Insatiable appetite for data throughout the APAC region is fueling growth of this new economy asset class. And as demand for digital services continues to accelerate globally, the importance of the sector will grow in kind.

From 5G mobile to Zoom conferencing, and from TikTok to video streaming, global consumption and processing of digital products continue to accelerate, leading to surging demand for new data center (DC) capacity for data to be stored and processed.

While cloud computing is today the primary driver for DC demand, the rise of AI learning and applications has become an additional demand driver. As operators prepare for an explosion in AI uptake, they have therefore embarked on a huge buildout of capital-intensive infrastructure to host the large number of specialized semiconductors the technology requires. In addition, there has been rapid expansion into peripheral locations able to offer both land and power resources required to accommodate escalating infrastructure needs.

The revolution in the scale at which data is being used and managed is fundamentally a global phenomenon, but nowhere is it unfolding as rapidly as in Asia Pacific (APAC) markets. Regional economies are not only growing faster and from a lower base, but they also have a cultural affinity for digitized business and technology adoption. In addition, the multitude of distinct regulatory jurisdictions across the region means data users must comply with a larger number of country-specific data protection policies compared to the West, driving a shift towards greater data localization. Together, these factors are creating new opportunities for early-stage investment in what remains an emerging regional asset class.

Demand in the APAC region is equally strong for both dedicated and colocation DCs. Singapore, Tokyo, Osaka, Seoul, and Sydney are identified as key markets for new DCs, with the major Indian cities of Mumbai, Bengaluru and Chennai also showing promise due to growing digital services sectors, strong government support, and robust long-term economic prospects.

The US model of workforce and affordable rental housing is unique relative to international affordable housing models, which are often deeply subsidized by public funds and targeted towards the lowest-income households, in that the US system serves a broad range of income levels.

AN ESSENTIAL REAL ASSET: DATA CENTERS IN A THRIVING DIGITAL ECONOMY

Soaring global demand for data storage and processing is making DC infrastructure a key component of the ongoing fifth industrial revolution, driven primarily by surging AI requirements and the adoption of cloud services.1 As a result, network providers and technology multinationals are now churning out ever-larger new facilities to accommodate expanding data storage and processing infrastructure.

While industry growth is strong globally, this revolution is more apparent in APAC markets, where DCs have emerged as a critical asset class for institutional investors.

1. NAVIGATING THE TRENDS DRIVING DC DEMAND

Secular and structural drivers

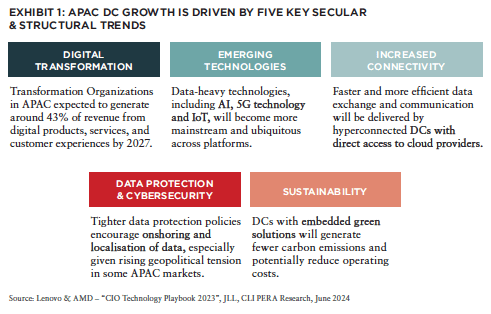

Rapid growth in global data consumption and processing are the main demand drivers for new DC capacity and services. They are a product of several secular trends:

- Surging consumption of digital content, including videos, social media and music

- Widespread adoption of digital communications platforms – a trend expedited by the pandemic

- Development of smart cities2

- Ongoing expansion of the digital economy

In addition, demand from global technology players, as well as growing digitization among businesses, are also boosting appetite for cloud adoption and digital services. Finally, cloud operators are expanding their range of software services to attract and retain customers, including via managed cloud, private cloud, and cybersecurity applications used for risk management.

Cusp of an AI-driven revolution

Even as appetite for cloud-based digital services continues to grow, the recent emergence of AI has now become the industry’s truly disruptive force, with the explosion of AI-enabled services following the introduction of ChatGPT in late 2022, creating a new catalyst for higher bandwidth and cloud-hosting DC infrastructure.3

The market for generative AI is projected to experience a remarkable 32-fold increase over the coming decade alone, driven by the development and uptake of AI across the global economy.4 In particular, given the proficiency of generative AI in producing significant quantities of content, businesses focused on creating analytical or creative material are likely to be key consumers of these new services.

The large number of new graphics processing units (GPUs) required for training generative deep-learning AI models has increased the size and energy intensity of associated IT infrastructure, fueling demand for a new generation of high-capacity, cutting-edge DC facilities. The snowballing size of new DC facilities and campuses, with the majority constructed with capacities in the 20MW to 50MW range—and some exceeding 100MW—is significantly greater than the 10MW to 20MW DCs commonly seen in previous development cycles. Such notable increases in capacity are in turn encouraging innovation in the design, management, and outfitting of new DC facilities.

2. THE GOLDEN OPPORTUNITY IN APAC

World’s largest colocation market

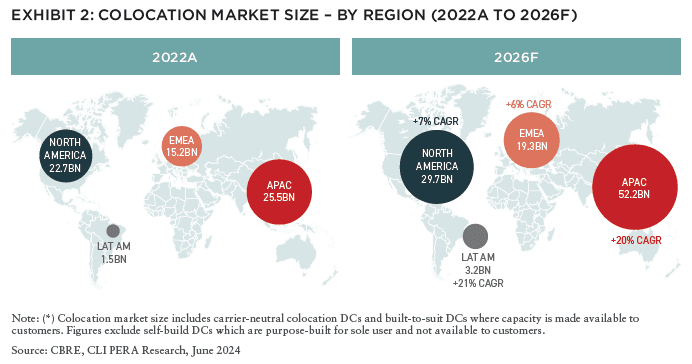

Colocation DCs are fully fitted facilities designed to host multiple customers, including cloud players and small and large enterprises. The APAC colocation market represents 39% of the global total and has an estimated value of $26 billion, making it by far the world’s largest. It is expected to double in size by 2026, as APAC digital organizations continue to expand significantly faster than their peers in the Americas and EMEA. To achieve this, a significant volume of new investment will be needed in both dedicated and colocation DCs.5

APAC’s demographic advantage

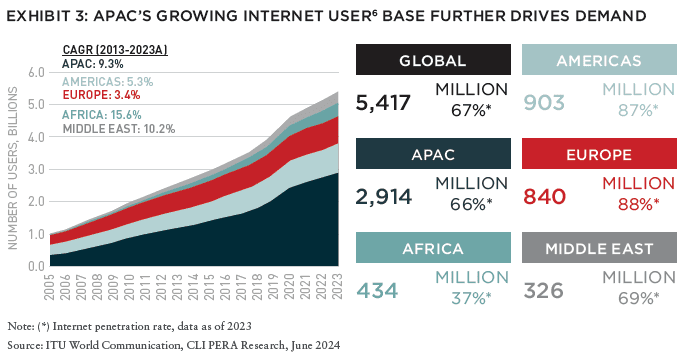

APAC’s enormous population and swelling internet user base cement its status as a highly attractive destination for DC investment. Its user base has grown sevenfold since 2005, compared to the growth of 1.9x in the Americas and 1.8x in Europe over the same period. Going forward, APAC markets should continue to lead, underpinned by further increases in internet adoption given the lower penetration rates in the region.

Currently, APAC’s network infrastructure remains structurally undersupplied, particularly in more populous sub-regional hubs. APAC’s market share of approximately 28% of worldwide bandwidth usage is therefore projected to more than double between 2023 and 2026, meaning DCs that are focused on improving interconnection nodes across the region will be able to offer clients a competitive advantage when establishing digital core, integrating digital ecosystems, and deploying digital edge strategies.6

Tighter data protection fuels additional growth

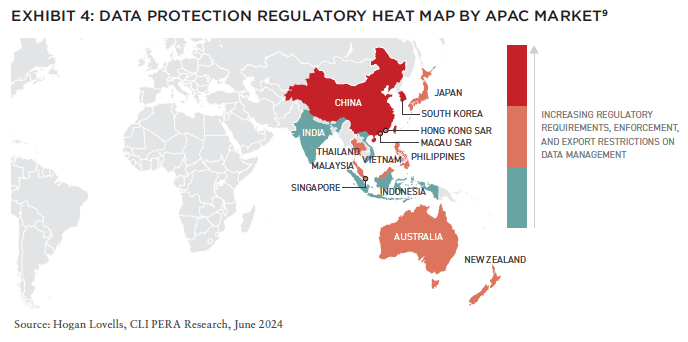

New data protection policies and cybersecurity laws introduced recently across individual APAC markets are another catalyst for DC demand because, in contrast to the more uniform regulatory environments in the US and Europe, they encourage regional governments and corporations to view data as a strategic asset.7 The resulting shift towards data localization, onshoring, and reshoring is therefore poised to boost demand for secure, onshore data storage systems.

The approach taken in Japan, Singapore, and Malaysia demonstrates that balancing data protection with pragmatic regulation can foster regionalization. By catering to specific jurisdictional requirements, while also aligning with global standards, these markets have managed to capture significant regional DC demand by offering a decentralized, yet cohesive data infrastructure network across the APAC region. Regulatory predictability and alignment with international norms have made these locations appealing for long-term investments and also provide clear pathways for market entry and exit.

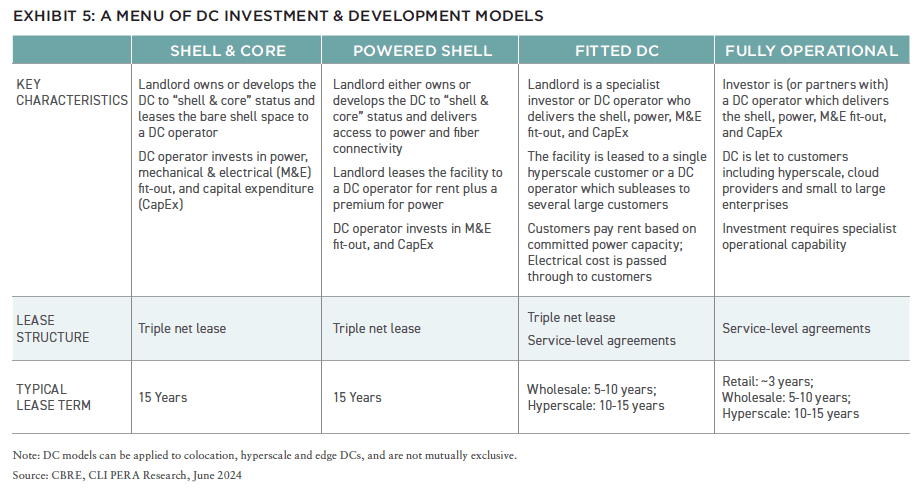

3. DCs EMERGE AS A NEW APAC INSTITUTIONAL ASSET CLASS

A platter of investment options

Given its unique and rapidly evolving nature, the DC industry offers a spectrum of options for both operators and investors, allowing it to cater to varying preferences and risk appetites.

This is one reason for the notable uptick of interest in the DC sector among institutional investors, as they look to:

- Pivot towards alternative asset classes that are more resilient to macroeconomic headwinds

- Align with strong secular, new economy tailwind

- Add assets that offer inflation protection and are complementary to existing portfolio exposure

- Go green with eco-friendly DCs that align with their ESG values and regulatory criteria

DCs becoming investment portfolio staples

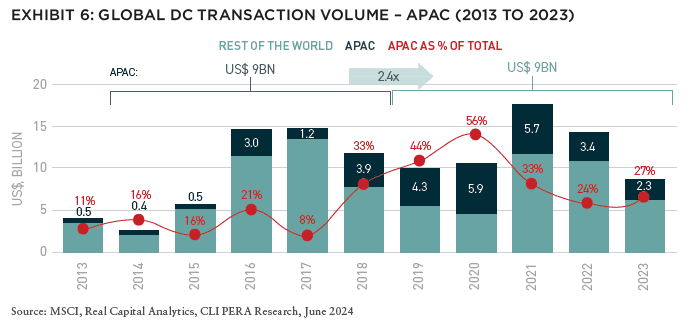

The shift in institutional investor interest towards DCs is especially evident in APAC markets. From 2019 to 2023, transactions involving APAC DCs rose to approximately US$22 billion—or almost 2.4 times the level recorded over the preceding five years—even as markets in general stagnated during the COVID-19 pandemic.

Surging volumes are the result of rising interest among institutional investors drawn to the sector’s resilience, long-term growth prospects, and more recently an extensive array of exit opportunities, including to DC operators, private equity funds, publicly traded real estate investment trusts (REITs), infrastructure investment trusts (InvITs), and sovereign wealth funds, among others.

However, despite this heightened interest, the notable lack of stabilized DCs available for sale in the region means the most promising opportunities for investors lie in developing new DC—a strategy that can both satisfy new demand and potentially yield higher returns.

NEW: SUMMIT #16

NOTE FROM THE EDITOR: ISSUE #16

Benjamin van Loon, CAE | AFIRE

GLOBAL CONSUMPTION: APAC DATA CENTER INVESTMENT STRATEGIES IN THE AGE OF DIGITIZATION

Michelle Lee, Eugene Seo, and Wayne Teo | CapitaLand Investment

DISTINCT VERTICALS: AI IS CHANGING THE REAL ESTATE INDUSTRY ON TWO DISTINCT PATHS

Daniel Carr and Andrew Peng | Alpaca Real Estate

DIVERGING FORTUNES: ARE COMPARISONS BETWEEN OFFICE AND RETAIL STILL WARRANTED?

Brian Biggs, CFA and Ashton Sein | Grosvenor

OCCUPYING FORCE: INSTITUTIONAL OFFICE PROPERTIES FEELING THE PAIN

Nolan Eyre, Scot Bommarito, and William Maher | RCLCO Fund Advisors

VALUE-ADD VS. CORE: COMPARING CORE AND NON-CORE STRATEGIES WITH NEW DATA

Yizhuo (Wilson) Ding | Related Midwest and Jacques Gordon, PhD | MIT Center for Real Estate

FAVORABLE CONDITIONS: STRUCTURAL CHANGES TO THE MARKET FAVOR NONBANK CRE LENDERS

Mark Fitzgerald, CFA, CAIA, and Jeff Fastov | Affinius Capital

INFRASTRUCTURE VIEWPOINT: INTEREST RATE CHANGES COULD UNLOCK NEW INFRASTRUCTURE INVESTMENTS

Tania Tsoneva | CBRE Investment Management

MISSING MIDDLE: WORKFORCE AND AFFORDABLE HOUSING IN THE US

Jack Robinson, PhD and Morgan Zollinger | Bridge Investment Group

NARROW SPACES: CHOKED STRAITS AND IMPLICATIONS FOR GDP, INFLATION, AND CRE

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

OPCO-PROPCO OPPORTUNITY: EMERGING MODELS AND THE KEYS TO STRUCTURING PARTNERSHIPS

Paul Stanton | PTB and Donal Warde | TF Cornerstone

TRANSFORMING LUXURY: UNLOCKING VALUE IN LUXURY HOSPITALITY REAL ESTATE

Alia Peragallo | Beach Enclave and AFIRE Mentorship Fellow, 2024

SOLAR VALUATION: IS SOLAR ENERGY A VALUATION GAME-CHANGER?

David Wei and Michael Conway | SolarKal

GROUND LEVEL: THE CASE FOR GROUND LEASES AND LONG-TERM CAPITAL

Shaun Libou | Raymond James

LEGAL UPDATE / DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman, Gregory Fennell, and Jon E. Linder | Dentons

LEGAL UPDATE / ENHANCED PROTECTION: LEVERAGING THE SAFETY ACT FOR ENHANCED LIABILITY PROTECTION IN REAL ESTATE

Andrew J. Weiner, Brian E. Finch, Aimee P. Ghosh, Samantha Sharma, and Sarah Hartman | Pillsbury

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

4. CHARTING THE COURSE THROUGH FUNDAMENTALS AND PROSPECTS

Demand-supply dynamics remain robust

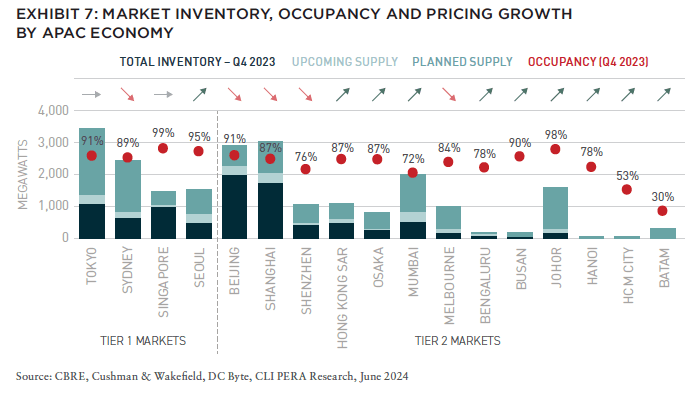

Although the APAC region already boasts an outsized internet user base as well as the world’s largest colocation market, its DC industry remains less mature compared to other parts of the world. This suggests robust growth potential, even before considering rising user demand.

Several APAC markets are set to double their DC inventory by 2025, primarily driven by Tier 1 cities such as Tokyo, Seoul and Sydney. These cities, once dominated by domestic telecom companies and conglomerates, are now seeing an influx of international DC operators in partnership with capital providers and / or strategic investors.

In addition, expansion into selective secondary markets is also underway. Johor, Malaysia, for example, is benefitting from spillover demand in the region caused by constrained capacity due to government regulations in its neighboring market, Singapore.

Major developed markets poised for future growth

A proprietary multi-criteria decision analysis8 of seventeen key markets in the APAC region identified Singapore, Tokyo; Osaka, Seoul; and Sydney as the most promising destinations. Common characteristics include robust macroeconomic and business environments, a high degree of digital literacy, availability of world-class infrastructure, and healthy demand-supply conditions for new DC capacity.

Otherwise, Hanoi and Ho Chi Minh City (Vietnam), along with Batam (Indonesia), rank lower, primarily because their status as emerging markets acts as a drag on short-term upside.

In India, while Mumbai and Bengaluru are also classified as emerging markets, they decisively outperform their regional peers in the above analysis for several reasons. For one, their economies have potential for enormous growth from a low base (in part due to growing capital migration from China); in addition, they are seeing rapid adoption of digital technologies by domestic businesses and consumers.

5. STRATEGIC IMPERATIVES AND CONSIDERATIONS

Critical elements in DC location and site selection

As in other markets worldwide, access to power and land have long been important issues for DC investors. Recently, however, power availability has taken center stage as a crucial determinant for DC locations, closely followed by a growing emphasis on sustainability.

Greening strategies for DCs

In particular, the rapid expansion of the regional DC industry, together with the energy-intensive nature of AI workloads, has added further fuel to long-standing concerns over the environmental impact of DC infrastructure,9 bringing DC users and operators under increasing pressure to reduce their carbon footprints.10

As a result, DC users are adopting new server designs and energy-efficient hardware that ensure more effective and energy-efficient use of computing resources. In addition, operators are increasingly using advanced cooling and airflow management systems that can optimize temperature regulation and curtail energy waste, as well as renewable energy sources such as solar or wind power that reduce reliance on fossil fuels. By embracing green solutions, DC operators are able not only to mitigate their impact on the environment, but also cut operational and maintenance costs.11

Risks remain

Although capacity shortages and rapidly rising demand have created favourable investment conditions, the APAC DC sector is not without risks. These include:

Cyclical demand: Global economic shifts or geopolitical factors represent significant threats to DC asset performance, both individually and collectively. Economic downturns, for example, can lead to reduced business IT spending, which in turn can impact take-up and occupancy rates.

Regulatory compliance: Data privacy and security regulations vary widely from market to market and are subject to rapid change, with potentially serious consequences for DC infrastructure demand. Additionally, compliance with local rules is essential to secure permits and regulatory approvals and to meet environmental and safety criteria. As a result, any change in local regulatory standards during the development or operational phases may necessitate costly modifications.

Obsolescence: Infrastructure must be future-proof and AI-ready. The rapid evolution of technology, regulations, and demand for new infrastructure typologies means that obsolescence risk is real. New DC infrastructure should therefore be constructed to the extent possible to allow for potential upgrades that will enable future operational efficiency, security, and cost-effectiveness.

Scope of occupier base: The dominance of major cloud operators sets a limit on the available pool of large customers, especially if they opt in future to build and manage their own DC infrastructure. The market share and capacity requirements of cloud operators also give them significant pricing power that can affect negotiations with landlords and DC providers across the industry.

Specialized capability: Various risks associated with the complexities and scale of DC operations, such as difficulty securing serviced sites, access to power supplies, and a range of operational, financial and regulatory concerns, underline the importance of partnering with DC developers that have a strong network and expertise in these sub-domains.

APAC IS WHERE CONNECTIVITY MEETS OPPORTUNITY

As demand for digital services continues to accelerate in the APAC region, the importance of the DC sector will only rise further. Each key market within the region has unique characteristics, offering investors a wealth of opportunities to tap into this fast-growing new economy sector. Given that DCs are a specialized asset class, it is crucial for investors to collaborate with dedicated partners who possess deep product knowledge and an intimate understanding of the markets in which they operate.

—

NOTES

1. The fifth industrial revolution, also known as “Industry 5.0,” is an emerging phase of industrialization with emphasis on key elements including automation, robotics, machine learning, Internet of Things (IoT), additive manufacturing, and quantum computing.

2. “Finding Opportunity in Volatility Within Asia Pacific,” n.d. https://www.capitaland.com/en/about-capitaland/newsroom/Perspectives/2023/Finding_Opportunity_in_Volatility_within_Asia_Pacific.html.

3. World Economic Forum. “The Future of Jobs Report 2023,” March 28, 2024. https://www.weforum.org/publications/the-future-of-jobs-report-2023/. More than 75% of 803 global companies surveyed will integrate big data, cloud computing, digitalization, and AI technologies by 2027.

4. Bloomberg. “AI’s Business Impact To Extend Far Beyond Nvidia,” August 2023. Accessed August 27, 2024. https://www.bloomberg.com/professional/insights/data/ais-business-impact-to-extend-far-beyond-nvidia/. Projections indicate a 42% CAGR increase from $40 billion in 2022 to $1.3 trillion by 2032.

5. Equinix. “Equinix 2023 Global Tech Trends Survey,” 2023. Accessed August 27, 2024. https://www.equinix.com/resources/infopapers/equinix-tech-trends-survey. In a recent poll, 80% of APAC companies surveyed indicated plans to expand into new regions, countries, and cities in the next 12 months. Of these, 46% plan to build dedicated DCs, while 36% intended to take space in colocation DCs.

6. Equinix. “The Global Interconnection Index (GXI) 2024,” 2024. Accessed August 27, 2024. https://www.equinix.com/gxi-report. APAC interconnection bandwidth is forecast to reach 9,283 terabits per second by 2026 and reflects a CAGR of 34% between 2023 and 2026.

7. Recent regulations include Singapore’s Personal Data Protection Act (PDPA); China’s Data Security Law (DSL) and Personal Information Protection Law (PIPL); which took effect in 2021, and Indonesia’s 2022 Personal Data Protection law (PDP law).

8. Six criteria applied in the assessment included broad economic factors, inherent business frameworks and risks, state of existing and planned infrastructure, technological readiness, susceptibility to natural calamities, and prevailing conditions in the DC market. The derived rankings are calculated using a proprietary framework that includes the six broad parameters set out above. Each comprises multiple sub-parameters that are assigned a weighting and scored on a predefined scale.

9. Boston Consulting Group. “Energy Industry Consulting & Strategy.” Accessed August 27, 2024. https://www.bcg.com/industries/energy/overview. DCs consume around 1% to 3% of global electricity usage. For example, DC electricity consumption was 2.5% of the US total (~130 TWh) in 2022 and is expected to triple to 7.5% (~390 TWh) by 2030.

10. Among global leading DC operators, Digital Realty, Equinix, Schneider Electric, Google Cloud, EdgeConneX and CapitaLand Investment have operations in APAC that embed green solutions as part of their ecosystems.

11. CapitaLand Investment operates five colocation DCs across Europe that procure 100% of its electricity from renewable sources.

—

ABOUT THE AUTHORS

Michelle Lee is the Managing Director, Private Funds (Data Center), for CapitaLand Investment. Eugene Seo is the Managing Director, Data Center, for CapitaLand Investment. Wayne Teo is a Senior Executive, Private Equity Real Assets, for CapitaLand Investment.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Leverage the only investment management suite that automates complex processes and ensures transparency from investor to asset operations, integrating investment and debt management, capital raising, investment, financial, and operational metrics through a branded investor portal. Learn more.