The growth outlook for listed infrastructure continued to improve in 2024, and companies have been key beneficiaries of a virtuous cycle of generative AI development.

We have seen increased profitability for data centers, rising estimates of future capacity installations, surging forecasts for power demand, and the utility investment needed to service this demand.

With these trends in mind, this article provides a brief overview of:

- The discounted valuations for listed infrastructure and the prospects for total return

- The extraordinary rise in utility earnings expectations following increased investment demand

- The need for infrastructure as an “all of the above” solution to service generative AI

ACCELERATING UTILITY EARNINGS EXPECTATIONS

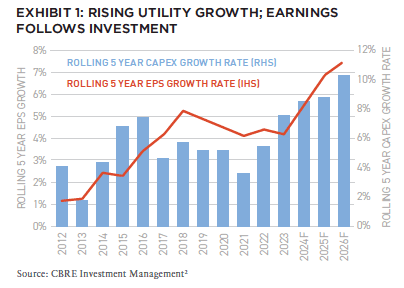

Current regulated utility earnings growth estimates are without precedent. Historically, regulated utilities in the US were moderate growers. With the retirement of coal plants, the replacement with natural gas, and the penetration of renewables, investment levels increased and growth improved (Exhibit 1).

Today’s generative AI needs represent a game change for the utility sector. As of September 2024, estimates for data center power demand called for a quadrupling of 2023 levels by 2030, representing more than 600 terawatt hours and 11%-12% of total US power demand.[1]

With associated levels for utility power demand growth rising, we expect a doubling in US utility investment by 2026 compared to 2015 levels. With higher investment, we expect utility earnings to accelerate. Notably, our forecasts do not consider a dramatic increase in the profitability or regulated returns (based on costs of capital) allowed for utilities.

These should have an additional upward bias in a future period where long-term interest rates average higher than in the previous decade; we have already seen an upward bias for utility authorized returns on equity (ROEs) in 2024 compared to 2023 and 2022 levels.

We see average long-term utility growth estimates as having the potential to reach a high single digit rate in the next two years. This is a dramatic change from a decade ago. We also see the potential for both upward revisions and an increased duration to these growth expectations.

At the utility level, planning for data center power capacity is extending into the latter half of this decade and beyond. Today, we see evidence of utilities rationing current power distribution to data centers pending the start-up of new transmission. Others have noted flagship assets as constrained by 2028, reduced transmission capacity through 2030, or are seeking “take-or-pay” contracts to support new transmission infrastructure. In the current environment, we clearly see a likelihood for enhanced utility investment over an extended period.

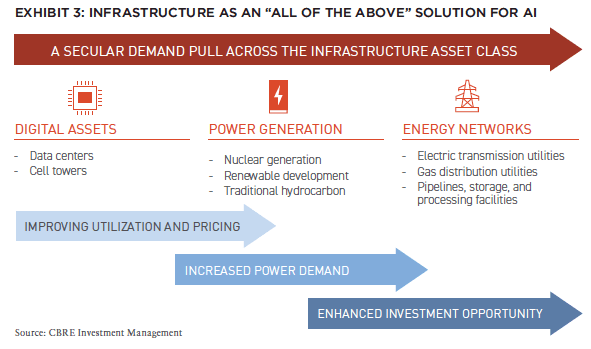

INFRASTRUCTURE AS AN “ALL OF THE ABOVE” SOLUTION

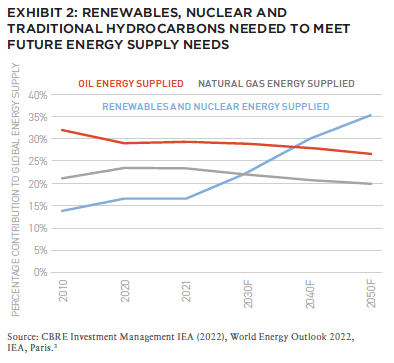

We see diverse forms of energy, and diverse sectors across infrastructure, as needed to service generative AI. In the last several months, announcements have been made regarding the restart of nuclear generation for the first time in US history; for example, Microsoft and Constellation Energy announced in September a partnership to restart the Three Mile Island nuclear facility, while Holtec Energy is working to restart the Palisades plant in Michigan. The Three Mile deal includes a long-term power purchase agreement from Microsoft.

Even before the rise of generative AI, we expected nuclear energy, renewable generation and traditional hydrocarbons capacity to assist in meeting future global demands. The need for a comprehensive energy supply is only enhanced in a post AI world.

We believe the beneficiaries of generative AI are well placed across the infrastructure asset class. Communications infrastructure companies are seeing stronger growth alongside the benefits of moderately lower borrowing rates. Contracted energy generation and renewable development are prospering in a new upcycle, while the need for energy transmission and transport remains strong.

When rolled up to the asset class level, we see infrastructure’s earnings are trending at approximately 300 basis points above their historic average, driven by infrastructure as an “all of the above” solution for generative AI.

COMPELLING VALUATIONS AND POTENTIAL TOTAL RETURNS

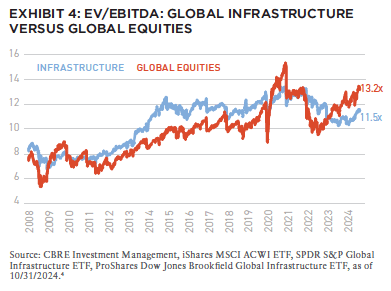

The above-average earnings growth of listed infrastructure is a key consideration in its ability to generate above-average returns in the years ahead. The starting point for investors—that of current discounted valuations—is also key.

As of Q3 2024, the earnings multiple of listed infrastructure still trades at a large discount to broad equities. The asset class offers high-income, discounted valuations to private markets and is one of the larger historical beneficiaries of cuts in global central bank borrowing rates. With the contributions of strong income yields, above-average earnings growth, and discounted valuations, we are optimistic that the asset class will eclipse the historical 8%-10% total returns it has generated over the course of the last decade.

NEW: SUMMIT #17

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

WHERE ARE WE IN THE CYCLE?: OVERVIEW OF THE US ECONOMY AND REAL ESTATE SECTOR

Richard Barkham + Jacob Cottrell | CBRE

COMPELLING OPPORTUNITIES: MAKING A CASE FOR US REAL ESTATE

Karen Martinus + Mark Fitzgerald + Max von Below | Affinius Capital

OPEN WINDOW: WHY NOW IS THE TIME TO INVEST IN COMMERCIAL REAL ESTATE

Chad Tredway + Josh Myerberg + Luigi Cerreta | JPMAM

NORMALIZING MOVEMENT: POPULATION MOVEMENTS NORMALIZING AFTER COVID-19 SHOCK

Martha Peyton + Matthew Soffair | LGIM America

CHRONIC SHORTAGE: THE US HOUSING SCARCITY WILL BE LIKELY TO PERSIST FOR SEVERAL YEARS

Gleb Nechayev | Berkshire Residential Investments

FLORIDA FOCUS: PRODUCTION INDEX BELOW 50 CURIOUSLY SIGNALS OPPORTUNITY

Rafael Aregger | Empira Group

WHOLESALE CHANGE: DEMOGRAPHIC CHANGES AND STAGNANT INVENTORY CREATE NEW OPPORTUNITIES FOR RETAIL

Stewart Rubin + Dakota Firenze | New York Life Real Estate Investors

GAME CHANGE: INFRASTRUCTURE GROWTH ACCELERATING WITH AI

Jon Treitel | CBRE Investment Management

FOR THE TREES: MASS TIMBER INTEGRATION IN INDUSTRIAL REAL ESTATE

Mary Ellen Aronow + Erin Patterson + Caroline Suarez + Cassidy Toth | Manulife Investment Management

BORDER INDUSTRIAL: INVESTING IN US/MEXICO BORDER PORT INDUSTRIAL MARKETS

Dags Chen, CFA + Lincoln Janes, CFA | Barings Real Estate

RESILIENCE AMIDST UNCERTAINTY: HOW ISRAELI AND UKRAINIAN INVESTORS ARE ADAPTING REAL ESTATE STRATEGIES DURING CONFLICT

Asaf Rosenheim | Profimex

CYBER RISK VIGILANCE: HOW REAL ESTATE DIRECTORS AND BOARDS CAN GUARD AGAINST CYBER RISK

Marie-Noëlle Brisson, FRICS, MAI + Michael Savoie, PhD | CyberReady, LLC

ALTERNATE REALTY: DIGITAL RIGHTS MANAGEMENT FOR REAL ESTATE AND AUGMENTED REALITY

Neil Mandt | Digital Rights Management + Steve Weikal | MIT Center for Real Estate

DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman + Gregory Fennell + Jon E. Linder | Dentons

HOUSING COMPLEX: CUTTING-EDGE APARTMENTS ARE A CATALYST FOR A MORE PROFITABLE FUTURE

Alejandro Dabdoub | AOG Living

NOTES

1. McKinsey and Company, “How data centers and the energy sector can sate AI’s hunger for power,” September 2024; one terawatt hour is enough to provide fully power 70,000 homes for a year, including heating and cooling.

2. Capex forecasts 2024-2025 per Edison Electric Institute; 2026 per CBRE Investment Management based on public company disclosures and informed by rate base growth expectations. Earnings forecasts per CBRE Investment Management as of September 2024. Earnings forecasts are based upon company-level forecasts, which are based upon company disclosures and CBRE IM analyst estimates for capital expenditures, equity ratios, regulated returns on equity, and other variables which can affect the earnings power of public utilities. Forecasts and any factors discussed are not a guarantee of future results.

3. Information is the opinion of CBRE Investment Management, which is subject to change and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Forecasts and any factors discussed are not a guarantee of future results.

4. Information is the opinion of CBRE Investment Management, which is subject to change and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Forecasts and any factors discussed are not a guarantee of future results.

5. Information is the opinion of CBRE Investment Management, which is subject to change and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Forecasts and any factors discussed are not a guarantee of future results.

ABOUT THE AUTHOR

Jon Treitel is the Portfolio Strategist for Listed Real Assets and a Senior Director at CBRE Investment Management. He leads listed consultant relations and supports CBRE IM client solutions and distribution partners while overseeing listed real asset thought leadership and related solutions analyses.

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

/ EXECUTIVE SPONSOR

AOG Living is a leading fully integrated, multifamily real estate investment, construction, and property management firm headquartered in Houston, Texas. AOG Living has acquired, built, or developed more than 20,000 multifamily units with a total aggregate value of over $2.4 billion and has a growing portfolio of more than 35,000 apartment homes and 170+ properties under management throughout the nation. Learn more at aogliving.com.

/ ASSOCIATE SPONSOR

Vertically integrated owner, operator, and developer of Sunbelt multifamily. Partnering with institutions on a single-asset and programmatic basis. 28k+ units acquired and developed. 62k+ units under management. 1,500+ associates. 8 Sunbelt states. To learn more, visit hrpinvestments.com and hrpliving.com. And for more information, contact john.duckett@hrpliving.com.

/ SUPPORTING SPONSOR

Affinius Capital is an integrated institutional real estate investment firm focused on value-creation and income generation. With a 40-year track record and $64 billion in gross assets under management, Affinius has a diversified portfolio across North America and Europe providing both equity and credit to its trusted partners and on behalf of its institutional clients globally. To learn more, visit affiniuscapital.com.