Already exponential, growth in demand for data center capacity is accelerating, fueled by surging digital data creation, cloud computing, and the widespread adoption of new technologies like artificial intelligence.

Society relies on digital applications for work, education, transportation, entertainment, healthcare, and just about every other aspect of our modern lives. Through these digital applications, we create and consume massive amounts of data (three times more in 2023 than 2019).

All that data—even data in the “cloud”—is processed and stored inside a data center. Data centers are the cornerstones of our digital world.

Already exponential, growth in demand for data center capacity is accelerating, fueled by surging digital data creation, cloud computing, and the widespread adoption of new technologies like artificial intelligence. This massive demand is outpacing data center development, which is challenged by supply chain delays, power constraints, and community pushback in some markets.

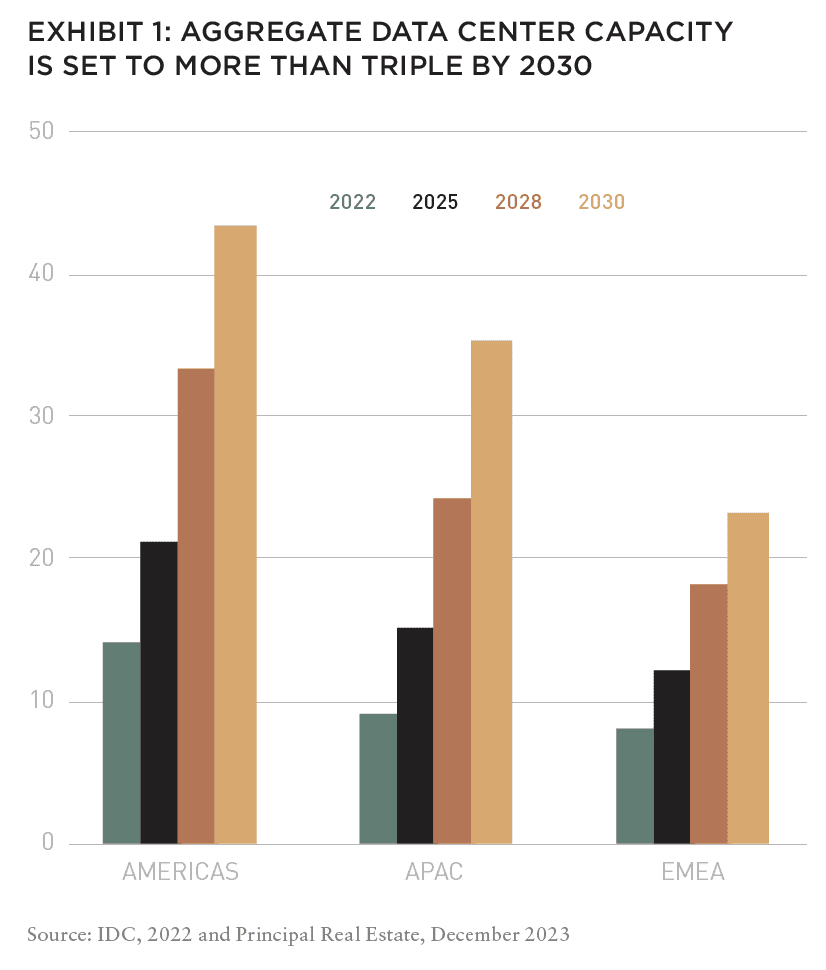

To be clear, supply is growing: aggregate data center capacity is set to more than triple by 2030. But it is not growing as fast as demand, and as a result, data center vacancy rates are at all-time historic lows and rents continue to rise. These market dynamics create a unique opportunity for investment in an alternative asset class that exhibits core characteristics, including relatively stable cash flow. Developing the data center capacity to meet demand will require a huge amount of capital, so investment opportunities abound.

Investors new to the data center sector may wonder about obsolescence: with technology changing so rapidly, will today’s data centers be able to support tomorrow’s workloads? It’s true that developers are innovating their designs, including new approaches to powering and cooling the data center in response to the demands of AI workloads, power constraints, and tenants’ increasing focus on sustainability. But even as developers introduce these new approaches, yesterday’s data centers won’t become obsolete as long as they were designed to be future-proof.

As part of a broader real estate portfolio, data centers are a diversification strategy that may help to maximize returns without increasing risk. For most investors, a fund investment is likely the most viable way to enter the data center market today, given that a single facility can cost upwards of a billion dollars (dependent, of course, on its size).

The sheer size of the market relative to other alternative investment sectors is in fact a distinct advantage. Data centers are a growing share of the net lease sector, and of some open-end diversified core equity (ODCE) funds as well. No question, data centers are a viable asset class for institutional investors.

NEW TRENDS IN THE DATA CENTER INDUSTRY

AI workloads, such as machine learning and natural language processing, are exceptionally computationally intensive. Training sophisticated AI models such as GPT-4 can require thousands of specialized processors running for weeks. As AI proliferates across industries, the need for infrastructure to support these workloads is skyrocketing.

In a single ninety-day period in 2023, end users in the US signed data center leases totaling a staggering 2.1 gigawatts, according to research by TD Cowen.1 That’s about 20% of the size of the entire third-party US data center market. Aggregate data center capacity is set to more than triple by 2030, and AI could drive demand up much more than that. (Dell CEO Michael Dell predicts that AI will drive a 100x increase in data center demand over the next ten years.2)

Cloud keeps growing, too. Demand for data centers to support AI is additive to demand for data centers to support traditional and cloud workloads, which continue to grow rapidly as enterprises migrate an ever-growing portion of their IT workloads to the cloud. Spending on cloud infrastructure is projected to reach $156.7 billion by 2027, according to IDC—over a third of total compute and storage infrastructure spend.3 In fact, hyperscale companies’ massive and growing cloud platforms are subsidizing their AI investments, as cloud businesses are typically very profitable. (For example, Amazon’s cloud business, AWS, is the company’s most profitable.4)

To meet rising demand, cloud providers are aggressively expanding their global footprints—including by launching new cloud regions and availability zones where they’ve outgrown existing regions and zones. (A cloud region has one or more availability zones within it, and an availability zone has one or more data centers.)

Manufacturing and transportation bottlenecks arising from COVID-19—exacerbated by exponentially rising demand—caused data center supply chain timelines to balloon. In general, supply chain constraints are easing as manufacturers and logistics providers work through backlogs and ramp up capacity to meet rising demand. However, lead times for some data center critical infrastructure remain significantly extended; generators, for example, are still two years out.

In both the US and Europe, power constraints have worsened as demand from the data center industry and other sectors outpaces utilities’ ability to expand capacity. In many markets, it can take years to get power utility interconnection at a data center site. In Northern Virginia, the world’s largest data center hub, developers face a multi-year backlog for new electricity connections. In Dublin, Ireland, new data center development has been stymied by power shortages.

In some markets, data center development is also slowed by local community concerns. For example, Amsterdam and Singapore have implemented restrictions on data center development due to resource constraints and local opposition. And in the US, in Virginia, lawmakers have proposed a wave of restrictions. In Georgia, the legislature suspended the state’s sales tax exemption for data centers for two years, during which time a state commission will examine the impact of data centers on the state’s power grid.

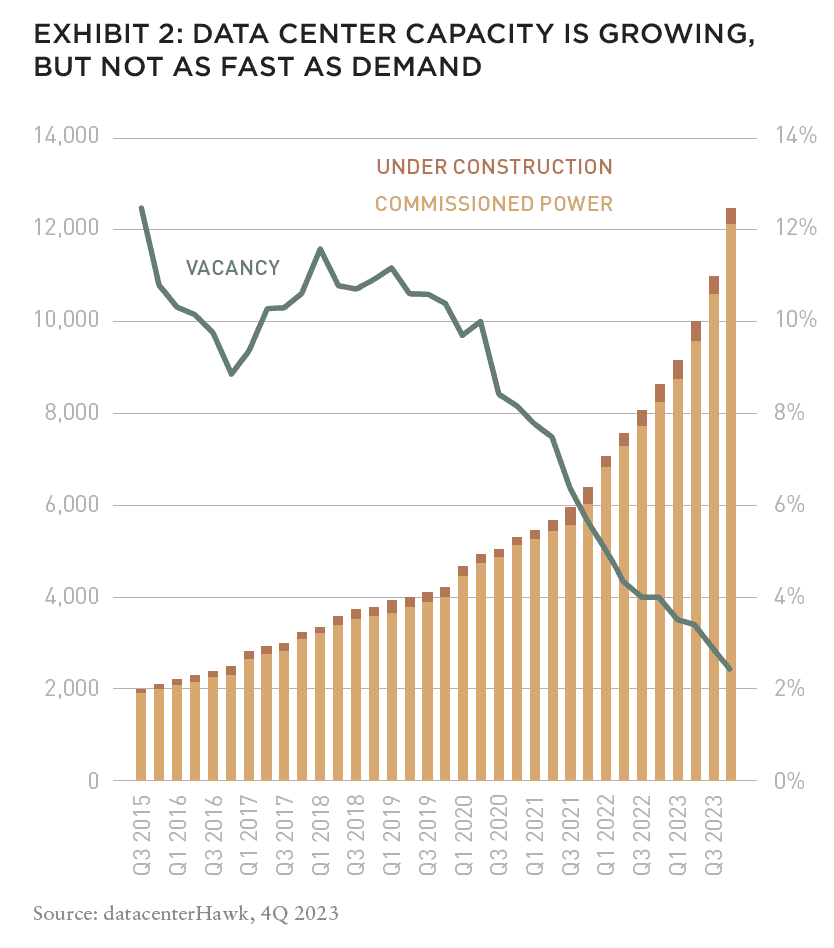

But even as supply chain delays, power constraints, and community pushback are a damper on data center development, they’re not shutting it down completely. The amount of data center capacity coming online continues to rise, rapidly—just not as fast as demand. As a result, vacancy rates are at all-time historic lows and rents continue to rise.

BOOSTING SUSTAINABILITY

Sustainability is a key corporate priority, as companies recognize the importance of reducing their environmental footprint to mitigate climate change, manage risk, meet customer expectations, and attract investors. Across industries, companies are taking steps to improve their sustainability, including by setting science-based emissions reduction targets, investing in renewable energy, and working to reduce carbon impact across their supply chains.

Much of the focus now is on identifying GHG emissions and opportunities to reduce those, which encompasses energy efficiency in both mechanical and electrical systems. Most large companies have committed to science-based emissions reductions targets—in line with limiting global warming to well-below 2°C above pre-industrial levels. Many have announced plans to achieve net-zero emissions or even be carbon negative by 2030.5

AI is pushing data center density to new heights, and rising densities demand new cooling approaches. The processors used for AI are far more power-hungry than traditional processors, and their deployments are far denser. A rack of AI servers can require ten times the amount of power as a rack of servers running typical enterprise workloads. And because more power per square foot translates to more heat, the cooling requirements for AI workloads are substantially higher than for traditional workloads. This drives the need for new cooling strategies.

Traditional forced-air cooling, which operates by circulating cool air and expelling warm air, can encounter several challenges at higher densities. The sheer volume of heat generated in a high-density rack can overwhelm the air-cooling capacity. A more effective solution for high-density racks, liquid cooling systems work by circulating a coolant directly through heat exchangers or cold plates positioned close to heat-generating components (such as the servers in the rack). This approach allows for more direct and efficient heat transfer and thereby enables higher densities.

Operators are also exploring new approaches to getting the power they need to meet demand. On-site nuclear generation via small modular reactors (SMRs) is gaining interest, though in many communities it would likely generate even more public backlash and regulatory scrutiny than developers already face. Microgrids, which combine on-site generation, storage, and intelligent control systems, are also attracting interest. By enabling data centers to operate independent of the grid when needed, microgrids can enhance uptime and reduce reliance on diesel generators. Fuel cells, which generate electricity through a clean electrochemical process, are another emerging power option. But none of these are quick solutions.

In response to tenants’ increasing focus on sustainability, data center operators are implementing a range of measures to minimize their environmental impact. These measures range from deploying energy- and water-efficient equipment to using AI-powered tools to optimize resource consumption. Renewable energy is a particular focus, with data centers increasingly powered by solar, wind, and other clean sources. In some cases, operators are building their own renewable energy plants. In addition to mitigating power constraints, on-site power generation could also improve sustainability—if generation is carbon-free. Other innovative solutions include capturing waste heat and cooling systems that don’t consume water.

EXPLORE THE NEW ISSUE

NOTE FROM THE EDITOR: WELCOME TO #15

Benjamin van Loon | AFIRE

MID-YEAR CRE MARKET OUTLOOK: AFIRE

Benjamin van Loon and Gunnar Branson | AFIRE

MULTIFAMILY OUTLOOK: AMERICAN REALTY ADVISORS

Sabrina Unger and Britteni Lupe | American Realty Advisors

MULTIFAMILY GAP CAPITAL: BARINGS REAL ESTATE

Dags Chen, CFA and Lincoln Janes, CFA | Barings Real Estate

SINGLE-FAMILY RENTAL OUTLOOK: CERBERUS CAPITAL MANAGEMENT

Kevin Harrell | Cerberus Capital Management

SINGLE-FAMILY RENTAL SUPPLEMENT: YARDI

Paul Fiorilla | Yardi

LOGISTICS OUTLOOK: BRIDGE INVESTMENT GROUP

Jay Cornforth, Jack Robinson, PhD, Morgan Zollinger, and Cole Nukaya | Bridge Investment Group

DATA CENTER OUTLOOK: PRINCIPAL ASSET MANAGEMENT

Casey Miller and Ben Wobschall | Principal Asset Management

SELF-STORAGE OUTLOOK: HEITMAN

Zubaer Mahboob | Heitman Europe

COLD-STORAGE OUTLOOK: NEWMARK

Lisa DeNight | Newmark

OFFICE OUTLOOK: CUSHMAN & WAKEFIELD

David Smith | Cushman & Wakefield

RETAIL OUTLOOK: MADISON INTERNATIONAL REALTY

Christopher Muoio | Madison International Realty

HOSPITALITY OUTLOOK: JLL

Zach Demuth | JLL

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

FUTURE-PROOF DESIGN

Investors new to the data center sector may wonder about obsolescence—with technology changing so rapidly, will today’s data centers be able to support tomorrow’s workloads? It’s a valid concern, and ensuring that yesterday’s data centers will serve tomorrow’s needs requires developers to “future proof” their designs.

Data center operators are embracing a “system of systems” approach to make their facilities adaptable—incorporating new technologies incrementally, without expensive and disruptive overhauls.

An operator might deploy a new cooling system in one data hall, for example, while leaving the rest of the facility unchanged. Standardized, interoperable components are key to this flexibility. Retrofitting a data center equipped with forced air cooling to accommodate liquid cooling at the rack level—to support high-density AI workloads, for example—is feasible. If the facility already has a chilled water loop, it can be extended directly to the racks, making for a relatively easy transition.

NEW OPPORTUNITIES FOR INVESTORS IN DATA CENTERS

The fact that massive demand for data center capacity is outpacing supply presents unique opportunities for investment in a large and growing alternative asset class that exhibits core characteristics. Even as data center developers innovate their designs, “old” facilities will remain viable for both traditional and new workloads—ensuring long-term viability of data center assets.

Beyond those underlying fundamentals, there are a range of reasons why investors are increasingly interested in the data center sector.

A diversified real estate portfolio with industrial and data center assets yields (in the example shown in Exhibit 3) a much larger return for the same level of risk as a portfolio with industrial and apartment assets.

For most investors, a fund investment is likely the most viable way to enter the data center market today, given that a single facility can cost upwards of a billion dollars.

In addition to higher-than-ever and still-rising aggregate demand, individual data centers are becoming ever larger, and thus require much more capital to develop. Those dynamics have changed the optimal investment approach. When a $500 million investment could buy a diversified portfolio of data center assets, an SMA-type approach was viable for many investors. But when a single facility costs $1 billion or more, a fund investment is the most viable way for most investors to get a diversified stake in the data center sector.

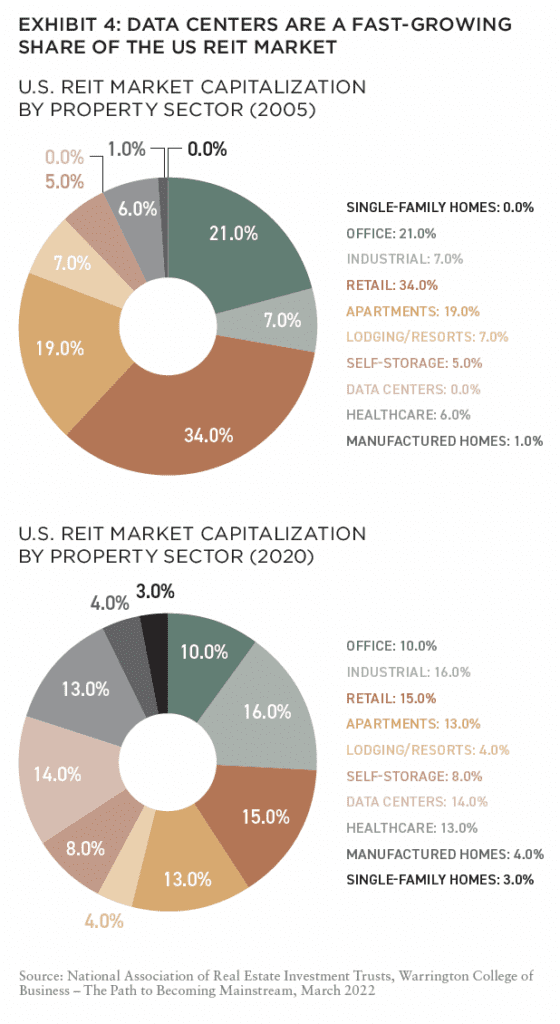

Investors report that they want to significantly increase their allocation to alternatives—and data centers in particular. Eighty-nine percent of respondents to CBRE’s 2023 Global Data Center Investor Sentiment Survey, many of whom are the world’s largest institutional real estate investors, reported plans to increase their capital deployment in the data center sector.6 One advantage of data centers relative to other alternative investments is the sheer size of the market. Other attractive alternative investment sectors—self-storage, manufactured housing, and single-family residential, for example—are quite small. Even compared to traditional sectors, data centers are a growing share. For example, the data center sector now has almost as large a share of the US REIT market as retail and industrial.

Another advantage of data centers relative to other alternative investments is the caliber of tenants. While a relatively small number of tenants consume the vast majority of data center capacity, these are the world’s largest technology companies with excellent credit profiles—Google, Amazon, Microsoft, and Meta, and a few others. Investors can reduce concentration risk with a larger fund vehicle that provides exposure to multiple assets in multiple markets, potentially with multiple developers or operating partners.

Among the advantages of the data center sector are its core investment characteristics, including long-term stable cash flows supported by high-quality tenancy, as well as secular demand drivers creating a very landlord-friendly market. Institutional investors have taken note, and data centers are a growing component in some open-end diversified core equity (ODCE) funds. Similarly, data centers are becoming a larger share of the net lease sector, which currently is primarily retail-driven, with some office.

Where investors historically would have bought a large office building leased to a corporate tenant based on the fact that it had a long-term net lease in place, that’s not a particularly attractive opportunity in today’s market. Data centers represent an opportunity for those types of investors to get similar cash flow profiles (long-term stable income) with a high-quality credit tenant while growing exposure to an alternative asset class.

BOTTOM LINE

The data center industry is experiencing explosive demand growth driven by AI and cloud computing. Although developers are innovating to overcome supply constraints and sustainability challenges, capacity is still outpaced by demand. This presents attractive opportunities for investors to diversify their portfolios with a viable alternative asset class.

—

NOTES

1. Cowen and Company, LLC. “A Tsunami of AI Demand Hits the Data Center Market.” TD Cowen. TD Cowen, July 24, 2023. Accessed May 28, 2024. https://cowen.bluematrix.com/sellside/EmailDocViewer?encrypt=78a0ca89-33f7-4a2a-9b79-9bc964666934&mime=pdf&co=cowen&id=world-cowen-morningnotesdistribution@cowen.com&source=mail.

2. Yao, Deborah. “Dell CEO: We Could Need 100X More Data Centers in 10 Years – SXSW 2024.” AIBusiness, March 14, 2024. Accessed May 28, 2024. https://aibusiness.com/verticals/dell-ceo-we-could-need-100x-more-data-centers-in-10-years-sxsw-2024.

3. IDC: The premier global market intelligence company. “Cloud Infrastructure Spending Continued to Grow in the Second Quarter of 2023 Led by Spending on Shared Cloud Infrastructure, According to IDC Tracker,” n.d. https://www.idc.com/getdoc.jsp?containerId=prUS51280423.

4. “Think Amazon Rakes In Most of Its Profit Through E-Commerce? Nope — 74% of Its Operating Income Instead Comes from This.” Nasdaq, n.d. https://www.nasdaq.com/articles/think-amazon-rakes-in-most-of-its-profit-through-e-commerce-nope-74-of-its-operating.

5. Science Based Targets. “Companies Taking Action.” Accessed May 28, 2024. https://sciencebasedtargets.org/companies-taking-action.

6. “CBRE Global Data Center 2023 Investor Sentiment Survey Results.” CBRE, June 2023. Accessed May 28, 2024. https://www.cbre.com/-/media/project/cbre/dotcom/global/services/invest/capital-markets/data-center-capital-markets/cbre-2023-data-center-investor-sentiment-survey–market-outlook.pdf

—

ABOUT THE AUTHORS

Casey Miller is Managing Director, Portfolio Management, and Ben Wobschall is Managing Director, Portfolio Management, for Principal Asset Management.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Founded in 1992, Cerberus is a global leader in alternative investing with approximately $65 billion1 in assets across complementary credit, private equity, and real estate strategies. We invest across the capital structure where our integrated investment platforms and proprietary operating capabilities create an edge to improve performance and drive long-term value. Learn more.

Principal Real Estate is the dedicated real estate investment team of Principal Asset Management, the global investment solutions business for Principal Financial Group®. As a top 10 global real estate manager, with over $98 billion in assets under management and more than 60 years of experience, we provide clients with access to opportunities across both public and private equity and debt. Learn more.