Temperature-controlled facilities utilized for storing perishable goods such as food, pharmaceuticals, and other temperature-sensitive products represent a small but essential portion of the US industrial base.

With a national inventory of approximately 300 million square feet, temperature-controlled industrial product (spanning freezer, cooler, and multi-temperature space) represents around 2% of the total industry inventory.

Within that slim portion of the whole, burgeoning growth is occurring, as the sector is benefitting from post-pandemic recognition of its structural importance: the temperature-controlled supply chain is essentially critical infrastructure supporting the fundamental human need for sustenance.

Additionally, secular growth trends are rendering “cold storage” an especially compelling alternative asset within the industrial real estate sector.

The origins of modern cold storage can be traced back to the late nineteenth and early twentieth centuries when the development and mass production of refrigeration systems, coupled with the invention of quick-freezing techniques, paved the way for constructing the first cold storage facilities. This enabled longer transportation and wider distribution of perishable goods, effectively breaking the age-old constraints imposed by geography and seasonality while also introducing consumers to a greater variety in their diets.

As the industry evolved, certain states emerged as hotbeds for cold storage space due to their proximity to ports, agricultural centers of production, and regional population centers. This threefold template for cold storage demand persists today, with California leading the nation in cold storage inventory, agricultural production, and population—not to mention its significant maritime ports, including the country’s largest complex by cargo volume, the ports of Los Angeles and Long Beach.

EVOLVING DEMAND DRIVERS

Throughout the latter half of the twentieth century, cold storage inventory experienced incremental growth. However, the rise of e-commerce in the mid-2000s disrupted traditional dynamics, triggering a new wave of demand within the cold storage market. Food and grocery e-commerce, as well as support for last-mile operations, have accelerated rapidly, particularly in fast-growing Sun Belt metropolitan areas. Population growth and shifting demographics in these regions have catalyzed greater demand for food and beverage products requiring cold storage.

Many consumers pivoted to online grocery shopping and meal services during the initial phases of the pandemic. What began as a safety consideration has now evolved into a convenient routine. E-commerce grocery sales are expected to grow at a 4.5% compounded annual growth rate (CAGR) over the next five years, outpacing the 1.3% rate expected for in-store grocery sales. In addition, grocery is forecasted to grow to 19% of all e-commerce sales by 2026, becoming the largest category e-commerce spending.1

Future annual growth forecasted does mark a decrease from the growth realized over the five years ending in 2023, due in part to the extreme surges in demand during the pandemic, and to the effects of persistent inflation, both of which the food industry and the cold storage sector are adjusting to in a variety of ways. For example, with grocery prices up 21% over the past three years according to federal data, consumers are spending less in real-dollar value on groceries. However, consumers are sourcing their food and beverage purchases from a wider variety of retailers. The average consumer shopped at 20.7 different grocery retailers between March 2023 and February 2024, a 23% increase from the same period between 2019 and 2020.2

Consumers shopping at a wider variety of retailers is underscored by data that shows a proliferation of new food and beverage retail establishments, which is in turn supported by the growth of users and operators in the cold storage sector. The number of food and beverage retailers grew 10% from 2020 to 2023, compared to a mere 1.2% between 2013 and 2020. Since e-commerce adoption has been steadily growing over the past decade, cold storage establishments have expanded in number at an elevated rate (19.2%) between 2013 and 2020, but that growth was also eclipsed in just the past few years (21% growth between 2020 and 2023)

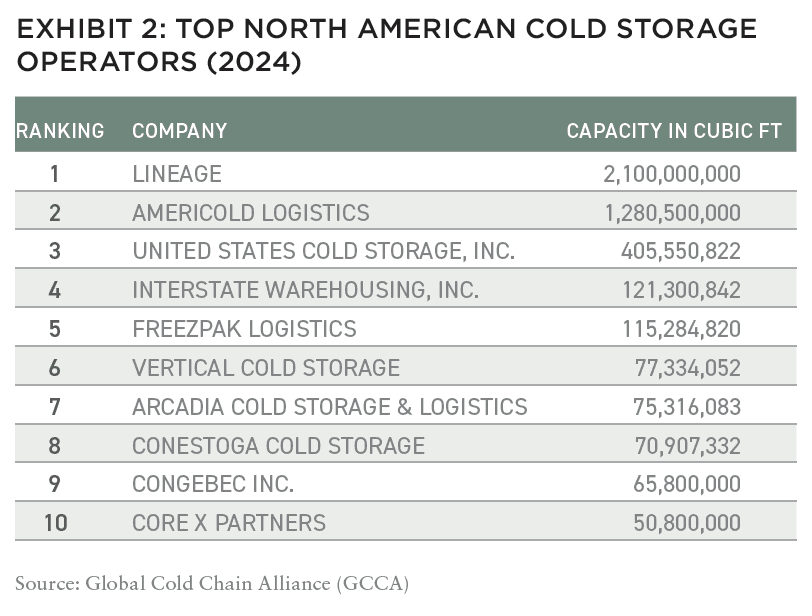

Interestingly, the expansion in the number of cold storage establishments is seen in part as a reaction to greater consolidation in cold storage on the macro scale. The biggest operators in cold storage, Lineage Logistics and Americold, accounted for 72% of the storage capacity of the top twenty-five markets in 2023, compared to 61% in 2019, increasing their share of the cold storage market through mergers, acquisitions, and development.3

As industry giants continue to solidify their dominant market positions, supporting the robust demand for cold storage space from their largest clients, this trend of consolidation is fueling competition in the sector. New and smaller users unable to attain space in the top cold storage firms’ facilities are presenting opportunities for new cold storage operator formation and development of the next generation of cold storage space, appealing to occupiers with a variety of specific focuses and needs.

Mirroring trends throughout the broader industrial market, third-party logistics companies are increasingly entering this segment, providing additive and complimentary fulfillment and logistics services. In the overall industrial market, third-party logistics providers represented a full third of all leasing activity in 2023 as companies increasingly outsource logistics operations due to cost and complexity of navigating supply chains.

The acceleration of grocery and food e-commerce and diversification and expansion across the broader food and cold storage sectors, amplified by population and demographics shifts, is complemented by several additional influential trends driving increased demand and development of modern cold storage space.

Cold storage is old. The average age of cold storage facilities in the top US markets is thirty-seven years, presenting challenges due to inefficient systems that generate higher operating costs and increased risk for product spoilage. Obsolescence will only accelerate further amid the convergence of evolving technologies such as automation, robotics, and AI. Demand for modern, functional space has driven renovations of older product and developments of new space to support supply chain optimization, adoption of warehouse automation, energy cost reduction, and compliance with sustainability mandates.

In addition to the growth of e-commerce, the reshoring and domestic expansion of critical supply chains like pharmaceuticals, medical supplies and other life science products is an emerging driver behind new cold storage construction – albeit on a more modest scale. These highly specialized facilities are typically purpose-built in proximity to major biomanufacturing hubs and rarely exceed 100,000 square feet. As one example, Alcami Corporation recently delivered a 65,000 square foot pharmaceutical storage facility in North Carolina’s Research Triangle to offer cold storage solutions to its biopharma clients. This delivery follows its 10,000-square-foot cold storage expansion at an existing Massachusetts facility last year.

DEVELOPMENT NEAR ALL-TIME HIGHS

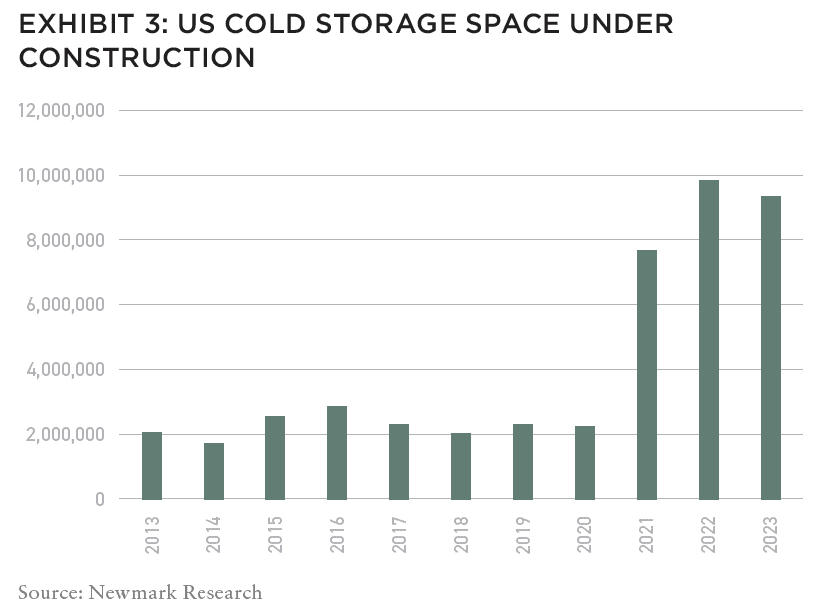

The convergence of these trends has pushed the development of cold storage space to new heights. The national cold storage development pipeline measured 9.4 million square feet at the beginning of 2024 (approximately 206 million cubic feet).

While ambient/dry warehousing space has seen a sharp decline in the pipeline after an unprecedented surge driven by demand and rock-bottom interest rates, cold storage development remains near record highs in 2024.

. . . And yet, cold storage still accounts for only 2.2% of the total industrial development pipeline, remaining disciplined in relation to demand. The limited development pipeline is due to a host of factors: steep development cost increases over the past few years, interest rate hikes, and unpredictable supply chain and consumer behavior.

Additionally, speculative cold storage space presents heightened riskiness in development as opposed to speculative ambient/dry storage due to a variety of factors. Port-serving and strong-population growth markets have seen a limited amount of speculative for cold storage development recently. Still, high operating costs, unique tenant requirements and the inflexibility for potential future conversion all play into consideration.

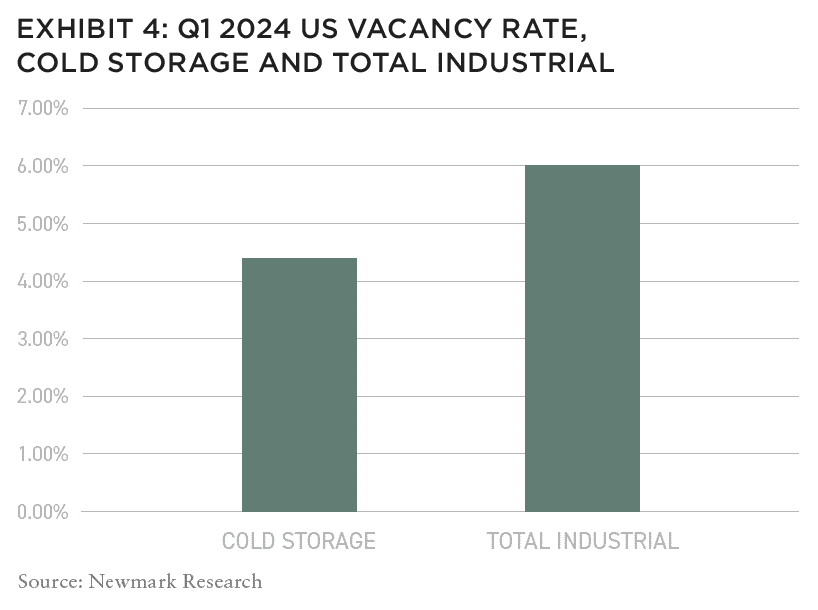

Conversely, modern specifications for ambient/dry storage are remarkably uniform across the country, which has allowed speculative development to substantially grow share; around 87% of the logistics pipeline was speculative in nature at the end of 2023, according to Newmark Research. Costs of cold storage construction are twice the cost per square foot of traditional warehouses or more, depending on building specifications and amount of cooler/freezer space, increasing financial risk for not securing a tenant pre-delivery. Nationally, the cold storage market vacancy rate was 4.4% in Q1 2024, 160 basis points less than the overall industrial average, indicating a steadier, more disciplined growth pattern has benefitted the market with little risk for oversupply.

EXPLORE THE NEW ISSUE

NOTE FROM THE EDITOR: WELCOME TO #15

Benjamin van Loon | AFIRE

MID-YEAR CRE MARKET OUTLOOK: AFIRE

Benjamin van Loon and Gunnar Branson | AFIRE

MULTIFAMILY OUTLOOK: AMERICAN REALTY ADVISORS

Sabrina Unger and Britteni Lupe | American Realty Advisors

MULTIFAMILY GAP CAPITAL: BARINGS REAL ESTATE

Dags Chen, CFA and Lincoln Janes, CFA | Barings Real Estate

SINGLE-FAMILY RENTAL OUTLOOK: CERBERUS CAPITAL MANAGEMENT

Kevin Harrell | Cerberus Capital Management

SINGLE-FAMILY RENTAL SUPPLEMENT: YARDI

Paul Fiorilla | Yardi

LOGISTICS OUTLOOK: BRIDGE INVESTMENT GROUP

Jay Cornforth, Jack Robinson, PhD, Morgan Zollinger, and Cole Nukaya | Bridge Investment Group

DATA CENTER OUTLOOK: PRINCIPAL ASSET MANAGEMENT

Casey Miller and Ben Wobschall | Principal Asset Management

SELF-STORAGE OUTLOOK: HEITMAN

Zubaer Mahboob | Heitman Europe

COLD-STORAGE OUTLOOK: NEWMARK

Lisa DeNight | Newmark

OFFICE OUTLOOK: CUSHMAN & WAKEFIELD

David Smith | Cushman & Wakefield

RETAIL OUTLOOK: MADISON INTERNATIONAL REALTY

Christopher Muoio | Madison International Realty

HOSPITALITY OUTLOOK: JLL

Zach Demuth | JLL

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

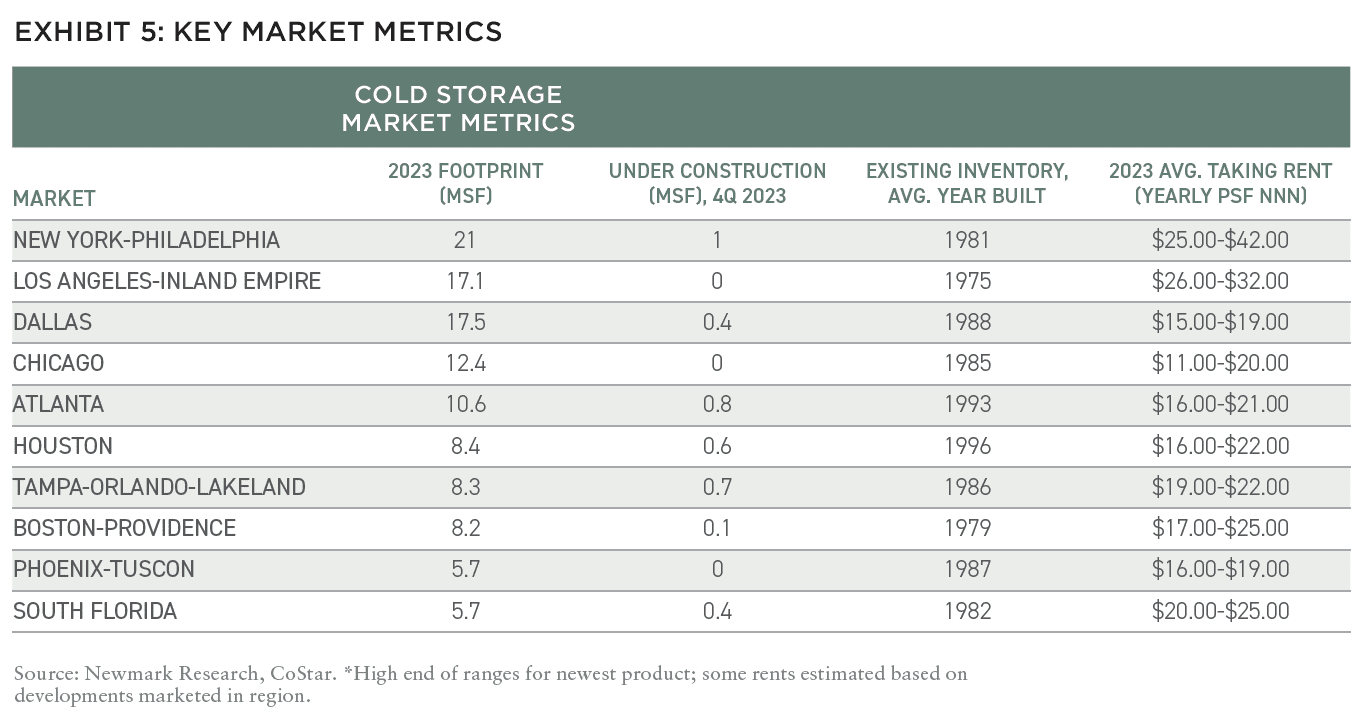

KEY MARKETS AND METRICS

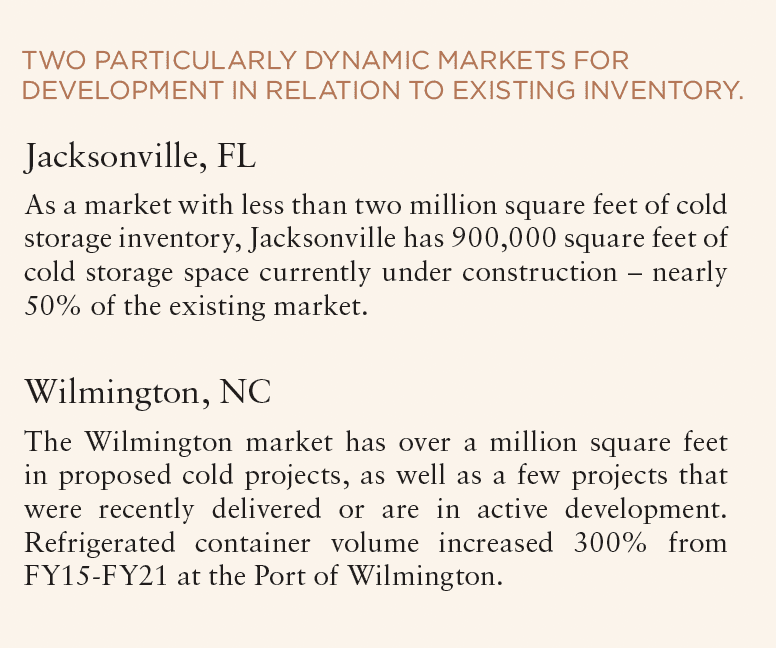

Cold storage projects are under construction in at least 18 states, with Florida, the Carolinas, and Texas seeing the greatest development volumes. Largely mirroring broader warehouse/distribution trends, seven of the top ten cold storage markets are in Sun Belt states, with Texas markets Dallas and Houston experiencing the greatest percentage growth in inventory over the past five years.

As transportation costs account for roughly half of overall supply chain costs, cold storage users will continue to follow end-consumers, with four of the top ten cold storage markets (Dallas, Houston, Central Florida, and Phoenix) located in the top ten major metros for population growth over the past five years.

WHAT’S NEXT FOR COLD STORAGE?

Looking ahead, projections from Newmark Research forecast annual cold storage inventory additions ranging from five to seven million square feet on average over the next five years. However, renovations of existing facilities may increase as an alternative to new construction, as approximately sixteen million square feet of inventory have undergone significant renovations over the past decade for properties with an average age of 42 years. Around 10% of the total US cold storage inventory predates 1960, which is essentially obsolete.

Beyond the risk profile of new development, another element that may keep new product development disciplined is the significant amount of cold storage space that resides within the retail sector. Major companies are increasingly leveraging their store networks’ proximity to customers by incorporating omnichannel fulfillment strategies.

Facilitating e-commerce orders via “click and collect” models has rapidly compressed the last-mile delivery footprint and proved increasingly popular with consumers. Players without a notable retail presence, like Amazon, are proactively expanding requirements for facilities that can fulfill orders for perishable groceries and pharmacy goods.4

Beyond the small-but-mighty handful of dominant national operators, the cold storage landscape is highly fragmented, with many small, localized family-owned firms or regional providers. These firms often lack the capital resources or incentive to modernize aging assets. This dynamic is leading to a bifurcation, with new state-of-the-art product being delivered for those capable of achieving scale, while older facilities may continue serving some tenants.

Cold storage opportunity lies ahead, driven by the continued proliferation of online grocery, the rise of new food production/distribution markets, ever-increasing sustainability mandates necessitating greater efficiency, and resolute national efforts to fortify food supply chain resilience after vulnerabilities were exposed during the pandemic. These trends will induce steady investment and spur innovation across the cold storage sector for years to come.

—

NOTES

1. EMarketer; as of November 2023.

2. Numerator, Wall Street Journal.

3. Global Cold Chain Alliance

4. Long, Ciara. “Amazon To Double Number Of Same-Day Delivery Distribution Hubs, CEO Says.” Bisnow, April 12, 2024. https://www.bisnow.com/national/news/industrial/amazon-will-use-its-same-day-warehouses-to-strengthen-its-foothold-in-grocery-pharmacy-123762.

—

ABOUT THE AUTHORS

Lisa DeNight is Managing Director, National Industrial Research, at Newmark, a leading commercial real estate advisor and service provider to large institutional investors, global corporations, and other owners.

—

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

Founded in 1992, Cerberus is a global leader in alternative investing with approximately $65 billion1 in assets across complementary credit, private equity, and real estate strategies. We invest across the capital structure where our integrated investment platforms and proprietary operating capabilities create an edge to improve performance and drive long-term value. Learn more.

Principal Real Estate is the dedicated real estate investment team of Principal Asset Management, the global investment solutions business for Principal Financial Group®. As a top 10 global real estate manager, with over $98 billion in assets under management and more than 60 years of experience, we provide clients with access to opportunities across both public and private equity and debt. Learn more.