The US is the largest global commercial real estate market and remains an attractive target for investors. Past return performance, favorable growth and demographics, a strong legal infrastructure, and a diverse asset base have historically attracted foreign investors, and we expect this trend to continue.

Overseas investors continue to look to the US amid a hunt for diversification and enhanced yield. The US is one of the most transparent developed markets globally, supported by a strong and deep private service sector market and coupled with leading academic institutions that all underpin real time information for global allocators.

This article examines recent investment activity and explores our view on why now, more than ever, may represent a good opportunity for foreign investors to invest in US real estate.

FOREIGN INVESTMENT DOWN, BUT NOT OUT

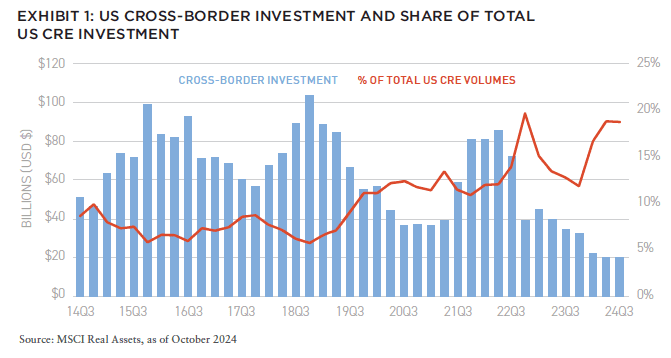

The volume of cross-border investment into the US fell sharply in 2024. Acquisitions by foreign investors totaled $20.2 billion for the year to Q3 2024, down 41% from the pace set in 2023 and 59% behind the 15-year average (Exhibit 1).

The decline in cross-border activity was much sharper compared to total US CRE investment volumes which declined 14% year-over-year in the twelve months to Q3 2024.[1] While cross-border investment volume has remained limited, there are some positive signals in the latest trends, and resultant opportunities ahead.

The US remains one of the most active destinations for foreign capital in the world. Recently, the US CRE investment market is showing tentative signs of recovery from the slowdown sparked by elevated inflation and higher interest rates. The Federal Reserve has recently cut rates by 75 basis points, ODCE/NPI returns were positive in Q3 2024 for the first time since Q3 2022, and valuations (outside of office) appear to have bottomed. REIT sectors certainly have seen a rebound in 2024 as well.[2]

US FACES BETTER ECONOMIC PROSPECTS

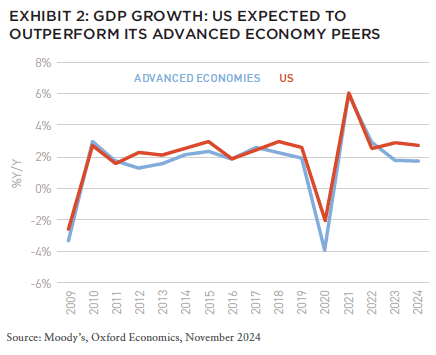

Since 2009, US GDP growth has largely outperformed other advanced economies. The outperformance over the past two years has been especially stark—a trend that is expected to continue into 2025 (Exhibit 2).[3] Continued healthy employment growth and moderating inflation are expected to have a positive effect on US economic activity over the next few years, and accordingly, growth forecasts have been revised upwards for both 2026 and 2027.[4]

Conversely, the imposition by the US of targeted tariffs on specific economies, particularly China (and to a lesser extent the European Union), could have an adverse effect on growth, particularly on exposed sectors such as car manufacturing. More broadly, measures of risk such as the Economic Policy Uncertainty Index remain elevated after a period of disruption from the pandemic, the surge in inflation, and fraying geopolitics.[5] In an investment environment with greater risk, investors are likelier to seek dollar-denominated real assets, particularly given the US dollar is still the overall reserve currency of the world.

In our opinion, the long-term demand drivers for US CRE remain attractive on a broad basis, and the outlook for fundamentals remains healthy.

ATTRACTIVE OPPORTUNITIES FOR INVESTMENT

Cross-border investors still view US CRE as a stable, safe investment. According to the 2024 Investment Intentions Survey from PREA, Asian investors favor the US for out-of-region investments. European investors have a slightly larger allocation to global strategies, however these may have a significant US element.[6] The current market dynamics are setting up for a period of new opportunities that prudent investors that are well-capitalized will be able to capture, leading to a period of outsized performance relative to peers. In light of the ongoing market volatility, our conviction around the intersection of real estate and technology has grown even stronger.

We see significant opportunities within logistics, data centers, and housing. The industrial market fundamentals remain strong, owing to accelerating tailwinds associated with e-commerce, on- and near-shoring, and a shift from “just-in-time” to “just-in-case” inventory levels.

Leasing activity reached 621.4 million square feet in the nine months to Q3 2024, up 5.2% compared to a year ago.The e-commerce share of total non-auto retail sales—a key indicator of demand for warehouse space—increased for the seventh consecutive quarter to a record-high 23.2%.[7] Even with the acceleration, there is still scope for expansion of online sales, compared to a more digitally mature market such as China, where almost 40% of the country’s retail sales come from e-commerce.[8]

In addition, evolving rental housing needs among a broad demographic coalition, combined with inadequate housing supply, has given rise to enduring investment opportunities across the rental housing spectrum. A combination of demographic trends, lifestyle choices, and the challenges of home ownership will continue to fuel strong demand for rental properties. Despite some excess supply over the last two years, which resulted in rental softening, the long-term fundamentals in housing remain compelling.

The rapidly increasing demand for digital storage is expected to change the data center landscape for many years to come. Some of the largest companies for cloud computing, including AWS, Microsoft, Meta, and Google are US-based, and are expected to be significant drivers of data center demand in the coming years. The demand for data is expected to be substantial, presenting a strategic advantage for platforms ready to serve major cloud providers and hyperscalers with a vertically integrated investment platform.

We believe private real estate debt also presents an attractive proposition, at a time when traditional lenders have withdrawn from more complex situations due to regulatory and financial pressures. We believe there continues to be an opportunity for alternative lenders to fill this void, create velocity, and capitalize on the robust demand in the commercial lending sector.

RELATIVE PERFORMANCE

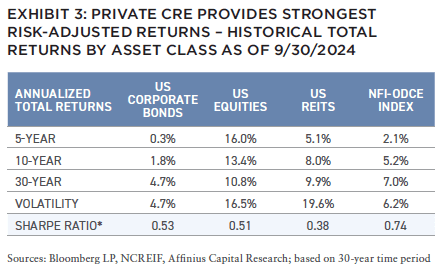

The long-term demand drivers for US CRE remain attractive on a broad basis. Over the last thirty years, private core real estate, as measured by the NCREIF ODCE Fund Index, has generated compelling absolute returns; but more importantly, the strongest risk-adjusted returns for investors based on a Sharpe ratio of 0.74.

The high-quality nature of CRE holdings that produce solid levels of current cash flow due to long-term, in-place lease agreements with creditworthy tenants combined with appreciation in the residual value of the assets has the ability to drive compelling performance. With greater clarity on future asset values anticipated, foreign buyers should become much more active as buying opportunities emerge.

DIVERSIFICATION

The US is well positioned for sustained growth over the next decade, particularly as compared to parts of Europe and Asia that are faced with shrinking populations. The working age population (15–64) has been declining in Japan for some time, started to go negative in Europe beginning in 2011, and began to go negative in China in 2019. But in the US, growth in the working age population remains positive.[9]

The US one of the most transparent developed markets globally, supported by a strong and deep private service sector market and coupled with leading academic institutions that all underpin reliable pricing and real-time information for global allocators. Powerful diversification benefits can be achieved by spreading investments across different regions and markets.

Despite the significant home bias within existing real estate portfolios, the US remains in focus for out-of-region capital deployments. Any investor needs to decide about the merits of a US real estate allocation given their own portfolio composition and objectives. But now, more than ever, one would do well not to ignore the positives. Given the relative liquidity and political stability, we believe the US will continue to attract foreign investors. The US economy is not immune from potential headwinds, but post-election there is a renewed confidence from businesses about the lower-tax, deregulatory, pro-growth mantra of the new administration that could help stimulate economic growth over the next several years. Given these factors, and amidst the uncertainty in global markets, one would do well not to ignore the positives for the US as a compelling investment opportunity at this moment in time.

NEW: SUMMIT #17

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

WHERE ARE WE IN THE CYCLE?: OVERVIEW OF THE US ECONOMY AND REAL ESTATE SECTOR

Richard Barkham + Jacob Cottrell | CBRE

COMPELLING OPPORTUNITIES: MAKING A CASE FOR US REAL ESTATE

Karen Martinus + Mark Fitzgerald + Max von Below | Affinius Capital

OPEN WINDOW: WHY NOW IS THE TIME TO INVEST IN COMMERCIAL REAL ESTATE

Chad Tredway + Josh Myerberg + Luigi Cerreta | JPMAM

NORMALIZING MOVEMENT: POPULATION MOVEMENTS NORMALIZING AFTER COVID-19 SHOCK

Martha Peyton + Matthew Soffair | LGIM America

CHRONIC SHORTAGE: THE US HOUSING SCARCITY WILL BE LIKELY TO PERSIST FOR SEVERAL YEARS

Gleb Nechayev | Berkshire Residential Investments

FLORIDA FOCUS: PRODUCTION INDEX BELOW 50 CURIOUSLY SIGNALS OPPORTUNITY

Rafael Aregger | Empira Group

WHOLESALE CHANGE: DEMOGRAPHIC CHANGES AND STAGNANT INVENTORY CREATE NEW OPPORTUNITIES FOR RETAIL

Stewart Rubin + Dakota Firenze | New York Life Real Estate Investors

GAME CHANGE: INFRASTRUCTURE GROWTH ACCELERATING WITH AI

Jon Treitel | CBRE Investment Management

FOR THE TREES: MASS TIMBER INTEGRATION IN INDUSTRIAL REAL ESTATE

Mary Ellen Aronow + Erin Patterson + Caroline Suarez + Cassidy Toth | Manulife Investment Management

BORDER INDUSTRIAL: INVESTING IN US/MEXICO BORDER PORT INDUSTRIAL MARKETS

Dags Chen, CFA + Lincoln Janes, CFA | Barings Real Estate

RESILIENCE AMIDST UNCERTAINTY: HOW ISRAELI AND UKRAINIAN INVESTORS ARE ADAPTING REAL ESTATE STRATEGIES DURING CONFLICT

Asaf Rosenheim | Profimex

CYBER RISK VIGILANCE: HOW REAL ESTATE DIRECTORS AND BOARDS CAN GUARD AGAINST CYBER RISK

Marie-Noëlle Brisson, FRICS, MAI + Michael Savoie, PhD | CyberReady, LLC

ALTERNATE REALTY: DIGITAL RIGHTS MANAGEMENT FOR REAL ESTATE AND AUGMENTED REALITY

Neil Mandt | Digital Rights Management + Steve Weikal | MIT Center for Real Estate

DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman + Gregory Fennell + Jon E. Linder | Dentons

HOUSING COMPLEX: CUTTING-EDGE APARTMENTS ARE A CATALYST FOR A MORE PROFITABLE FUTURE

Alejandro Dabdoub | AOG Living

NOTES

1. MSCI Real Assets. Data as of October 22, 2024

2. MSCI Real Assets. Capital Trends US Big Picture, Q3 2024

3. Oxford Economics. Key Themes 2025: Global resilience gives way to uncertainty. November 13, 2024

4. Oxford Economics. What Trump 2.0 means for the global economy. November 6, 2024

5. https://www.policyuncertainty.com/

6. PREA, 2024 Investment Intentions Survey

7. CBRE, US Industrial Figures Q3 2024

8. HSBC, China e-commerce, 12 March 2024

9. Our World in Data, November 2024

ABOUT THE AUTHORS

Karen Martinus is Senior Vice President, Research & Investments; Mark Fitzgerald, CFA, CAIA is Executive Director, Head of North American Research; Max von Below is Managing Director, Global Investors Group for Affinius Capital.

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

/ EXECUTIVE SPONSOR

AOG Living is a leading fully integrated, multifamily real estate investment, construction, and property management firm headquartered in Houston, Texas. AOG Living has acquired, built, or developed more than 20,000 multifamily units with a total aggregate value of over $2.4 billion and has a growing portfolio of more than 35,000 apartment homes and 170+ properties under management throughout the nation. Learn more at aogliving.com.

/ ASSOCIATE SPONSOR

Vertically integrated owner, operator, and developer of Sunbelt multifamily. Partnering with institutions on a single-asset and programmatic basis. 28k+ units acquired and developed. 62k+ units under management. 1,500+ associates. 8 Sunbelt states. To learn more, visit hrpinvestments.com and hrpliving.com. And for more information, contact john.duckett@hrpliving.com.

/ SUPPORTING SPONSOR

Affinius Capital is an integrated institutional real estate investment firm focused on value-creation and income generation. With a 40-year track record and $64 billion in gross assets under management, Affinius has a diversified portfolio across North America and Europe providing both equity and credit to its trusted partners and on behalf of its institutional clients globally. To learn more, visit affiniuscapital.com.