Sentiment around multifamily production is mixed, with significant obstacles for new development. The National Association of Home Builders’ (NAHB) Multifamily Production Index, a scale from zero to one hundred measuring builder and developer sentiment around current apartment and condo development conditions, reported a reading of forty in Q3 2024. This score, the lowest in 2024, indicates that present conditions are chiefly viewed more negative than good.

But instead of serving as a red flag for developers, a low rating can also be seen as an opportunity—particularly in markets like South Florida.

Upon emerging from the depths of the COVID-19 pandemic, a widespread narrative centered on residential oversupply has risen to the top of industry conversations. Yet, the real situation is more nuanced.

It is true that a large number of new units are being delivered throughout 2024 and 2025; however, due to the current capital markets-related headwinds, new development has essentially come to a halt. New deliveries significantly drop off in 2026, 2027, and the years thereafter. On aggregate, the region is still tremendously undersupplied when it comes to housing and the slowdown in construction activity and aging of existing inventory will only exacerbate this supply shortage in the medium- and long-term.

The combination of diminishing new supply, aging/subpar existing inventory, plus growing regional demand for housing driven by favorable economic and demographic trends, offers a solid long-term foundation for developers to capitalize on.

OVERSUPPLY: AN OVERESTIMATED PHENOMENON

Concerns around temporary oversupply are valid, and effects are being felt by developers who are currently delivering new units, competing on lease-up with several other projects delivering at the same time.

When looking ahead to 2026 and 2027 once new deliveries have largely diminished, absorption projections signal that South Florida’s multifamily pipeline will struggle to keep up with demand as there continues to be a broader regional housing shortage on an aggregate level. This shortage will only widen as developers and investors continue to pump the brakes and newer units continue to be absorbed.

In terms of occupancy, the South Florida market continues to report resilient occupancy rates, despite absorption concerns: 95% in Q2 2024, outpacing the national average by 80 basis points.[1] With regard to absorption, by the end of Q2 2024, there were 6,910 net units absorbed in South Florida, equating to 89% of the total net absorption in 2023 and more than the entire net absorption in 2022.[2]

A recent report by Berkadia contradicts the oversupply worries with occupancy projections showcasing that multifamily occupancy has already troughed in 2023 and is expected to remain within the 96% range in 2026. Furthermore, the occupancy spread between South Florida and the national level is solely expected to widen in favor of the former.

Brickell, an area of Miami, which has become the leading financial hub of the South and a draw for large corporations, experienced growing residential rents, resilient office occupancies, and is a prime example that the oversupply phenomenon is overstated. As of Q3 2024, there were no market-rate-only multifamily projects under construction, with only three in the permitting phase, despite the strong local market fundamentals.[3] The newest entirely market-rate multifamily property in Brickell was delivered in 2019 under the name “Maizon.”

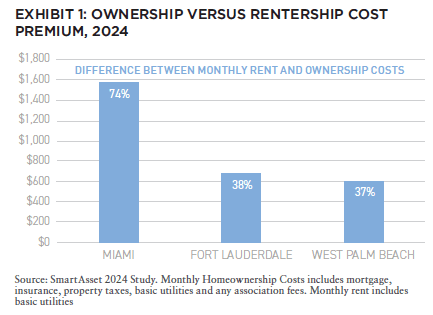

Brickell has seen numerous branded luxury condominiums deliver since 2019, though South Florida’s condominium shadow rental market is a common misconception. It would be inaccurate to assume that this condominium shadow rental market will capture or subsidize the multifamily housing shortage in a meaningful way. Owning a residential property today is much more costly than renting, which is an equation unlikely to change any time soon, with the average monthly mortgage payment significantly outpacing monthly rent payments nationwide.[4]

In South Florida, monthly cost premiums for total ownership compared to costs for renter households are up as much as 74% in metros, including Miami.[5] In addition to mortgage payments, condominium owners are also on the hook for escalating HOA fees, insurance, and property taxes, thereby limiting ability to recoup costs of ownership from a tenant. As a result, Miami’s condominium shadow rental market comes at much higher rents (approximately 20%-30% higher) than the top end of the Class-A multifamily market, which means that a condominium rental unit and a multifamily unit are not in fact competing for the same type of tenant.

NOT ALL STOCK IS EQUAL

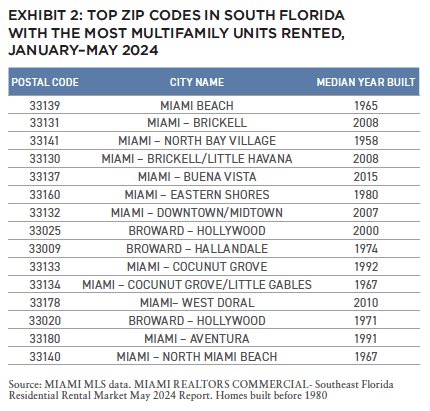

Another consideration limiting aggregate residential supply is the fact that a significant portion of South Florida’s housing inventory is aging. In Miami-Dade, Broward, and Palm Beach counties, 74% of condos were built before 1993.[6] The aging supply forces renters to rent older units. For example, 377 multifamily units were rented that were built before 1980 in the affluent zip code of Brickell from January through May 2024, due to the undersupply of newer buildings.

Further analyzing South Florida zip codes with the most pre-1980 multifamily units rented during this time period, more than two-thirds of those zip codes had an inventory with a median built year prior to 2000.[7] Older buildings have become costly to maintain, lack safety measures to mitigate the effects of severe weather hazards, and overall present as a much less attractive housing option for the evolving renter profile in the region.

New building codes implemented following the Champlain South Tower collapse in 2021 have increased operational costs and potential financial risks (e.g., assessments) for older buildings, making them less appealing for both residential and investment purposes. These new building codes require mandatory structural integrity inspections for condominium buildings that are three stories or taller, particularly those reaching thirty years old, with harsh timelines for buildings located near the coastline.

Meanwhile, affluent young professionals and empty nesters increasingly seek new, amenity-rich rental properties in premium locations. New York transplants focus on walkability and amenity scores, willing to pay a premium for such conveniences. Traffic has also become an infrastructural hurdle for South Florida, further increasing the value for properties accessible to public transportation and with proximity to jobs, restaurants, and leisure activities.

The price margin between Class A, B, and C rents have widened. From the end of 2020 to the first quarter of 2024, average Class A rent premiums increased by approximately 23% compared to Class B from 2015-2019, and average Class A rents saw an increase of 35% in premiums compared to Class C from 2015-2019.[8] Furthermore, over the last decade, 90% of demand growth has been concentrated in four- and five-star units in Miami.

ECONOMIC AND DEMOGRAPHIC RESILIENCE IN SOUTH FLORIDA

In terms of multifamily rental demand, South Florida has solidified its position as a hotspot for resilient economic and demographic growth, particularly Miami and West Palm Beach, which have benefited from an influx of high-paying jobs and skilled professionals.

Florida’s GDP is expected to grow by 4.1% in 2025, with a 3.9% increase anticipated in 2026.[9] The strong correlation between multifamily rent growth, GDP growth and a healthy local labor market, illustrates a solid demand backdrop for multifamily investments in South Florida in the years ahead.

The region’s economy is also diversifying beyond its traditional reliance on leisure and hospitality, in turn cultivating resilience. Sectors such as information technology, professional services, and manufacturing are expanding, further decreasing industry-specific dependence and risk. Southeast Florida is projected to boast 2.4% job growth in 2025. As of Q2 2024, there were 1.6 job openings for every unemployed Floridian.[10] This exemplifies a robust job market and confirms a dynamic business landscape for employers, both of which will continue to propel in-migration.

Revisiting Miami and Brickell as a prime example, in August 2024, Miami recorded a 2.9% increase in private-sector jobs—double the national average—adding 33,300 positions.[11] Brickell appeals to affluent residents, with its primary ZIP code (33131) boasting a mean household income of $185,585 (median of $121,730).[12]

Further highlighting the strength of the job market and the robust demand for commercial spaces, recent Q2 2024 data indicates that Miami’s Class A office vacancy rates have decreased 1.1% year-over-year. Brickell displayed an impressive average asking lease rate of $99.40 per square foot—a 5.8% year-over-year increase in price.[13]

Companies are investing in the region and growing their skilled workforces. In addition to Ken Griffin’s large investment in South Florida, J.P. Morgan is also increasing its capacity by adding four hundred more employees, doubling the size of its Brickell office to 160,000 square feet. Paul Singer’s firm, Elliott, just closed on the office tower 701 Brickell, a Class A trophy asset, for $443 million, which represents the second largest office transaction in the history of Florida. Similarly, in West Palm Beach, Goldman Sachs, Point72, and J.P. Morgan are among an impressive list of tenants of the newly developed office tower, 360 Rosemary.

South Florida’s Class A office market is healthy, which differentiates it from most office markets across the US and is representative for the region’s strong local economy and intact growth prospect.

THE IMPORTANCE OF MICRO-LOCATION STRATEGY

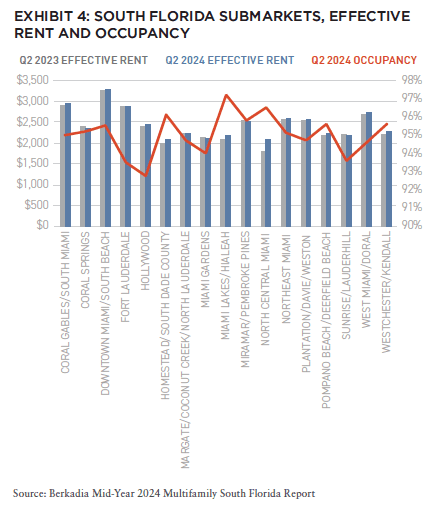

Investment success in South Florida increasingly depends on micro-location analysis. Submarkets like Coral Gables or Downtown Miami outshine others in effective rent and occupancy growth.

For instance, in Q2 2024, Downtown Miami reported an effective rent of $3,286 with a 70-basis-point increase in occupancy to 95.5%. In contrast, North Central Miami reported rents of $2,096 and a 150-basis-point decline in occupancy, which indicates lower desirability and stronger temporary supply headwinds due to lower barriers to entry for new development.[14]

Developers who target submarkets with higher barriers to entry plus superior characteristics regarding walkability, transportation, safety, and access to top schools will see higher rent growth and occupancy, thereby increasing their chance for investment success.

ACTIVE PLAYERS IN THE SOUTH FLORIDA MARKET WILL BE REWARDED

The real estate sector is approaching the next phase of growth, making this the ideal moment to prepare for future opportunities. In fact, the negative sentiment and related slowdown in new supply activity may essentially unearth the best opportunities in South Florida over the next few years.

The current environment offers unique entry points that should not be overlooked due to negative sentiment. Investors who continue to be active in markets with steady demand, growth drivers and supply limitations will be rewarded over the next real estate market cycle.

NEW: SUMMIT #17

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

WHERE ARE WE IN THE CYCLE?: OVERVIEW OF THE US ECONOMY AND REAL ESTATE SECTOR

Richard Barkham + Jacob Cottrell | CBRE

COMPELLING OPPORTUNITIES: MAKING A CASE FOR US REAL ESTATE

Karen Martinus + Mark Fitzgerald + Max von Below | Affinius Capital

OPEN WINDOW: WHY NOW IS THE TIME TO INVEST IN COMMERCIAL REAL ESTATE

Chad Tredway + Josh Myerberg + Luigi Cerreta | JPMAM

NORMALIZING MOVEMENT: POPULATION MOVEMENTS NORMALIZING AFTER COVID-19 SHOCK

Martha Peyton + Matthew Soffair | LGIM America

CHRONIC SHORTAGE: THE US HOUSING SCARCITY WILL BE LIKELY TO PERSIST FOR SEVERAL YEARS

Gleb Nechayev | Berkshire Residential Investments

FLORIDA FOCUS: PRODUCTION INDEX BELOW 50 CURIOUSLY SIGNALS OPPORTUNITY

Rafael Aregger | Empira Group

WHOLESALE CHANGE: DEMOGRAPHIC CHANGES AND STAGNANT INVENTORY CREATE NEW OPPORTUNITIES FOR RETAIL

Stewart Rubin + Dakota Firenze | New York Life Real Estate Investors

GAME CHANGE: INFRASTRUCTURE GROWTH ACCELERATING WITH AI

Jon Treitel | CBRE Investment Management

FOR THE TREES: MASS TIMBER INTEGRATION IN INDUSTRIAL REAL ESTATE

Mary Ellen Aronow + Erin Patterson + Caroline Suarez + Cassidy Toth | Manulife Investment Management

BORDER INDUSTRIAL: INVESTING IN US/MEXICO BORDER PORT INDUSTRIAL MARKETS

Dags Chen, CFA + Lincoln Janes, CFA | Barings Real Estate

RESILIENCE AMIDST UNCERTAINTY: HOW ISRAELI AND UKRAINIAN INVESTORS ARE ADAPTING REAL ESTATE STRATEGIES DURING CONFLICT

Asaf Rosenheim | Profimex

CYBER RISK VIGILANCE: HOW REAL ESTATE DIRECTORS AND BOARDS CAN GUARD AGAINST CYBER RISK

Marie-Noëlle Brisson, FRICS, MAI + Michael Savoie, PhD | CyberReady, LLC

ALTERNATE REALTY: DIGITAL RIGHTS MANAGEMENT FOR REAL ESTATE AND AUGMENTED REALITY

Neil Mandt | Digital Rights Management + Steve Weikal | MIT Center for Real Estate

DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman + Gregory Fennell + Jon E. Linder | Dentons

HOUSING COMPLEX: CUTTING-EDGE APARTMENTS ARE A CATALYST FOR A MORE PROFITABLE FUTURE

Alejandro Dabdoub | AOG Living

NOTES

1. “Multifamily Market Survey (MMS) (National Association of Home Builders).” Q3 2024. Nahb.org. 2024. https://www.nahb.org/news-and-economics/housing-economics/indices/multifamily-market-survey.

2. Berkadia. 2024. Review of South Florida Multifamily Report. July 2024 https://berkadia.com/wp-content/uploads/2024/07/Berkadia-Mid-Year-2024-Multifamily-Report-South-Florida.pdf.

3. CBRE Multifamily South Florida, CBRE, Inc, and Calum Weaver. 2024. Review of 2024 Mid-Year Market Report. August 19, 2024. https://mediaassets.cbre.com/-/media/project/cbre/shared-site/teams/united-states/ft-lauderdale/calum-weaver/2024-mid-year-market-report.pdf?rev=b02612ecb06347569ea904c3e417e6a7

4. Walker & Dunlop. Q2 2024. Review of South Florida Multifamily Pipeline Report. https://acrobat.adobe.com/id/urn:aaid:sc:EU:9d961b06-0f6e-4e02-9674-03410a7cbd1b.

5. Likos, Paulina. 2024. “The Commercial Real Estate Recovery Is On, but the Rebound May Be Uneven.” CNBC. October 18, 2024. https://www.cnbc.com/2024/10/18/commercial-real-estate-recovery-may-be-uneven.html.

6. “Rent vs. Buy: A Comparison of Housing Costs in U.S. Cities – 2024 Study.” 2024. Smartasset.com. 2024. https://smartasset.com/data-studies/rent-vs-buy-2024.

7. Gregor, Lori. “Cause and Effect of Florida’s New Condo Law.” Due Diligence, 5 March 2024, warrington.ufl.edu/due-diligence/2024/03/05/cause-and-effect-of-floridas-new-condo-law/.

8. Miami Realtors Commercial “Southeast Florida Residential Market Report” May 2024. https://www.miamirealtors.com/wp-content/uploads/bsk-pdf-manager/2024/06/Southeast-Florida-Residential-Rental-Market-Report-May-2024.pdf.

9. “Metro of the Month: South Florida.” Berkadia, July 11, 2024. https://berkadia.com/blog/metro-of-the-month-south-florida/.

10. Florida TaxWatch. 2024. “Florida Economic Forecast 2023-2028 | Q2 2024”. Floridataxwatch.org.

11. Florida TaxWatch. 2024. “Florida Economic Forecast 2023-2028 | Q2 2024”. Floridataxwatch.org.

12. “FloridaCommerce Announces the Miami Area August 2024 Employment Data.” 2024. Floridajobs.org. 2024. https://floridajobs.org/news-center/DEO-Press/2024/09/20/floridacommerce-announces-the-miami-area-august-2024-employment-data.

13. United States Census Bureau. 2022. “American Community Survey 5-Year Data (2009-2017).” Census.gov. December 6, 2022. https://www.census.gov/data/developers/data-sets/acs-5year.html.

14. “Miami Office Figures – Q2 2024.” 2024. Cbre.com. 2024. https://www.cbre.com/insights/figures/miami-office-figures-q2-2024.

15. Berkadia. 2024. Review of South Florida Multifamily Report. July 2024 https://berkadia.com/wp-content/uploads/2024/07/Berkadia-Mid-Year-2024-Multifamily-Report-South-Florida.pdf.

ABOUT THE AUTHOR

Rafael Aregger is the Head of US Investments at Empira Group, a leading real estate investment manager.

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

/ EXECUTIVE SPONSOR

AOG Living is a leading fully integrated, multifamily real estate investment, construction, and property management firm headquartered in Houston, Texas. AOG Living has acquired, built, or developed more than 20,000 multifamily units with a total aggregate value of over $2.4 billion and has a growing portfolio of more than 35,000 apartment homes and 170+ properties under management throughout the nation. Learn more at aogliving.com.

/ ASSOCIATE SPONSOR

Vertically integrated owner, operator, and developer of Sunbelt multifamily. Partnering with institutions on a single-asset and programmatic basis. 28k+ units acquired and developed. 62k+ units under management. 1,500+ associates. 8 Sunbelt states. To learn more, visit hrpinvestments.com and hrpliving.com. And for more information, contact john.duckett@hrpliving.com.

/ SUPPORTING SPONSOR

Affinius Capital is an integrated institutional real estate investment firm focused on value-creation and income generation. With a 40-year track record and $64 billion in gross assets under management, Affinius has a diversified portfolio across North America and Europe providing both equity and credit to its trusted partners and on behalf of its institutional clients globally. To learn more, visit affiniuscapital.com.