year bond.[11] Exhibit 3 illustrates this relationship across a range of discount rates.

WHAT IS THE MARKET OPPORTUNITY?

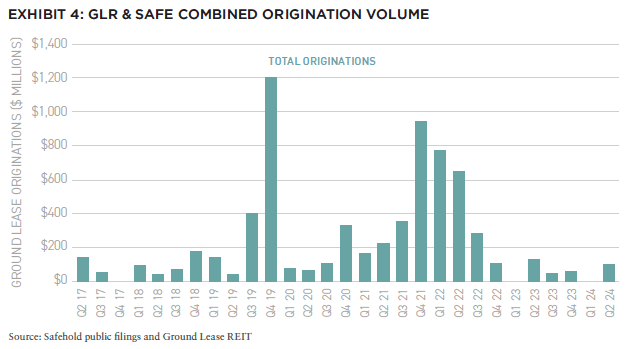

Although the addressable ground lease market is robust, existing ground lease stock in the US is scarce and the marketplace is opaque. Outside of the publicly traded stock of Safehold (NYSE: SAFE), the secondary market for ground leases is effectively non-existent because those who originate ground leases often do so to hold them through maturity or perpetually (via regular lease extensions).

Because of these blurry market dynamics, the primary means to build a scaled ground lease portfolio is by direct origination. This realization ultimately crafted the business models of the two largest and well-known pure-play ground lease originators in the space: (1) Safehold ($6.2 billion ground lease portfolio)[12] and (2) Ground Lease REIT (GLR)[13] (~$1 billion ground lease portfolio).[14] Despite the involvement of institutional players, the sector remains nascent, with estimated 2023 origination volume representing <1% of the 2023 transaction volume of a mainstream sector like multifamily.[15] Exhibit 4 shows the historical ground lease origination volume of Safehold and GLR combined since 2017.

Whereas traditional ground leases were often originated as bespoke, brokered solutions between landowners and, usually, developers in a dense urban area, the modern ground lease is more akin to an alternative financing tool. In fact, in a modern ground lease transaction, the developer often voluntarily creates a ground lease via a sale-leaseback of the land to a ground lease originator in exchange for financing proceeds.

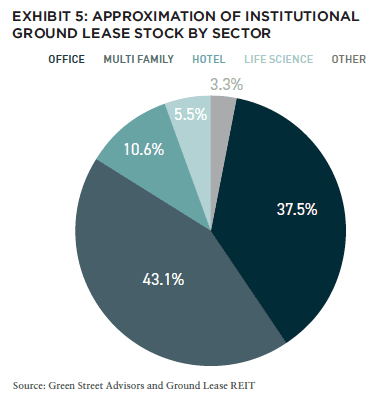

Like debt, sector selection and credit strength play a meaningful role in deal origination and portfolio construction. Per data from Safehold and GLR over the past twelve months, of the eleven completed transactions, 100% were in multifamily with average GLTV of 34.9% and rent coverage of ~3.0x. Multifamily remains the collateral of choice for ground leases, yet Safehold and GLR’s combined portfolios are diversified across sectors, as presented in Exhibit 5.

Among these recently originated ground leases, a meaningful portion served as financing for development projects. As compensation for the incremental risk, originators typically seek a 50BPS+ spread to those ground leases with stabilized collateral. Whether the additional yield is worth the risk of new development is a debated topic in the ground lease industry. We firmly believe the additional cap rate spread justifies the risk of development. Aside from the facts that the ground lessor will have brand-new collateral, robust lender-like protections and a highly defensible “last dollar” basis, a 50BPS spread on an otherwise 5% cap rate would increase the origination yield by 10% and ninety-nine-year ground lease multiple on invested capital (MOIC) by ~1.5x[16] for “risk” that likely only exists for around three out of ninety-nine years of term.

SEE YOU IN A CENTURY

The United Nations projects that by 2054 the number of centenarians will reach a record four million globally, likely to grow further by 2124 (when today’s ground leases will expire).

For those long-term investors out there, consider a ground lease investment. Perhaps we’ll catch up in a hundred years to see how it turned out, and we’ll be waiting with those same centuries’ old institutions who prudently invested in ground leases.

NEW: SUMMIT #16

NOTE FROM THE EDITOR: ISSUE #16

Benjamin van Loon, CAE | AFIRE

GLOBAL CONSUMPTION: APAC DATA CENTER INVESTMENT STRATEGIES IN THE AGE OF DIGITIZATION

Michelle Lee, Eugene Seo, and Wayne Teo | CapitaLand Investment

DISTINCT VERTICALS: AI IS CHANGING THE REAL ESTATE INDUSTRY ON TWO DISTINCT PATHS

Daniel Carr and Andrew Peng | Alpaca Real Estate

DIVERGING FORTUNES: ARE COMPARISONS BETWEEN OFFICE AND RETAIL STILL WARRANTED?

Brian Biggs, CFA and Ashton Sein | Grosvenor

OCCUPYING FORCE: INSTITUTIONAL OFFICE PROPERTIES FEELING THE PAIN

Nolan Eyre, Scot Bommarito, and William Maher | RCLCO Fund Advisors

VALUE-ADD VS. CORE: COMPARING CORE AND NON-CORE STRATEGIES WITH NEW DATA

Yizhuo (Wilson) Ding | Related Midwest and Jacques Gordon, PhD | MIT Center for Real Estate

FAVORABLE CONDITIONS: STRUCTURAL CHANGES TO THE MARKET FAVOR NONBANK CRE LENDERS

Mark Fitzgerald, CFA, CAIA, and Jeff Fastov | Affinius Capital

INFRASTRUCTURE VIEWPOINT: INTEREST RATE CHANGES COULD UNLOCK NEW INFRASTRUCTURE INVESTMENTS

Tania Tsoneva | CBRE Investment Management

MISSING MIDDLE: WORKFORCE AND AFFORDABLE HOUSING IN THE US

Jack Robinson, PhD and Morgan Zollinger | Bridge Investment Group

NARROW SPACES: CHOKED STRAITS AND IMPLICATIONS FOR GDP, INFLATION, AND CRE

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

OPCO-PROPCO OPPORTUNITY: EMERGING MODELS AND THE KEYS TO STRUCTURING PARTNERSHIPS

Paul Stanton | PTB and Donal Warde | TF Cornerstone

TRANSFORMING LUXURY: UNLOCKING VALUE IN LUXURY HOSPITALITY REAL ESTATE

Alia Peragallo | Beach Enclave and AFIRE Mentorship Fellow, 2024

SOLAR VALUATION: IS SOLAR ENERGY A VALUATION GAME-CHANGER?

David Wei and Michael Conway | SolarKal

GROUND LEVEL: THE CASE FOR GROUND LEASES AND LONG-TERM CAPITAL

Shaun Libou | Raymond James

LEGAL UPDATE / DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman, Gregory Fennell, and Jon E. Linder | Dentons

LEGAL UPDATE / ENHANCED PROTECTION: LEVERAGING THE SAFETY ACT FOR ENHANCED LIABILITY PROTECTION IN REAL ESTATE

Andrew J. Weiner, Brian E. Finch, Aimee P. Ghosh, Samantha Sharma, and Sarah Hartman | Pillsbury

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

—

NOTES

1. Safehold’s (NYSE: SAFE) published “Economic Yield” on six new ground lease investments originated in 2Q 2024. All six transactions have multifamily leaseholds.

2. A simple average of stated long-term investment targets of California Public Employees’ Retirement System, California State Teachers Retirement System, New York Employees’ Retirement System, New York State Teachers’ Retirement System, and Teacher Retirement System of Texas.

3. Allaway, Spenser. Safehold (SAFE): Breaking Ground. Green Street Advisors, 2022.

4. The institutionalized ground lease market did not exist in 2004. Ground lease originations in 2Q 2024 are an appropriate and conservative proxy for those that could have been issued in 2004 because the 30-year treasury (the benchmark rate for pricing ground leases yields) in 3Q 2004 was ~57 bps higher than in 2Q 2024 on average.

5. Trust Level Review. CalPERS, 2024. This graphic utilizes CalPERS’ publicly available historical return and risk metrics to evaluate what CalPERS’ historical risk and return of their portfolio over the past 20 years could have been if the fund invested in ground leases in lieu of fixed income. The analysis represents an approximation of what such change could look like but is imperfect due to limited (1) detailed information available about the underlying positions in the CalPERS portfolio and (2) return / risk disclosures over the same measurement window.

6. Data per Green Street Advisors and based on the public trading of the only dedicated ground lease REIT, Safehold (NYSE: SAFE).

7. Most ground leases have a limit on the amount of rent increases as a result of inflation, though these limits are usually in-line with or above U.S. long-term average inflation.

8. Over the past 15 years from 2009 to 2024, the delta between Green Street’s nominal and implied real estate cap rates is 32 bps, which offers a helpful proxy for a real estate liquidity premium. Utilizing this premium, the liquidity adjusted spread between 30-year TIPS and ground leases would decline from 261 bps to 229 bps.

9. Convexity is a measure of the non-linear relationship of bond prices to changes in interest rates.

10. Federal Reserve Board summary of economic projections

11. This analysis compares the net present value of the future cash flows of a 5-year bond with 5% coupon and 99-year ground lease with a 5% coupon (and no annual rent escalation to keep the comparison apples-to-apples), each discounted at discount rates of 5% and 4%.

12. Aggregate cost basis per Safehold’s 2Q24 investor presentation.

13. Ground Lease REIT is a privately held real estate investment trust, externally managed by private equity firm Montgomery Street Partners.

14. Ground lease portfolio values reflect funded and/or committed proceeds at cost as of quarter-end of 2Q 2024.

15. ~$61.5 billion of aggregate multifamily transaction volume in 2023 per Green Street versus ~$233 million of institutional ground lease originations (see Exhibit 4)

16. This analysis calculates the delta in MOIC between two ground leases through their 99-year term with 2% annual rent increases that are identical in all ways except the entry cap rate.

—

ABOUT THE AUTHORS

Shaun Libou is a Director of Raymond James, a client-focused global financial services company providing wealth management, capital markets, asset management and other tailored services.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Leverage the only investment management suite that automates complex processes and ensures transparency from investor to asset operations, integrating investment and debt management, capital raising, investment, financial, and operational metrics through a branded investor portal. Learn more.